What Are the Advantages of Using a Flexible Budget vs. a Static Budget?

What is a flexible budget?

A document that consists of key financial ratios calculated based on information is included in the budget. These ratios will help to understand whether the master budget has been prepared realistically based on the actual past results.

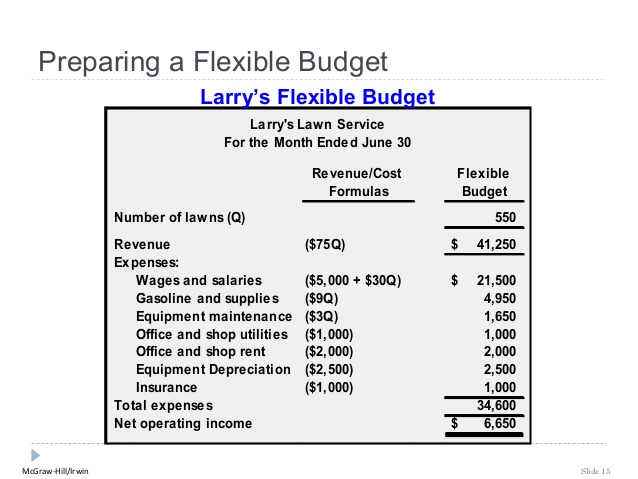

This type of budget shows the business what the static budget should have been by using actual output figures from the budget period. For example, if the static budget covered the production of 1,000 units, but only 600 units were made, the flexible budget takes only 600 units into account. The flexible budget shows the budgeted items from the static budget — such as cost and expected sales — and the actual results.

Both these budgets are considered important milestones in the budgetary control process. They are equipped with a number of uses such as cost control and performance measurement.

Master budget is a financial forecast of all elements in the business for the financial year prepared by combining many functional budgets such as sales budget, purchases budget, etc. These different budgets are interconnected and collectively provide accounting estimates for the upcoming financial period. Individual budgets will be prepared by each department, and the net outcome will be reflected in the master budget. A flexible budget allows you to transfer money to cover an unexpected emergency room bill or car repair.

When you transfer the money over, reduce the budgeted amount in the category you “borrowed” the money from. If a budget does not allow for flexibility, an emergency can make it difficult to meet your financial obligations. Create wiggle room by having a savings or miscellaneous category each month. A flexible budget allows you to plan expenses according to what you have made. When you do not make as much money, you would cut back to necessities only.

The difference between master budget and flexible budget mainly depends on the purpose they are prepared for. The budget prepared by amalgamating all the sub-budgets is referred to as the master budget whereas the budget that is prepared is for different activity levels is referred to as the flexible budget. If budgets are used effectively, they enable a wider range of benefits including revenue growth and effective cost control. Flexible budgets are particularly useful for organizations that have variable cost structures. Fixed Budget is mainly based on assumptions which are unrealistic and so this is not applicable to business concerns, but if we talk about Flexible Budget, it is more practicable.

Why Use a Flexible Budget?

In its simplest form, the flex budget uses percentages of revenue for certain expenses, rather than the usual fixed numbers. This allows for an infinite series of changes in budgeted expenses that are directly tied to actual revenue incurred.

The former is does not help to make a comparison if the actual and budgeted outputs differ, but the latter proves to helpful to judge the performance by comparing actual output with the budgeted targets. Cost Ascertainment is also not possible in case of fixed budget if the actual and budgeted levels of activity vary and the same can be easily determined in the case of a flexible budget. In the original budget, making 100,000 units resulted in total variable costs of $130,000. Dividing total cost of each category by the budgeted production level results in variable cost per unit of $0.50 for indirect materials, $0.40 for indirect labor, and $0.40 for utilities. The master budget is the aggregation of all lower-level budgets produced by a company’s various functional areas, and also includes budgeted financial statements, a cash forecast, and a financing plan.

This should not be confused with budget contingency that includes amounts for costs that are difficult to plan or predict. A flexible budget is a special kind of budget that includes fixed amounts and variable amounts that are based on a formula.

It finds this change very useful as it can alter its budgeted expenses to take its new orders into account. Instead of preparing a budget on a yearly basis, King’s Apparel switches over to a monthly budget. It also classifies each expense into “fixed,” “variable,” and “semi-variable.” This allows it to make accurate adjustments based on the level of activity. A flexible budget is a budget that changes according to business or activity volumes.

