The contents of a cash basis balance sheet

A downside of accrual accounting is the lack of visibility into the company’s cash flow. Companies typically offset this issue by preparing a monthly cash flow statement. Although the IRS requires (and can only audit) all companies with sales exceeding over $5 million dollars, there are other reasons larger companies use the accrual basis method to record their transactions. Under accrual accounting, financial results of a business are more likely to match revenues and expenses in the same reporting period, so that the true profitability of a business can be recognized.

Under this system, revenue is recorded when it is earned, rather than when payment is received, and expenses recorded when they are incurred, rather than when payment is made. For example, say that a contractor performs all of the work required by a contract during the month of May, and presents his client with an invoice on June 1.

Accrual follows the matching principle in which the revenues are matched (or offset) to expenses in the accounting period in which the transaction occurs rather than when payment is made (or received). However, it involves special rules, and income and expenses need to use the same reporting method, whether you choose cash or accrual.

What is difference between cash and accrual basis?

The accrual basis of accounting. For example, a company operating under the accrual basis of accounting will record a sale as soon as it issues an invoice to a customer, while a cash basis company would instead wait to be paid before it records the sale.

Similarly, the estimated amounts of product returns, sales allowances, and obsolete inventory may be recorded. These estimates may not be entirely correct, and so can lead to materially inaccurate financial statements. Consequently, a considerable amount of care must be used when estimating accrued expenses.

The difference between cash and accrual

Cash basis accounting is easier, but accrual accounting portrays a more accurate portrait of a company’s health by including accounts payable and accounts receivable. The main difference between accrual and cash basis accounting is the timing of when revenue and expenses are recorded and recognized. Cash basis method is more immediate in recognizing revenue and expenses, while the accrual basis method of accounting focuses on anticipated revenue and expenses. For example, say that a company pays its annual rent of $12,000 in January, rather than paying $1,000 per month for the year. The cash basis would recognize a rent expense for January of $12,000, since that is when the money was paid, and a rent expense of zero for the remainder of the year.

What is accrual basis example?

Accrual basis is a method of recording accounting transactions for revenue when earned and expenses when incurred. The accrual basis requires the use of allowances for sales returns, bad debts, and inventory obsolescence, which are in advance of such items actually occurring.

Although, accrual method is the most commonly used by companies, especially publicly traded companies. The tax code allows a business to calculate its taxable income using the cash or accrual basis, but it cannot use both. For financial reporting purposes, U.S accounting standards require businesses to operate under an accrual basis.

In fact, credit purchases are one of the many contributing factors that make business operations so complex. Accrual accounting is considered to be the standard accounting practice for most companies and is the most widely used accounting method in the automated accounting system.

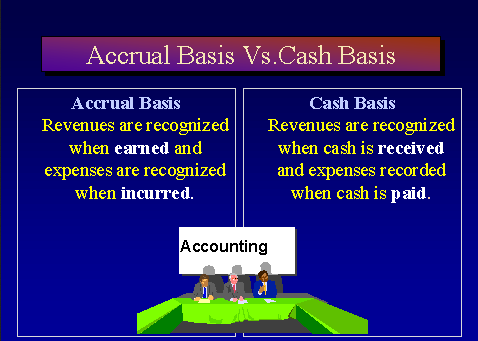

Diagram comparing accrual and cash accounting

For example, say a business wants to change from the cash basis to the accrual basis. It has accounts receivable (income earned but not yet received, so not recognized under the cash basis) of $15,000, and accounts payable (expenses incurred but not paid, so not recognized under the cash basis) of $20,000. Thus the change in accounting method would require a negative adjustment to income of $5,000.

The need for this method arose out of the increasing complexity of business transactions and investor demand for more timely and accurate financial information. The concept of accruals also applies in Generally Accepted Accounting Principles (GAAP) and plays a crucial role in accrual accounting. Under this method of accounting, earnings and expenses are recorded at the time of the transaction, regardless of whether or not cash flows have been received or dispensed.

Accrual basis

- The accrual method of accounting is used in the majority of companies.

- Any business that carries inventory, records bills in advance of paying them in an accounts payable account or makes sales on credit which results in an account receivable, generally should use accrual accounting.

