What Are Trade Receivables? It’s Money Your Business Is Owed

What Does Increase in Trade Receivables Mean?

However, with receivables, the company will be paid by their customers, whereas accounts payables represent money owed by the company to its creditors or suppliers. Gem’s Bad Debts Expense will report credit losses of $2,000 on its June income statement. This expense is being reported even though none of the accounts receivables were due in June. (Recall the credit terms were net 30 days.) Gem is attempting to follow the matching principle by matching the bad debts expense as best it can to the accounting period in which the credit sales took place.

Another balance sheet account to analyze closely is allowance for doubtful accounts. A sharp increase in this account is a likely indicator that the company is issuing credit to riskier customers; take this information into consideration when analyzing the company’s receivables. Look at the company’s accounts receivable turnover, calculated by dividing its total sales on credit over a period of time by its average accounts receivable balance during that time. A high number here indicates that the company is effective at collecting on its receivables. Having an automated software to manage your bookkeeping needs does wonders for your business.

Sometimes companies sell their receivables for cents on the dollar to other companies that focus solely on collecting the owed amounts. Trade receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment. The amount of the provision is the difference between the asset’s carrying amount and the recoverable amount, being the present value of expected cash flows, discounted at the original effective interest rates. The carrying amount of the asset is reduced through the use of an allowance account, and the amount of the loss is recognised in the statement of comprehensive income as an administrative expense.

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets except for maturities greater than 12 months after the statement of financial position date. Loans and receivables comprise trade and other receivables in the statement of financial position excluding prepaid tax, prepaid expenses and VAT receivable.

Typically, companies practice accrual-based accounting, wherein they add the balance of accounts receivable to total revenue when building the balance sheet, even if the cash hasn’t been collected yet. Accounts payable is a liability since it’s money owed to creditors and is listed under current liabilities on the balance sheet.

What is trade receivables?

Trade receivables are amounts billed by a business to its customers when it delivers goods or services to them in the ordinary course of business. These billings are typically documented on formal invoices, which are summarized in an accounts receivable aging report.

Accounts receivable represents money owed to a business in return for goods already delivered or services already rendered. As an integral element of a company’s cash flow, accounts receivable can impact several other areas of accounting, including accounts payable, financial statements, budgeting and collections. The average maturity of accounts receivable and the ratio of outstanding receivables to cash-based revenue both exert pressure on the rest of accounting. Understanding these impacts can provide guidance as you make decisions on your credit and collections policies. The allowance is established by recognizing bad debt expense on the income statement in the same period as the associated sale is reported.

What Are Trade Receivables?

As we stated above, the account Allowance for Doubtful Accounts is a contra asset account containing the estimated amount of the accounts receivable that will not be collected. For example, let’s assume that Gem Merchandise Co.’s Accounts Receivable has a debit balance of $100,000 at June 30. Gem anticipates that approximately $2,000 of this is not likely to turn to cash, and as a result, Gem reports a credit balance of $2,000 in Allowance for Doubtful Accounts. The accounting entry to adjust the balance in the allowance account will involve the income statement account Bad Debts Expense. To guard against overstatement, a company will estimate how much of its accounts receivable will never be collected.

- A sharp increase in this account is a likely indicator that the company is issuing credit to riskier customers; take this information into consideration when analyzing the company’s receivables.

- Another balance sheet account to analyze closely is allowance for doubtful accounts.

In accordance with the matching principle of accounting, this ensures that expenses related to the sale are recorded in the same accounting period as the revenue is earned. If the receivable amount only converts to cash in more than one year, it is instead recorded as a long-term asset on the balance sheet (possibly as a note receivable). Accounts receivable are similar to accounts payable in that they both offer terms which might be 30, 60, or 90 days.

Only entities that extend credit to their customers use an allowance for doubtful accounts. Regardless of company policies and procedures for credit collections, the risk of the failure to receive payment is always present in a transaction utilizing credit. Thus, a company is required to realize this risk through the establishment of the allowance account and offsetting bad debt expense.

