Why Does GAAP Require Accrual Basis Accounting?

In general, most businesses use accrual accounting, while individuals and small businesses use the cash method. The IRS states that qualifying small business taxpayers can choose either method, but they must stick with the chosen method. The chosen method must also accurately reflect business operations.

What is difference between cash and accrual basis?

The difference between cash and accrual accounting lies in the timing of when sales and purchases are recorded in your accounts. Cash accounting recognizes revenue and expenses only when money changes hands, but accrual accounting recognizes revenue when it’s earned, and expenses when they’re billed (but not paid).

The other option is cash basis accounting or its close counterpart, the modified cash basis. The Internal Revenue Service allows individuals and small companies to use cash basis accounting. Cash accounting often works well for very small businesses that work primarily in cash. By requiring businesses to book revenue when earned and expenses when incurred, GAAP aims to prevent companies from misrepresenting their business activity by manipulating the timing of cash flows. Under cash accounting, a business could avoid recording a loss for, say, the month of June simply by holding off on paying its bills until July 1.

Both accrual and cash basis accounting methods have their advantages and disadvantages but neither shows the full picture about a company’s financial health. Although, accrual method is the most commonly used by companies, especially publicly traded companies. All general QuickBook reports show income and expenses accrued instead of paid when you set up your company on an accrual basis.

Cash Basis Accounting

It is important to note that changing accounting methods does not permanently change the business’s long-term taxable income, but only changes the way that income is recognized over time. In contrast, the accrual basis makes a greater effort to recognize income and expenses in the period to which they apply, regardless of whether or not money has changed hands.

Companies typically offset this issue by preparing a monthly cash flow statement. Although the IRS requires (and can only audit) all companies with sales exceeding over $5 million dollars, there are other reasons larger companies use the accrual basis method to record their transactions.

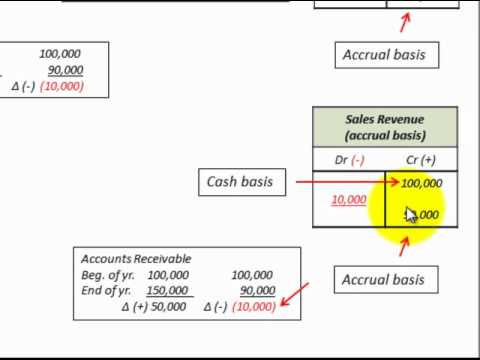

For example, you would record revenue when a project is complete, rather than when you get paid. The cash basis of accounting recognizes revenues when cash is received, and expenses when they are paid. This method does not recognize accounts receivable or accounts payable. The accrual method is most commonly used by companies, particularly publicly-traded companies.

What Are the Objectives of Financial Accounting?

In business, many times these occur simultaneously, but the cash transaction is not always completed immediately. Businesses with inventory are almost always required to use the accrual accounting method and are a great example to illustrate how it works.

Under the accrual accounting method, when a company incurs an expense, the transaction is recorded as an accounts payable liability on the balance sheet and as an expense on the income statement. As a result, if anyone looks at the balance in the accounts payable category, they will see the total amount the business owes all of its vendors and short-term lenders.

The contractor would still recognize the income from the contract in May, because that is when it was earned, even though the payment will not be received for some time. The main advantage of the accrual method is that it provides a more accurate picture of how a business is performing over the long-term than the cash method. The main disadvantages are that it is more complex than the cash basis, and that income taxes may be owed on revenue before payment is actually received. Accrual accounting is based on the idea of matching revenueswith expenses.

- A downside of accrual accounting is the lack of visibility into the company’s cash flow.

- The accrual method of accounting is used in the majority of companies.

Under accrual accounting, financial results of a business are more likely to match revenues and expenses in the same reporting period, so that the true profitability of a business can be recognized. Unless a statement of cash flow is included in the company’s financial statements, this approach does not reveal the company’s ability to generate cash. Changes in accounting methods generally result in adjustments to taxable income, either positive or negative. For example, say a business wants to change from the cash basis to the accrual basis. Thus the change in accounting method would require a negative adjustment to income of $5,000.

This differs from the cash basis of accounting, under which a business recognizes revenue and expenses only when cash is received or paid. Two concepts, or principles, that the accrual basis of accounting uses are the revenue recognition principle and the matching principle. The accrual method includes accounting for all the bills you owe in a payables account, and all the money owed to you, in a receivables account. This gives you a more accurate picture of your company’s true profitability, especially in the long-term.

