T account

Since your company did not yet pay its employees, the Cash account is not credited, instead, the credit is recorded in the liability account Wages Payable. A credit to a liability account increases its credit balance.

How to Use Excel as a General Accounting Ledger

T accounts can also include cash accounts, expense accounts, revenue accounts, and more. Thus, accounts payable is credited when goods/services are purchased on credit because the liability increases.

On the other hand, when a company makes a payment for items purchased on credit, this results in a debit to accounts payable (decrease). Expenses normally have debit balances that are increased with a debit entry. Since expenses are usually increasing, think “debit” when expenses are incurred.

T- Account Recording

Whenever an accounting transaction is created, at least two accounts are always impacted, with a debit entry being recorded against one account and a credit entry being recorded against the other account. There is no upper limit to the number of accounts involved in a transaction – but the minimum is no less than two accounts. Thus, the use of debits and credits in a two-column transaction recording format is the most essential of all controls over accounting accuracy. We now offer eight Certificates of Achievement for Introductory Accounting and Bookkeeping.

Debits and credits are the basis of double-entry accounting systems. If you don’t understand how they work, it is very difficult to make entries into an organization’s general ledger.

Is T account same as general ledger?

Key Takeaways. A T-account is an informal term for a set of financial records that use double-entry bookkeeping. It is called a T-account because the bookkeeping entries are laid out in a way that resembles a T-shape. The account title appears just above the T.

This means that a business that receives cash, for example, will debit the asset account, but will credit the account if it pays out cash. The credits and debits are recorded in ageneral ledger, where all account balances must match.

On the statement of retained earnings, we reported the ending balance of retained earnings to be $15,190. We need to do the closing entries to make them match and zero out the temporary accounts. As it can be noted that all the payables account has been cleared to 0 since they were paid out. A simple journal entry is an accounting entry in which just one account is debited and one is credited. Many entries are much more complex; for example, a payroll entry may involve several dozen accounts.

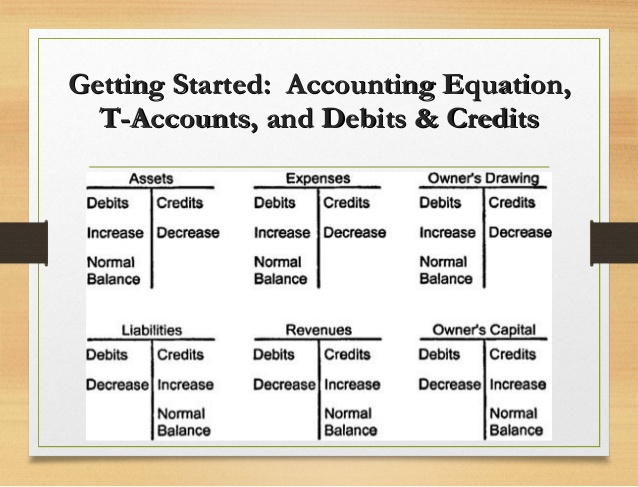

Therefore, asset, expense, and owner’s drawing accounts normally have debit balances. Liability, revenue, and owner’s capital accounts normally have credit balances. To determine the correct entry, identify the accounts affected by a transaction, which category each account falls into, and whether the transaction increases or decreases the account’s balance. As noted earlier, expenses are almost always debited, so we debit Wages Expense, increasing its account balance.

Financial History: The Evolution of Accounting

The certificates include Debits and Credits, Adjusting Entries, Financial Statements, Balance Sheet, Income Statement, Cash Flow Statement, Working Capital and Liquidity, and Payroll Accounting. Since cash was paid out, the asset account Cash is credited and another account needs to be debited.

Making accounting journal entries is how accounting transactions are recorded. There’s a particular way to make an accounting journal entry when recording both debits and credits. In an accounting journal, debits and credits are always going to be in adjacent columns on a page.

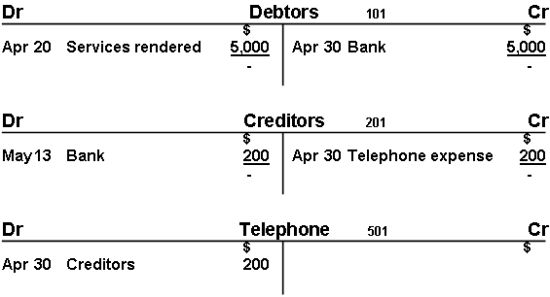

(We credit expenses only to reduce them, adjust them, or to close the expense accounts.) Examples of expense accounts include Salaries Expense, Wages Expense, Rent Expense, Supplies Expense, and Interest Expense. The bottom set of T accounts in the example show that, a few days later, the company pays the rent invoice.

