What is the difference between a general ledger and a general journal?

General ledger accounting refers to recording and accounting used in storing and sorting out income statement and balance sheet transactions. General ledger accounts are diverse such as investments, cash, land, accounts receivable, to equipment and inventory. It also includes general ledger liability accounting where accounts could include customer deposits, notes payable, expenses payable accrued and accounts payable.

General ledgers contain income statements in their accounting, which include entries such as interest expense, sales, salaries expense, disposal assets loss, advertising expense, rent expense among others. General ledger holds accounting information containing both liabilities and assets, which essentially indicate the activities of the business. General ledger accounting has five unique categories inside accounting charts made up of expenses, assets, revenue, equity of the owner and liabilities. The asset accounts are made up of mostly accounts receivable, cash, fixed assets, investment and inventories. For liability, the accounts include accrued expenses payable, notes payable and accounts payable.

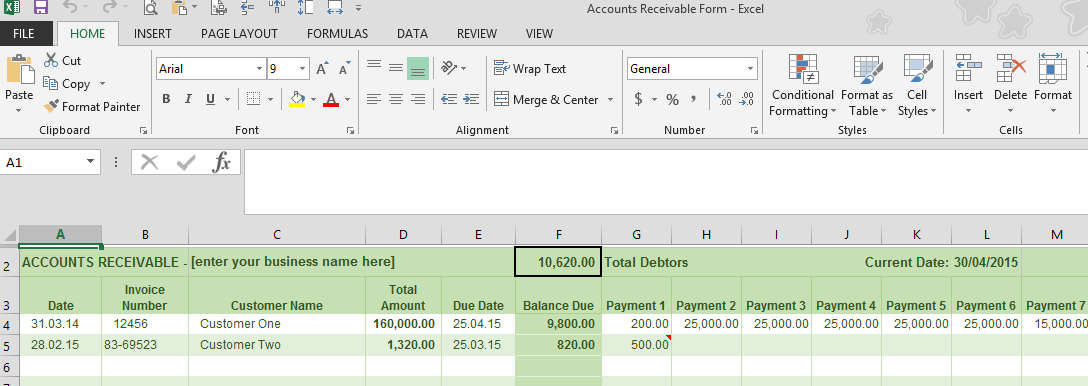

Accounts receivable refers to the outstanding invoices a company has or the money clients owe the company. The phrase refers to accounts a business has the right to receive because it has delivered a product or service. Accounts receivable, or receivables represent a line of credit extended by a company and normally have terms that require payments due within a relatively short time period. It typically ranges from a few days to a fiscal or calendar year.

The expense side of the income statement might be based on GL accounts for interest expenses and advertising expenses. Income statements are considered temporary accounts and closed at the end of the accounting year. In contrast, the accounts that feed into the balance sheet are permanent accounts used to track the ongoing financial health of the business. Companies record accounts receivable as assets on their balance sheets since there is a legal obligation for the customer to pay the debt.

The accounts receivable ledger is a subledger in which is recorded all credit sales made by a business. The ending balance of the accounts receivable ledger equals the aggregate amount of unpaid accounts receivable. Accounts payable are not to be confused with accounts receivable. Accounts receivablesare money owed to the company from its customers. As a result, accounts receivable are assets since eventually, they will be converted to cash when the customer pays the company in exchange for the goods or services provided.

Owner’s equity accounts are accounts that show how much money company owners and investors have invested in the company. A general ledger (GL) is a set of numbered accounts a business uses to keep track of its financial transactions and to prepare financial reports. Each account is a unique record summarizing each type of asset, liability, equity, revenue and expense. A chart of accounts lists all of the accounts in the general ledger, which can number in the thousands for a large business.

There are five main types of accounts in accounting, namely assets, liabilities, equity, revenue and expenses. Their role is to define how your company’s money is spent or received. Each category can be further broken down into several categories. Revenue is only increased when receivables are converted into cash inflows through the collection. Revenue represents the total income of a company before deducting expenses.

Accounts payable is a liability since it’s money owed to creditors and is listed under current liabilities on the balance sheet. Current liabilities are short-term liabilities of a company, typically less than 90 days. Information is stored in a ledger account with beginning and ending balances, which are adjusted during an accounting period with debits and credits. Individual transactions are identified within a ledger account with a transaction number or other notation, so that one can research the reason why a transaction was entered into a ledger account. Transactions may be caused by normal business activity, such as billing customers or recording supplier invoices, or they may involve adjusting entries, which call for the use of journal entries.

AR is any amount of money owed by customers for purchases made on credit. Accounts receivable are similar to accounts payable in that they both offer terms which might be 30, 60, or 90 days. However, with receivables, the company will be paid by their customers, whereas accounts payables represent money owed by the company to its creditors or suppliers.

Furthermore, accounts receivable are current assets, meaning the account balance is due from the debtor in one year or less. If a company has receivables, this means it has made a sale on credit but has yet to collect the money from the purchaser. Essentially, the company has accepted a short-term IOU from its client. Accounts receivable (AR) is the balance of money due to a firm for goods or services delivered or used but not yet paid for by customers. Accounts receivables are listed on the balance sheet as a current asset.

- General ledger accounting refers to recording and accounting used in storing and sorting out income statement and balance sheet transactions.

In other words, this means you allow them to take possession of your products before they pay you. If your business accepts credit cards, the credit card company manages the risk.

Accounts payable are the opposite of accounts receivable, which are current assets that include money owed to the company. Liability accounts are accounts that show what a company owes. Owner’s equity accounts are accounts that show how much money company owners and stockholders have invested in the company. Revenue accounts are accounts that show the cash inflows of a company due to operations, while expense accounts are accounts that show the cash outflows of a company due to operations.

General Ledger Control Accounts

But if customers are going to pay with cash or cheques, you must manage verification of payments and risk. The transactions of a business in general ledger accounting end up in double-entry bookkeeping record where each transaction is recorded twice. For each debit there’re credits to counterbalance them with liabilities cancelling assets and income offsetting losses. Critical in this method is that ensuring two columns are maintained for each account every account is analyzed to ascertain accuracy.

Once the chart of accounts has been established, then a company is ready to begin the process of accounting. The chart of accounts is broken down into asset, liability, owner’s equity, revenue and expense accounts.

Examples of General Ledger Control Accounts

Which general ledger accounts are involved in accounts receivable accounting?

The accounts receivable ledger is a subledger in which is recorded all credit sales made by a business. It is useful for segregating into one location a record of all amounts invoiced to customers, as well as all credit memos and (more rarely) debit memos issued to them, and all payments made against invoices by them.

Then, credit the accounts receivables account for the same amount. If you are using accounting software with a receivables option, it will allow you to easily keep track of invoices and payments that are due. You can load all of your customer and sales information into the system.

What is a general ledger account?

Companies looking to increase profits want to increase their receivables by selling their goods or services. Typically, companies practice accrual-based accounting, wherein they add the balance of accounts receivable to total revenue when building the balance sheet, even if the cash hasn’t been collected yet.

First, credit the sales account for the amount owed for the service. Next, debit the accounts receivables account for the same amount. When the customer pays, debit the cash account for the amount paid.

If your program has internet connectivity, it can send your digital invoices to customers. You can run a report that tells you what invoices are still outstanding, so you don’t have to keep separate paper files of paid and unpaid invoices. You need to set up procedures for accounts receivable if you extend credit to your customers. An account receivable arises when you allow a customer to take immediate possession of a product or receive a service in return for a promise to pay in the future.