You record income when you create an invoice for a completed project or sale of goods, and record expenses when you receive a bill. Your profit/loss report coincides directly with work completed and expenses incurred, but it’s only bank account registers in QuickBooks that show cash on hand. Reports on Accounts Receivable show money owed by customers and Accounts Payable on money you owe vendors. Any business owner knows that you don’t pay your bills with “revenue.” You pay them with cash, so cash flow is just as important to companies using accrual accounting as cash accounting. Combined, the income and cash flow statements present a full picture of when the company earns its money and when it gets its money.

When Is Accrual Accounting More Useful Than Cash Accounting?

If September looks like it’s going to be a weak month for sales, a company could prop up the numbers by delaying the billing of some customers so that their payment doesn’t arrive until after Sept. 1. With accrual accounting, a company hoping to manipulate its numbers like this would have to lie about the timing of revenue and expenses — in other words, to commit fraud. A business that uses the accrual basis of accounting recognizes revenue and expenses in the accounting period in which they are earned or incurred, regardless of when payment occurs.

If you are tempted to use the cash-basis method of accounting for your business, that’s understandable because of the method’s simplicity. However, your accounting system won’t track outstanding bills due, or allow you to offer credit terms to customers and track that outstanding money. Additionally, your company might look like it’s doing very well with a lot of cash in the bank. However, you could actually have a lot of unpaid bills not being tracked, that far exceed the cash in your business.

The business incurs the expense of stocking inventory and may also have sales for the month to match with the expense. If the business makes sales on credit, however, payment may not be received in the same accounting period. In fact, credit purchases are one of the many contributing factors that make business operations so complex. Accrual basis accounting is the standard approach to recording transactions for all larger businesses. This concept differs from the cash basis of accounting, under which revenues are recorded when cash is received, and expenses are recorded when cash is paid.

Under this system, revenue is recorded when it is earned, rather than when payment is received, and expenses recorded when they are incurred, rather than when payment is made. For example, say that a contractor performs all of the work required by a contract during the month of May, and presents his client with an invoice on June 1.

And significant discrepancies between the two can raise red flags, such as revenue that has been recorded before it was earned — and before it was billed to the customer. Managing a company is a complex process that involves multiple variables including the capital, revenue, and expenses along with reporting to stakeholders. Most companies start with a specified amount of capital gained through equity or debt to get their business running and maintain this capital level for efficient operations. While some small businesses may be able to fully manage the business on a cash basis, it is much more common for businesses to stretch out their revenue recognition and receivables over time. Accrual accounting is a method of accounting where revenues and expenses are recorded when they are earned, regardless of when the money is actually received or paid.

Accrual Accounting vs. Cash Basis Accounting: An Overview

When the expense is paid, the account payable liability account decreases and the asset used to pay for the liability also decreases. Small companies can choose from three different options to prepare their company’s financial statements. One option is accrual basis accounting, which is based on generally accepted accounting principles, or GAAP.

Similarly, an accrual basis company will record an expense as incurred, while a cash basis company would instead wait to pay its supplier before recording the expense. For example, say that a company pays its annual rent of $12,000 in January, rather than paying $1,000 per month for the year. The cash basis would recognize a rent expense for January of $12,000, since that is when the money was paid, and a rent expense of zero for the remainder of the year. Accrual accounting involves stating revenues and expenses as they occur, not necessarily when cash is received or paid out. In contrast, cash accounting systems do not report any income or expenses until the cash actually changes hands.

Accrual accounting requires companies to record sales at the time in which they occur. Unlike the cash basis method, the timing of actual payments is not important. This can be important for showing investors the sales revenue the company is generating, the sales trends of the company, and the pro forma estimates for sales expectations. In contrast, if cash accounting was used, a transaction would not be recorded for a while after the item leaves inventory. Investors would then be left in the dark as to the actual sales performance and total inventory on hand.

What is accrual basis accounting?

Accrual basis is a method of recording accounting transactions for revenue when earned and expenses when incurred. A key advantage of the accrual basis is that it matches revenues with related expenses, so that the complete impact of a business transaction can be seen within a single reporting period.

The accrual method of accounting is used in the majority of companies. By this method, you record revenues and expenses as soon as you incur them, even if the money hasn’t arrived in your account yet or the bill has not been paid. A downside of accrual accounting is the lack of visibility into the company’s cash flow.