Using Cost-Volume-Profit Models for Sensitivity Analysis

How to Solve Profit With Cost & Revenue

Because a brewpub does not sell “units” of a specific product, the owners found the break-even point in sales dollars. The owners knew the contribution margin ratio and all fixed costs from the financial model. With this information, they were able to calculate the break-even point and margin of safety.

Profit formula is used to know how much profit has been made by selling a particular product. Formula for profit is majorly used for business and financial transactions. Profit arises when the selling price of any product sold is greater than the cost price (that is the price at which the product was originally bought). It should be noted that the profit and loss as a percentage is generally used to depict how much profit or loss a trader gets from a particular deal. Operating leverage shows how a company’s costs and profit relate to each other and changes can affect profits without impacting sales, contribution margin, or selling price.

The difference between the cost of a product or service and its sale price is called the markup (or markon). As a general guideline, markup must be set in such a way as to be able to produce a reasonable profit. The markup price can be calculated in your local currency or as a percentage of either cost or selling price.

Using the example of the $100 dollar product, the $40 in margin is a 67 percent markup on the $60 costs. Businesses must report information about sales and profits or losses each accounting period on the firm’s income statement. However, just listing the profit on sales may not tell you much about a company’s performance.

By dividing the total fixed costs by the contribution margin ratio, the break-even point of sales in terms of total dollars may be calculated. For example, a company with $100,000 of fixed costs and a contribution margin of 40% must earn revenue of $250,000 to break even. Profit may be added to the fixed costs to perform CVP analysis on a desired outcome. This is calculated by first determining the total variable costs for all the products.

The worried owner was relieved to discover that sales could drop over 35 percent from initial projections before the brewpub incurred an operating loss. Contribution margin is the difference between total sales and total variable costs.

And that does not factor in the marketing costs associated with increasing sales. The basic rule of a successful business model is to sell a product or service for more than it costs to produce or provide it.

Businesses also calculate profit as a percentage of sales, which is referred to as the profit margin. Now let’s look at what the sales department would have to do to achieve a comparable increase in net profit.

Subtract this amount from gross profit of $900,000 to find the operating profit of $400,000. Divide $400,000 by $2 million in sales to calculate the operating profit margin of 20%. Likewise, there’s a profit margin formula, which is sometimes termed a sales margin formula.

For a business to be profitable, the contribution margin must exceed total fixed costs. The unit contribution margin is simply the remainder after the unit variable cost is subtracted from the unit sales price. The contribution margin ratio is determined by dividing the contribution margin by total sales. Gross profit is the first profitability figure that appears on an income statement. It equals sales less the direct costs required to acquire products for sale.

Using the base case as an example, sales of $175,000 (cell D14) are calculated by multiplying the $250 sales price per unit (cell D5) by 700 units (cell D8). Variable costs of $105,000 (cell D15) are calculated by multiplying the $150 variable cost per unit (cell D6) by 700 units (cell D8). The contribution margin of $70,000 is calculated by subtracting variable costs from sales, and profit of $20,000 is calculated by subtracting fixed costs from the contribution margin. The contribution margin is used in the determination of the break-even point of sales.

- With this information, they were able to calculate the break-even point and margin of safety.

- Because a brewpub does not sell “units” of a specific product, the owners found the break-even point in sales dollars.

What is the formula for percentage profit?

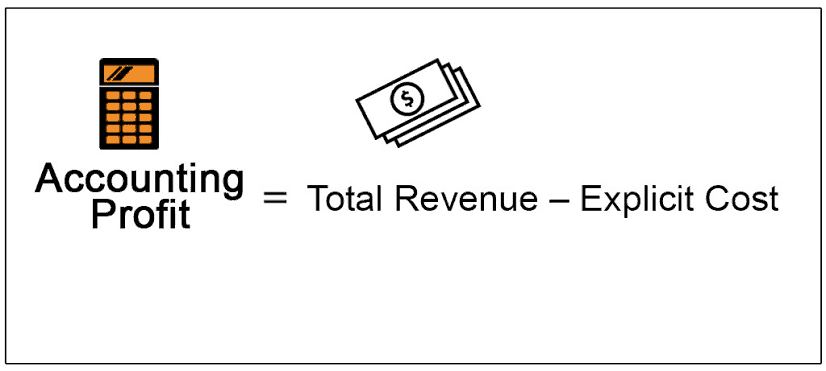

Economic profit is the difference between the total revenue received by a business and the total explicit and implicit costs for a firm. Economic profit can be both positive and negative and is calculated as follows: Total Revenues – (Explicit Costs + Implicit Costs) = Economic Profit.

