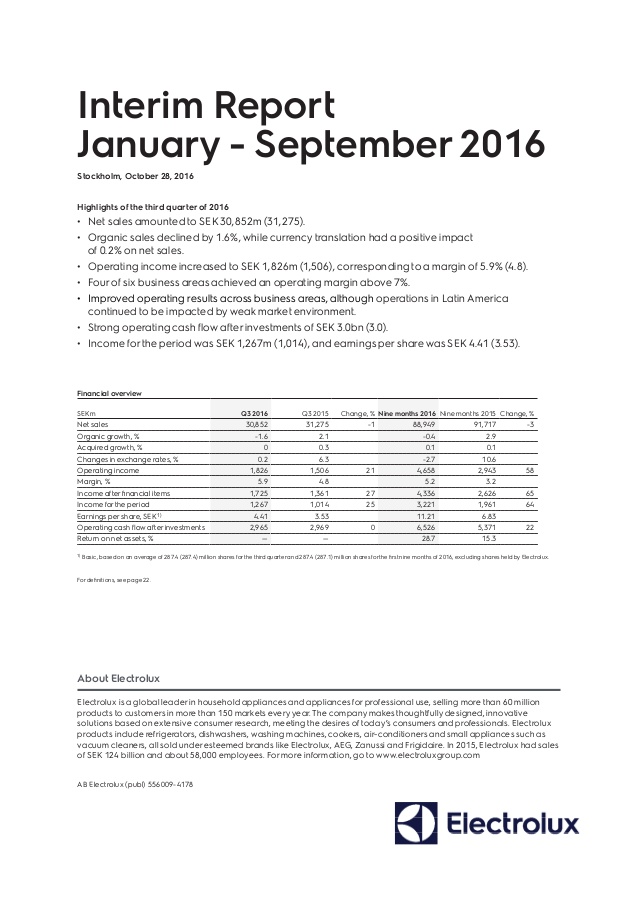

What Is an Interim Statement?

Interim financial statements are financial statements that cover a period of less than one year. They are used to convey information about the performance of the issuing entity prior to the end of the normal reporting year, and so are closely followed by investors. The concept is most commonly applied to publicly-held companies, which must issue these statements at quarterly intervals.

Interim statements are used to convey the performance of a company before the end of normal full-year financial reporting cycles. Unlike annual statements, interim statements do not have to be audited.

This will let the recipients know that these reports haven’t undergone the same rigorous review that your annual financial statements are subject to each year. Publicly traded companies and most nonprofits undergo an annual external audit.

Publicly-traded companies must file their reports with the Securities Exchange Commission. This form, known as a 10-Q, does not include all the detailed information, such as background and operations detail that the annual report (known as a 10-K) would. Especially if you follow publicly traded companies, you might have heard of “interim financial statements,” which are published with publicly traded companies’ quarterly reports. The term also appears on occasion in non-public companies, especially if a board of directors is involved or if the company is seeking investors. An interim statement is a financial report covering a period of less than one year.

Unlike an IRS or other tax audit, the purpose of an external audit is to verify the accuracy of the financial statements and to examine the business’s accounting practices. But external audits can become expensive and complicated, so interim financial statements aren’t audited. Interim financial statements cover a period of less than one year.

Often, these interim statements are prepared quarterly, but they may also be prepared monthly or even once every six months. Interim statements are financial reports produced by firms covering a period of less than one year. The twelve-month measurements will reflect any changes in estimates of amounts reported for the first six-month period.

Such periodic reporting between the dates of annual financial statements is known as interim reporting. If you have a child in middle school or high school, you’ve probably encountered interims, or progress reports, as they are sometimes called. Interims help parents stay on top of their child’s progress in a given subject, and because they’re usually issued half-way through a grading period, they also give families a chance to correct academic problems, if they exist.

Interim report may be a problem if the inventory level at the end of reporting period is below than in the beginning of the year. If you’ll be presenting your interim financial statements to investors, lenders, or a board of directors, include a note stating that these reports are interim financial statements and are for management purposes only.

Year-to-date measurements may involve changes in estimates of amounts reported in prior interim periods of the current financial year. But the principles for recognising assets, liabilities, income, and expenses for interim periods are the same as in annual financial statements. However, the frequency of an enterprise’s reporting (annual, half-yearly, or quarterly) should not affect the measurement of its annual results. To achieve that objective, measurements for interim reporting purposes should be made on a year-to-date basis. Paragraph 16(d) of this Standard requires similar disclosure in an interim financial report.

Interim reporting concentrates on providing periodic interim reports on fix interval during an accounting period say half yearly, quarterly or monthly. The basic problem which every reporting entity faces is determination of quantity of inventory, valuation of inventory and adjustments of valuation in every report. Inventory problem becomes more complex for companies following LIFO method.

Doing so benefits the client, which can issue its audited financial statements sooner. An interim audit also helps the auditors, who now have more time available during their peak audit season to engage in activities for more clients. In every business organisation inventories are main elements in the generation of income.

- Interim financial statements are financial statements that cover a period of less than one year.

- The concept is most commonly applied to publicly-held companies, which must issue these statements at quarterly intervals.

- They are used to convey information about the performance of the issuing entity prior to the end of the normal reporting year, and so are closely followed by investors.

Given the cost and time required for an audit, only the year-end financial statements are audited. If a company is publicly-held, its quarterly financial statements are instead reviewed.

My Child’s Interim Report Wasn’t Good, Now What?

The disclosures required by those other Accounting Standards are not required if an enterprise’s interim financial report includes only condensed financial statements and selected explanatory notes rather than a complete set of financial statements. An interim audit involves preliminary audit work that is conducted prior to the fiscal year-end of a client. The interim audit tasks are conducted in order to compress the period needed to complete the final audit.

AccountingTools

These entities issue three sets of interim statements per year, which are for the first, second, and third quarters. The final reporting period of the year is encompassed by the year-end financial statements, and so is not considered to be associated with interim financial statements. The most common interim statement may be the quarterly report. Aquarterly reportis a summary or collection of un-audited financial statements, such as balance sheets, income statements, and cash flow statements, issued by companies every quarter (three months).

A review is conducted by outside auditors, but the activities encompassed by a review are much reduced from those employed in an audit. The IASB also suggests that companies should follow the same guidelines in their interim statements as they use in preparing their annual reports (which are audited), including the use of similar accounting methods. Other Accounting Standards specify disclosures that should be made in financial statements. In that context, financial statements mean complete set of financial statements normally included in an annual financial report and sometimes included in other reports.

How do you write an interim report?

Interim reporting is the reporting of the financial results of any period that is shorter than a fiscal year. Interim reporting is usually required of any company that is publicly held, and it typically involves the issuance of three quarterly financial statements each year. These statements include: Balance sheet.

What Information Is on an Interim?

Interim statements increase communication between companies and the public and provide investors with up-to-date information between annual reporting periods. Periodic reporting at half yearly, quarterly and sometimes even monthly intervals, provides users with more current information for use in assessing the performance of a business enterprise.

The amounts reported in the interim financial report for the first six-month period are not retrospectively adjusted. Paragraphs 16(d) and 25 require, however, that the nature and amount of any significant changes in estimates be disclosed. However, by providing that the frequency of an enterprise’s reporting should not affect the measurement of its annual results, paragraph 27 acknowledges that an interim period is a part of a financial year.