Receivables that a company does not expect to collect, instead of being reclassified as cash, are moved to a contra-asset account on the balance sheet known as allowance for doubtful accounts. An allowance for doubtful accounts is a contra-asset account that nets against the total receivables presented on the balance sheet to reflect only the amounts expected to be paid. The allowance for doubtful accounts is only an estimate of the amount of accounts receivable which are expected to not be collectible. The actual payment behavior of customers may differ substantially from the estimate.

There are many accounting software options that are great for managing everything from your sales invoices to maintaining income statements and balance sheets. This software allows you to keep and edit notes on specific clients, which is accessible to every member of the collection team as well as other concerned departments. Therefore, everyone will evidently know the current stance of the client regarding their payment. From the above example, suppose that customer ABC went bankrupt after its purchase from XYZ Company before paying the bill, or that it found itself insolvent. Even though the customer has a legal obligation to pay, it cannot do so if it doesn’t have the money.

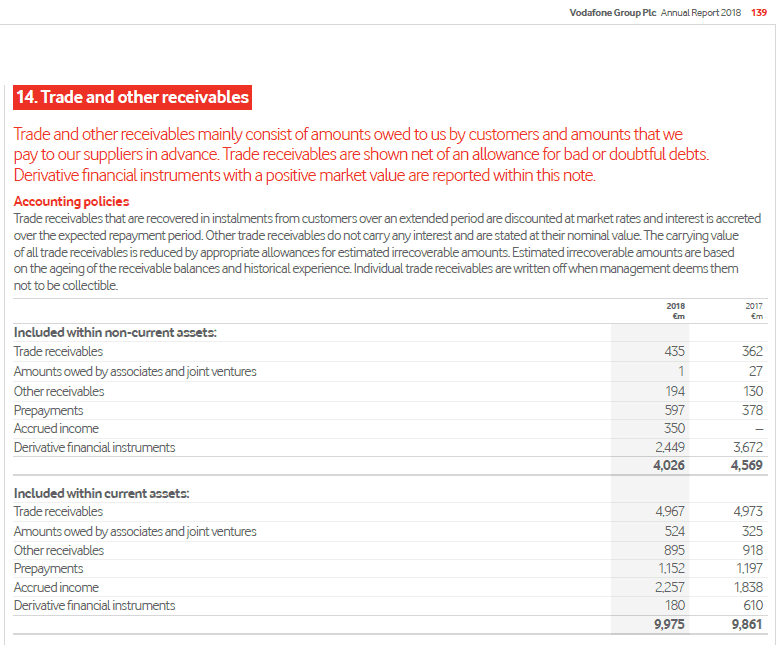

Trade receivables

Companies can calculate the amount a number of ways, but the amount is deducted from the accounts receivable total in the assets section of the balance sheet. Cash flow directly impacts your ability to pay short-term liabilities, including any current portions of long-term debt. If accounts receivable turnover time increases, a small business can be at risk of experiencing a negative cash flow, even if it has earned sufficient revenues to cover expenses and earn a profit. Revenue looks good on paper, but turning accounts receivable into cash is essential for a business to continue functioning. Consider your daily, weekly and monthly cash-flow needs to determine how much credit to extend to customers, taking care not to tip the balance so far in favor of receivables that you are unable to pay your own short-term liabilities.

Sometimes, companies are not able to pay the money they owe for a very long time, or ever. The company may have gone out of business, maybe their industry is seeing a downturn in demand, or it simply does not have the cash flow. There is an allowance for this on the vendor’s balance sheet with a line amount called “Allowance For Doubtful Accounts”.

This estimate is reported in a balance sheet contra asset account called Allowance for Doubtful Accounts. Trade receivables are amounts billed by a business to its customers when it delivers goods or services to them in the ordinary course of business. These billings are typically documented on formal invoices, which are summarized in an accounts receivable aging report. This report is commonly used by the collections staff to collect overdue payments from customers. In the general ledger, trade receivables are recorded in a separate accounts receivable account, and are classified as current assets on the balance sheet if you expect to receive payment from customers within one year of the billing date.

Revenue is only increased when receivables are converted into cash inflows through the collection. Companies looking to increase profits want to increase their receivables by selling their goods or services.