- The major components of thebalance sheet—assets, liabilitiesand shareholders’ equity (SE)—can be reflected in a T-account after any financial transaction occurs.

- For different accounts, debits and credits may translate to increases or decreases, but the debit side must always lie to the left of the T outline and the credit entries must be recorded on the right side.

- A general ledger is a record of all of a company’s accounts and their associated transactions and balances.

The visual appearance of the ledger journal of individual accounts resembles a T-shape, hence why a ledger account is also called a T-account. Temporary – revenues, expenses, dividends (or withdrawals) account. These account balances do not roll over into the next period after closing. The closing process reduces revenue, expense, and dividends account balances (temporary accounts) to zero so they are ready to receive data for the next accounting period.

Cash is credited because the cash is an asset account that decreased because you use the cash to pay the bill. In finance and accounting, accounts payable can serve as either a credit or a debit. Because accounts payable is a liability account, it should have a credit balance. The credit balance indicates the amount that a company owes to its vendors.

What is a T-Account?

A debit is an accounting entry that results in either an increase in assets or a decrease in liabilities on a company’s balance sheet. In fundamental accounting, debits are balanced by credits, which operate in the exact opposite direction. The matching principle in accrual accounting states that all expenses must match with revenues generated during the period. The T-account guides accountants on what to enter in a ledger to get an adjusting balance so that revenues equal expenses. The debit entry of an asset account translates to an increase to the account, while the right side of the asset T-account represents a decrease to the account.

A general ledger is a record of all of a company’s accounts and their associated transactions and balances. Revenue, expense and dividend accounts are temporary accounts because they hold a balance for only one accounting period. Permanent accounts, such as assets, in comparison, hold a balance over multiple periods. Accountants record increases in asset, expense, and owner’s drawing accounts on the debit side, and they record increases in liability, revenue, and owner’s capital accounts on the credit side. An account’s assigned normal balance is on the side where increases go because the increases in any account are usually greater than the decreases.

For the revenue accounts, debit entries decrease the account, while a credit record increases the account. On the other hand, a debit increases an expense account, and a credit decreases it. Accounts are usually listed in order of their appearance in the financial statements, starting with the balance sheet and continuing with the income statement. Thus, the chart of accounts begins with cash, proceeds through liabilities and shareholders’ equity, and then continues with accounts for revenues and then expenses. The exact configuration of the chart of accounts will be based on the needs of the individual business.

This results in the elimination of the accounts payable liability with a debit to that account, as well as a credit to the cash (asset) account, which decreases the balance in that account. A T-account is an informal term for a set of financial records that uses double-entry bookkeeping. The term describes the appearance of the bookkeeping entries. The title of the account is then entered just above the top horizontal line, while underneath debits are listed on the left and credits are recorded on the right, separated by the vertical line of the letter T.

Whenever cash is received, the asset account Cash is debited and another account will need to be credited. Since the service was performed at the same time as the cash was received, the revenue account Service Revenues is credited, thus increasing its account balance. Revenues and gains are recorded in accounts such as Sales, Service Revenues, Interest Revenues (or Interest Income), and Gain on Sale of Assets. These accounts normally have credit balances that are increased with a credit entry. T-accounts can also be used to record changes to theincome statement, where accounts can be set up for revenues (profits) and expenses (losses) of a firm.

The use of simple journal entries is encouraged as a best practice, since it is easier to understand the entry. You debit the inventory account because it is an asset account that increases in this transaction. Accounts payable is credited to a liability account that increases because of the inventory was purchased on credit. When you pay the bill, you would debit accounts payable because you made the payment.

T accounts, refer to an account such as accounts payable, written in the visual representation of a “T”. For that account, each transaction is recorded as either a debit or a credit. The information can then be transferred to a journal from the T account.

For different accounts, debits and credits may translate to increases or decreases, but the debit side must always lie to the left of the T outline and the credit entries must be recorded on the right side. The major components of thebalance sheet—assets, liabilitiesand shareholders’ equity (SE)—can be reflected in a T-account after any financial transaction occurs.

Debits will be on the left and Credits will be on the right. Entries are always recorded in the relevant column for the transaction that is being entered.

Because the rent payment will be used up in the current period (the month of June) it is considered to be an expense, and Rent Expense is debited. If the payment was made on June 1 for a future month (for example, July) the debit would go to the asset account Prepaid Rent.