- Both these budgets are considered important milestones in the budgetary control process.

- This type of budget shows the business what the static budget should have been by using actual output figures from the budget period.

The master budget is typically presented in either a monthly or quarterly format, and usually covers a company’s entire fiscal year. There may also be a discussion of the headcount changes that are required to achieve the budget.

Line items vary by business type but commonly include individual overhead costs, such as materials, and labor costs. A favorable variance works to the business’s advantage by increasing overall income, while an unfavorable variance represents unexpected costs or cost increases that negatively affected profit levels. Unfavorable variances represent areas the business must work on to improve profits and reduce overhead. For example, if a factory has a larger than typical order for next month, the expense budget for that month could be based on the anticipated number of units to be produced. Management could calculate that there are $3 in variable costs per unit produced, so an increase in production of 10,000 units will increase the budget by $30,000 for that month.

By incorporating these changes into the budget, a company will have a tool for comparing actual to budgeted performance at many levels of activity. A flexible budget shows the budget figures for each line item from the static budget, the actual figures as shown on business statements, and the variances between the figures.

Separate fixed and variable costs

Beyond that threshold if you make more money, contribute a set amount to savings. For example if your basic needs can be met with $1500, then once you earn that for the month, contribute the first $300 to savings and spend the rest the way you want to. Or set a percentage, such as 50 percent of money earned beyond your threshold goes to savings and 50 percent is fun money. A flexible budget allows you to transfer money between categories and to create new spending limits as needed. If your water or electric bill is significantly higher in winter, you would adjust your budget by transferring money from a different category.

Definition of a Flexible Budget

A flexible budget is a budget that adjusts or flexes for the changes in the activity level. Unlike in a static budget, which is prepared for a single activity level, a flexible budget is more sophisticated and useful. Here, irrespective of the budgeted volume of output, the revenues and costs will be compared with the adjusted results to the actual volume.

Variance information, such as the difference between estimated and actual sales and estimated and actual operating costs, helps the business improve efficiency and identify problem areas. For example, if a static budget has a material cost of $45 each piece, but the flexible budget shows $65 each piece, the variance may indicate an issue with the material ordering or selection. A flexible budget variance is the difference between a line on the flexible budget and the corresponding information from actual business statements.

However, this approach ignores changes to other costs that do not change in accordance with small revenue variations. Consequently, a more sophisticated format will also incorporate changes to many additional expenses when certain larger revenue changes occur, thereby accounting for step costs.

What is a flexible budget?

Example of a Flexible Budget ABC Company has a budget of $10 million in revenues and a $4 million cost of goods sold. Of the $4 million in budgeted cost of goods sold, $1 million is fixed, and $3 million varies directly with revenue. Thus, the variable portion of the cost of goods sold is 30% of revenues.

Flexible budgets are most appropriate for organizations that operate with an increased variable cost structure where the costs are mainly associated with the level of activity. On the other hand, flexible budgets are time-consuming and require more planning due to the alterations in activity levels. In business, a flexible budget is one that you adjust based on changing costs and revenue. You build your budget at the beginning of the fiscal year, accounting for how much money your business has, needs and expects to make.

A flexible budget allows a business to see more variances than a static budget. The information from the flexible budget is based on actual results, allowing the business to adjust the static budget for accuracy and compare results. The business compares actual line-by-line costs and profits from the flexible budget with the estimations made in the static budget.

Then during higher earning months, you would save for the months when your income will be lower again. Set a spending threshold that covers your basic necessities, such as housing, food, utilities, gas.

Fixed expenses, savings expenses, and variable costs are the three categories that make up your budget, and are vitally important when learning to manage your money properly. When you’ve committed to living on a budget, you must know how to put your plan into action. A flexible budget is a budget that shows differing levels of revenue and expense, based on the amount of sales activity that actually occurs. Master budgets are usually presented in monthly or quarterly formats, for the entire financial year. Various other documents can also be presented along with the master budget in order to assist informed decision making.

Flexible budgets are not rigid as static budgets; thus, are an appropriate tool for performance measurement to evaluate the performance of the managers. If the volume is fixed, then the managers can later claim that the demand and cost forecasts significantly changed from the budgeted levels and they were unable to achieve the budget.