What Is Amortization?

For monthly payments, the interest payment is calculated by multiplying the interest rate by the outstanding loan balance and dividing by twelve. The amount of principal due in a given month is the total monthly payment (a flat amount) minus the interest payment for that month. The next month, the outstanding loan balance is calculated as the previous month’s outstanding balance minus the most recent principal payment. The interest payment is once again calculated off the new outstanding balance, and the pattern continues until all principal payments have been made and the loan balance is zero at the end of the loan term.

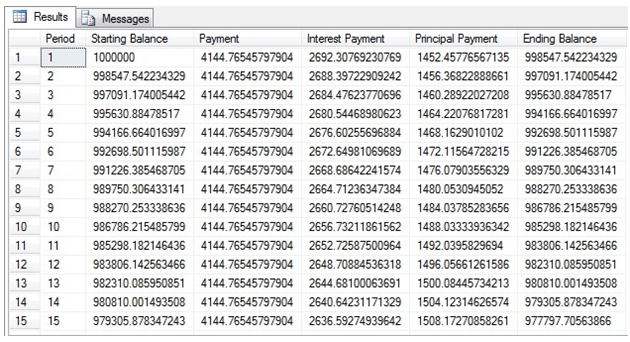

Sometimes it’s helpful toseethe numbers instead of reading about the process. The table below is known asan amortization table(or amortizationschedule) and demonstrates how each payment affects the loan, how much you pay in interest, and how much you owe on the loan at any given time. This amortization schedule is for the beginning and end of an auto loan. This is a $20,000 five-year loan charging 5% interest (with monthly payments). This loan calculator – also known as an amortization schedule calculator – lets you estimate your monthly loan repayments.

Loans with shorter terms have less interest because they amortize over a shorter period of time. Amortization is the process of spreading out a loan (such as a home loan or auto loans) into a series of fixed payments. While each monthly payment remains the same, the payment is made up of parts that change over time. A portion of each payment goes towards interest costs (what your lendergets paid for the loan) and reducing your loan balance (also known as paying off the loan principal). Amortization can refer to the process of paying off debt over time in regular installments of interest and principal sufficient to repay the loan in full by its maturity date.

What Is the Effective Interest Method of Amortization?

A portion of each payment is for interest while the remaining amount is applied towards the principal balance. The percentage of interest versus principal in each payment is determined in an amortization schedule. Amortization is a repayment feature of loans with equal monthly payments and a fixed end date. Even with a longer amortization mortgage, it is possible to save money on interest and pay off the loan faster through accelerated amortization. This strategy involves adding extra payments to your monthly mortgage bill, potentially saving you tens of thousands of dollars and allowing you to be debt-free (at least in terms of the mortgage) years sooner.

Subtract the interest from the total monthly payment, and the remaining amount is what goes toward principal. For month two, do the same thing, except start with the remaining principal balance from month one rather than the original amount of the loan. Personal loansthat you get from a bank, credit union,or online lenderare generally amortized loans as well. They often have three-year terms, fixed interest rates, and fixed monthly payments.

Here, we take a look at different mortgages amortization strategies for today’s home-buyers. It’s relatively easy to produce a loan amortization schedule if you know what the monthly payment on the loan is. Starting in month one, take the total amount of the loan and multiply it by the interest rate on the loan. Then for a loan with monthly repayments, divide the result by 12 to get your monthly interest.

It typically includes a full list of all the payments that you’ll be required to make over the lifetime of the loan. Each payment on the schedule gets broken down according to the portion of the payment that goes toward interest and principal. You’ll typically also be given the remaining loan balance owed after making each monthly payment, so you’ll be able to see the way that your total debt will go down over the course of repaying the loan. When you take out a loan with a fixed rate and set repayment term, you’ll typically receive a loan amortization schedule.

If an extra $100 payment were applied to the principal each month, the loan would be repaid in full in 25 years instead of 30, and the borrower would realize a $31,745 savings in interest payments. Bring that up to an extra $150 each month, and the loan would be satisfied in 23 years with a $43,204.16 savings. Naturally, you shouldn’t forgo necessities or take money out of profitable investments to make extra payments. The exact amount of principal and interest that make up each payment is shown in the mortgage amortization schedule (or amortization table).

