Three Types of Cash Flow Activities

The exact formula used to calculate the inflows and outflows of the various accounts differs based on the type of account. In the most commonly used formulas, accounts receivable are used only for credit sales and all sales are done on credit. If cash sales have also occurred, receipts from cash sales must also be included to develop an accurate figure of cash flow from operating activities. Since the direct method does not include net income, it must also provide a reconciliation of net income to the net cash provided by operations. The purpose of drawing up a cash flow statement is to see a company’s sources of cash and uses of cash over a specified time period.

When these operating expenses are added to the net profit, the cash flow of this business is a respectable $150,000. Multiply that number by two or three, and ABC Inc. is worth between $300,000 and $450,000. Operating cash flow is just one component of a company’s cash flow story, but it is also one of the most valuable measures of strength, profitability, and the long-term future outlook.

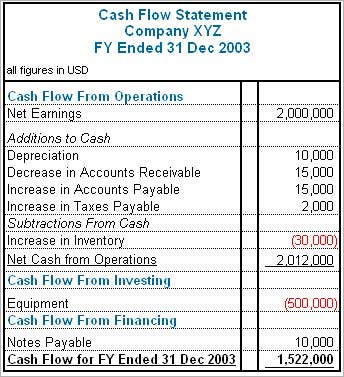

Essentially, the cash flow statement is concerned with the flow of cash in and out of the business. The statement captures both the current operating results and the accompanying changes in the balance sheet and income statement. The operating cash flows component of the cash flow statement refers to all cash flows that have to do with the actual operations of the business. Essentially, it is the difference between the cash generated from customers and the cash paid to suppliers. Significant cash outflows are salaries paid to employees and purchases of supplies.

Unlevered Free Cash Flow

Those preparers that use the direct method must also provide operating cash flows under the indirect method. The indirect method must be disclosed in the cash flow statement to comply with U.S. accounting standards, or GAAP.

Corporate Cash Flow: Understanding the Essentials

What is an example of a cash flow?

Cash flow is the net amount of cash that an entity receives and disburses during a period of time. This is cash paid by customers for services or goods provided by the entity. Financing activities. An example is debt incurred by the entity. Investment activities.

With theindirect method, cash flow from operating activities is calculated by first taking the net income off of a company’s income statement. Because a company’s income statement is prepared on anaccrual basis, revenue is only recognized when it is earned and not when it is received. The three categories of cash flows are operating activities, investing activities, and financing activities. Investing activities include cash activities related to noncurrent assets. Financing activities include cash activities related to noncurrent liabilities and owners’ equity.

The cash flow statement, as the name suggests, provides a picture of how much cash is flowing in and out of the business during the fiscal year. Non-cash investing and financing activities are disclosed in footnotes to the financial statements. General Accepted Accounting Principles (GAAP), non-cash activities may be disclosed in a footnote or within the cash flow statement itself.

It is derived either directly or indirectly and measures money flow in and out of a company over specific periods. Unlike net income, OCF excludes non-cash items like depreciation and amortization, which can misrepresent a company’s actual financial position. It is a good sign when a company has strong operating cash flows with more cash coming in than going out. Companies with strong growth in OCF most likely have a more stable net income, better abilities to pay and increase dividends and more opportunities to expand and weather downturns in the general economy or their industry. Still, whether you use the direct or indirect method for calculating cash from operations, the same result will be produced.

- Essentially, the cash flow statement is concerned with the flow of cash in and out of the business.

- The operating cash flows component of the cash flow statement refers to all cash flows that have to do with the actual operations of the business.

This sheds important insight into how the company is making or losing money. The cash flow is widely believed to be the most important of the three financial statements because it is useful in determining whether a company will be able to pay its bills and make the necessary investments. A company may look really great based on the balance sheet and income statement, but if it doesn’t have enough cash to pay its suppliers, creditors, and employees, it will go out of business. A positive cash flow means that more cash is coming into the company than going out, and a negative cash flow means the opposite. One of the components of the cash flow statement is the cash flow from investing.

Free Cash Flow

Just as with sales, salaries, and the purchase of supplies may appear on the income statement before appearing on the cash flow statement. Operating cash flows, like financing and investing cash flows, are only accrued when cash actually changes hands, not when the deal is made. Cash flows from operating activities can be calculated and disclosed on the cash flow statement using the direct or indirect method. The direct method shows the cash inflows and outflows affecting all current asset and liability accounts, which largely make up most of the current operations of the entity.

In contrast, under the indirect method, cash flow from operating activities is calculated by first taking the net income from a company’s income statement. Because a company’s income statement is prepared on an accrual basis, revenue is only recognized when it is earned and not when it is received. The indirect method also makes adjustments to add back non-operating activities that do not affect a company’s operating cash flow.

Investments in property, plant, and equipment and acquisitions of other businesses are accounted for in the cash flow from investing activities section. Proceeds from issuing long-term debt, debt repayments, and dividends paid out are accounted for in the cash flow from financing activities section. Assessing the amounts, timing, and uncertainty of cash flows is one of the most basic objectives of financial reporting. Understanding the cash flow statement – which reports operating cash flow, investing cash flow, and financing cash flow — is essential for assessing a company’s liquidity, flexibility, and overall financial performance.

Non-cash financing activities may include leasing to purchase an asset, converting debt to equity, exchanging non-cash assets or liabilities for other non-cash assets or liabilities, and issuing shares in exchange for assets. To illustrate this equation, let’s say ABC Inc. has a net profit of $30,000 on sales of $600,000. Other cash flow components in the operating expenses include interest payments of $10,000, depreciation of $25,000 and amortization of $3,000.

Regardless of whether the net cash flow is positive or negative, an analyst will want to know where the cash is coming from or going to. The three types of cash flows (operating, investing, and financing) will all be broken down into their various components and then summed. The company may have a positive cash flow from operations, but a negative cash flow from investing and financing.

Financial statements are written records that convey the business activities and the financial performance of a company. Financial statements include the balance sheet, income statement, and cash flow statement. For investors, the cash flow statement reflects a company’s financial healthsince typically the more cash that’s available for business operations, the better. Sometimes a negative cash flow results from a company’s growth strategy in the form of expanding its operations.

Cash flow definition

In the case of a trading portfolio or an investment company, receipts from the sale of loans, debt, or equity instruments are also included. However, purchases or sales oflong-term assetsare not included in operating activities. The cash flow statement (CFS) measures how well a company manages its cash position, meaning how well the company generates cash to pay its debt obligations and fund its operating expenses. The cash flow statement complements the balance sheet and income statementand is a mandatory part of a company’s financial reports since 1987.