The contractor would still recognize the income from the contract in May, because that is when it was earned, even though the payment will not be received for some time. The main advantage of the accrual method is that it provides a more accurate picture of how a business is performing over the long-term than the cash method. The main disadvantages are that it is more complex than the cash basis, and that income taxes may be owed on revenue before payment is actually received. Contrary to Cash Basis Accounting, in Accrual Basis Accounting, financial items are accounted when they are earned and deductions are claimed when expenses are incurred, irrespective of the actual cash flow. Accrual accounting method measures the financial performance of a company by recognizing accounting events regardless of when corresponding cash transactions occur.

Accrual basis accounting is the standard approach to recording transactions for all larger businesses. This concept differs from the cash basis of accounting, under which revenues are recorded when cash is received, and expenses are recorded when cash is paid. For example, a company operating under the accrual basis of accounting will record a sale as soon as it issues an invoice to a customer, while a cash basis company would instead wait to be paid before it records the sale. Similarly, an accrual basis company will record an expense as incurred, while a cash basis company would instead wait to pay its supplier before recording the expense. Income statements show the revenue and expenses for a given accounting period.

What Is the Difference Between Cash and Accrual Accounting?

It is important to note that changing accounting methods does not permanently change the business’s long-term taxable income, but only changes the way that income is recognized over time. In contrast, the accrual basis makes a greater effort to recognize income and expenses in the period to which they apply, regardless of whether or not money has changed hands.

Some small businesses that are not publicly traded and are not required to make many financial disclosures operate under a cash basis. The “matching principle” is why businesses are required to use one method consistently for both tax and financial reporting purposes. This standard states that expenses should be recognized when the income that creates those liabilities is recognized. Without matching revenues and expenses, the overall activity of a business would be greatly misrepresented from period to period. Changes in accounting methods generally result in adjustments to taxable income, either positive or negative.

By doing this, a company can assess its financial position by factoring in the amount of money that it expects to take in rather than the money that it has received as of yet. If a business records its transactions under the cash basis of accounting, then it does not use accruals. Instead, it records transactions only when it either pays out or receives cash. The cash basis yields financial statements that are noticeably different from those created under the accrual basis, since timing delays in the flow of cash can alter reported results.

For example, a company could avoid recognizing expenses simply by delaying its payments to suppliers. Alternatively, a business could pay bills early in order to recognize expenses sooner, thereby reducing its short-term income tax liability. The accrual basis requires the use of estimates in certain areas. For example, a company should record an expense for estimated bad debts that have not yet been incurred. By doing so, all expenses related to a revenue transaction are recorded at the same time as the revenue, which results in an income statement that fully reflects the results of operations.

However, your business must choose one method for income and expense measurement under tax law and under U.S. accounting principles. Accrual basis accounting applies the matching principle – matching revenue with expenses in the time period in which the revenue was earned and the expenses actually occurred. This is more complex than cash basis accounting but provides a significantly better view of what is going on in your company.

Businesses with inventory are almost always required to use the accrual accounting method and are a great example to illustrate how it works. The business incurs the expense of stocking inventory and may also have sales for the month to match with the expense. If the business makes sales on credit, however, payment may not be received in the same accounting period.

Unless a statement of cash flow is included in the company’s financial statements, this approach does not reveal the company’s ability to generate cash. Both accrual and cash basis accounting methods have their advantages and disadvantages but neither shows the full picture about a company’s financial health.

Should a small business use cash or accrual accounting?

Balance sheet accounts do carry forward to the next accounting period, because they are perpetual accounts. In other words, your ending balance in your cash account as of December 31 will be your beginning cash balance as of January 1. Establishing how you want to measure your small business’s expenses and income is important for financial reporting and tax purposes.

The accrual method of accounting is used in the majority of companies. By this method, you record revenues and expenses as soon as you incur them, even if the money hasn’t arrived in your account yet or the bill has not been paid. Any business that carries inventory, records bills in advance of paying them in an accounts payable account or makes sales on credit which results in an account receivable, generally should use accrual accounting.

The difference between the two categories is your profit or loss for that period. Income statements display only the activity for the selected period; the ending balance from the previous accounting period does not carry forward to the next. It includes the assets your company owns, such as equipment, automobiles, cash and inventory, and the company’s liabilities, or money that you owe. Your balance sheet captures the information as of the date you choose to print the report.

In other words, you cannot record your income using the cash method and record expenses with the accrual method. It’s best to get advice from a tax accountant if you fall into this category. Accrual accounting is based on the idea of matching revenueswith expenses. In business, many times these occur simultaneously, but the cash transaction is not always completed immediately.