Amortization is an accounting technique used to periodically lower the book value of a loan or intangible asset over a set period of time. First, amortization is used in the process of paying off debt through regular principal and interest payments over time. An amortization schedule is used to reduce the current balance on a loan, for example a mortgage or car loan, through installment payments.

If you are in a high tax bracket, this deduction will be of more value than to those with lower tax rates. The maturity of a mortgage loan follows an amortization schedule that keeps monthly payments equal while modifying the relative amount of principal vs. interest in each payment.

- Amortization is an accounting technique used to periodically lower the book value of a loan or intangible asset over a set period of time.

- First, amortization is used in the process of paying off debt through regular principal and interest payments over time.

While the most popular type is the 30-year, fixed-rate mortgage, buyers have other options, including 25-year and 15-year mortgages. The amortization period affects not only how long it will take to repay the loan, but how much interest will be paid over the life of the mortgage. Longer amortization periods typically involve smaller monthly payments and higher total interest costs over the life of the loan. Shorter amortization periods, on the other hand, generally entail larger monthly payments and lower total interest costs. It’s a good idea for anyone in the market for a mortgage to consider the various amortization options to find one that provides the best fit concerning manageability and potential savings.

Loan Amortization and Amortization Schedules

The NegAm loan, like all adjustable rate mortgages, is tied to a specific financial index which is used to determine the interest rate based on the current index and the margin (the markup the lender charges). Most NegAm loans today are tied to the Monthly Treasury Average, in keeping with the monthly adjustments of this loan. There are also Hybrid ARM loans in which there is a period of fixed payments for months or years, followed by an increased change cycle, such as six months fixed, then monthly adjustable. Adjustable-rate mortgages may allow you to pay even less per month than a 30-year, fixed rate mortgage and you may be able to adjust payments in other ways that could match an expected rise in personal income.

By understanding how to calculate a loan amortization schedule, you’ll be in a better position to consider valuable moves like making extra payments to pay down your loan faster. Also, interest rates on shorter loans are typically lower than those for longer terms. This is a good strategy if you can comfortably meet the higher monthly payments without undue hardship. Remember, even though the amortization period is shorter, it still involves making 180 sequential payments. It’s important to consider whether or not you can maintain that level of payment.

What is an example of amortization?

Amortization is the process of incrementally charging the cost of an asset to expense over its expected period of use, which shifts the asset from the balance sheet to the income statement. Examples of intangible assets are patents, copyrights, taxi licenses, and trademarks.

Similarly, interest-only and other types of balloon mortgages often have low payments but will leave you owing a huge balance at the end of the loan term, also a risky bet. By making regular payments toward a mortgage, you reduce the balance of both principal and interest. In the case of a 15-year fixed-rate mortgage, the loan is paid in full at the end of 15 years. A 30-year fixed-rate mortgage is paid in full at the end of 30 years, if payments are made on schedule.

Amortization

Second, amortization can also refer to the spreading out of capital expenses related to intangible assets over a specific duration – usually over the asset’s useful life – for accounting and tax purposes. A loan amortization schedule gives you the most basic information about your loan and how you’ll repay it.

Get the best rates

What amortization means?

Amortization is an accounting term that refers to the process of allocating the cost of an intangible asset over a period of time. It also refers to the repayment of loan principal over time.

With mortgage and auto loan payments, a higher percentage of the flat monthly payment goes toward interest early in the loan. With each subsequent payment, a greater percentage of the payment goes toward the loan’s principal. Amortization can be calculated using most modern financial calculators, spreadsheet software packages such as Microsoft Excel, or online amortization charts. As an amortization method the shorted amount (difference between interest and repayment) is then added to the total amount owed to the lender.

Such a practice would have to be agreed upon before shorting the payment so as to avoid default on payment. This method is generally used in an introductory period before loan payments exceed interest and the loan becomes self-amortizing. The term is most often used for mortgage loans; corporate loans with negative amortization are called PIK loans. The longer the amortization schedule (say 30 years), the more affordable the monthly payments, but at the same time the most interest to be paid to the lender over the life of the loan. This schedule is quite useful for properly recording the interest and principal components of a loan payment.

It also determines out how much of your repayments will go towards the principal and how much will go towards interest. Simply input your loan amount, interest rate, loan term and repayment start date then click “Calculate”. Amortization refers to the process of paying off a debt (often from a loan or mortgage) through regular payments.