Margin is the difference between cost and price, and the margin percentage is calculated from the sales price. Markup is added to the cost and calculated from your wholesale cost.

ACCOUNTING

Cost can be the wholesale price you pay your supplier or the cost to manufacture the product if you produce it yourself. Subtract the cost from the sale price to get profit margin, and divide the margin into the sale price for the profit margin percentage. For example, you sell a product for $100 that costs your business $60. It’s computed by subtracting financing expenses from operating profit. Miscellaneous items, such as interest earned on investments, legal judgments and other amounts not related to the firm’s primary operations, are also added or subtracted.

How do you calculate profit?

The formula for solving profit is fairly simple. The formula is profit (p) equals revenue (r) minus costs (c). The process of organizing revenue and costs and assessing profit typically falls to accountants in the preparation of a company’s income statement.

These costs are deducted from revenues and are the alternative returns you decided not to pursue. Adding implicit costs to your profit calculation gives you another way to compare financial alternatives. Calculate a retail or selling price by dividing the cost by 1 minus the profit margin percentage. If a new product costs $70 and you want to keep the 40 percent profit margin, divide the $70 by 1 minus 40 percent – 0.40 in decimal. The profit margin on a product you sell is the difference between your cost and the selling price.

BUSINESS IDEAS

Variable costs are all the costs that increase proportionately to an increase in production. They include material costs, direct labor costs and any other costs that increase as production increases. Variable costs include all costs that are not fixed costs, such as equipment, indirect labor and real estate. Add all of the variable costs and divide the total by the number of units produced. In any retail or manufacturing business, it is important to know how much each unit sold contributes to the business’s profit.

Cost-volume-profit (CVP) analysis is a method of cost accounting that looks at the impact that varying levels of costs and volume have on operating profit. Profit contribution is a tool intended to help make management decisions. Operating profit equals the gross profit minus selling, administrative and general costs. Examples of operating costs include office salaries, advertising and office rent. For instance, the Acme Widget Company has operating expenses of $500,000.

By calculating the contribution margin, a manager can determine which products are most profitable and make production decisions accordingly. It is easy to calculate the profit contribution of a product by following several basic steps. Keep track of the difference between markup and margin when calculating your retail or selling prices.

In retail, direct costs are usually referred to as the cost of goods sold. Suppose the Acme Widget Company has $2 million in sales for an accounting period. If the cost of goods sold equals $1,100,000, subtracting this amount leaves a gross profit of $900,000. The gross profit margin is calculated as $900,000 divided by $2 million, with the result multiplied by 100 to express it as a percentage.

To calculate how many more sales dollars would have to be generated we divide the needed additional profits ($4,500) by the operating profit margin (21%). The sales department will therefore have to sell an additional $21,428.57 worth of your product or service, which is the equivalent of increasing sales by 15%.

The formula is the profit divided by total revenue and multiplied by 100 to express as a percentage. Simply choose the applicable profit figure to calculate as a percentage of sales. One of the owners asked, “What if our projected revenues are too high? After all, we will have debt of well over $1 million, and I don’t want anyone coming after my personal assets if the business doesn’t have the money to pay!

Suppose Acme Widget Company has net costs in this category of $100,000. Subtracting out from the operating profit of $400,000 leaves you with $300,000 in pretax profit. Again, divide by total sales of $2 million to calculate the pretax profit margin of 15%. Businesses calculate profit margins because they make it easier to assess company performance than relying on the actual dollar figures alone.

Formulas

Suppose you find the business records an operating profit margin of 30% one year and this falls to 25% the following year. This may indicate the firm is using its revenues less efficiently since more of each dollar is going to cover operating costs. Using margins also allows you to compare how efficiently companies of different sizes use their revenue dollars.