For perpetuities, however, there are an infinite number of periods, so we need a formula to find the PV. The formula for calculating the PV is the size of each payment divided by the interest rate. The PV for both annuities -due and ordinary annuities can be calculated using the size of the payments, the interest rate, and number of periods. For an ordinary annuity, however, the payments occur at the end of the period. This means the first payment is one period after the start of the annuity, and the last one occurs right at the end.

Another way to think of it is how much an annuity due would be worth when payments are complete in the future, brought to the present. The initial payment earns interest at the periodic rate (r) over a number of payment periods (n). PVIFA is also used in the formula to calculate the present value of an annuity.

An annuity due arises when each payment is due at the beginning of a period; it is an ordinary annuity when the payment is due at the end of a period. A common example of an annuity due is a rent payment that is scheduled to be paid at the beginning of a rental period. The Present Value of Annuity table Calculator is used to calculate the present value of an ordinary annuity, which is the current value of a stream of equal payments made at regular intervals over a specified period of time.

It is adjusted for risk based on the duration of the annuity payments and the investment vehicle utilized. Higher interest rates result in lower net present value calculations.

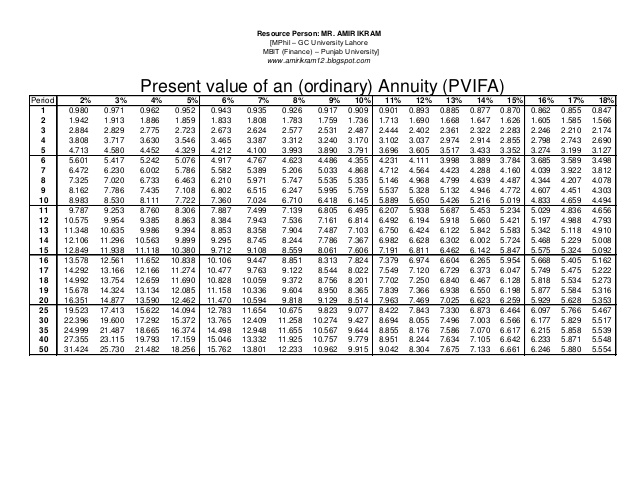

Calculate the present value interest factor of an annuity (PVIFA) and create a table of PVIFA values. Create a printable compound interest table for the present value of an ordinary annuity or present value of an annuity due for payments of $1. The present value interest factor of an annuity is useful when determining whether to take a lump-sum payment now or accept an annuity payment in future periods. Using estimated rates of return, you can compare the value of the annuity payments to the lump sum. The present value interest factor may only be calculated if the annuity payments are for a predetermined amount spanning a predetermined range of time.

There are different FV calculations for annuities due and ordinary annuities because of when the first and last payments occur. Valuation of life annuities may be performed by calculating the actuarial present value of the future life contingent payments.

It uses a payment amount, number of payments, and rate of return to calculate the value of the payments in today’s dollars. They can arise in loans, retirement plans, leases, insurance settlements, tax-related calculations, and so forth.

This is because the value of $1 today is diminished if high returns are anticipated in the future. There are some formulas to make calculating the FV of an annuity easier. The present value of an annuity due (PVAD) is calculating the value at the end of the number of periods given, using the current value of money.

Sometimes, one may be curious to learn how much a recurring stream of payments will grow to after a number of periods. An annuity due is an annuity where the payments are made at the beginning of each time period; for an ordinary annuity, payments are made at the end of the time period. The formula for the present value of an annuity due, sometimes referred to as an immediate annuity, is used to calculate a series of periodic payments, or cash flows, that start immediately. An annuity is a series of payments that occur over time at the same intervals and in the same amounts.

The fact that the value of the annuity-due is greater makes sense because all the payments are being shifted back (closer to the start) by one period. Moving the payments back means there is an additional period available for compounding. Note the under the annuity due the first payment compounds for 3 periods while under the ordinary annuity it compounds for only 2 periods. Likewise for the second and third payments; they all have an additional compounding period under the annuity due. Note also that the above formula implies that both the PV and the FVof an annuity due will be greater than their comparable ordinary annuity values.

Calculate the present value interest factor of an annuity (PVIFA) and create a table of PVIFA values.

Create a printable compound interest table for the present value of an ordinary annuity or present value of an annuity due for payments of $1.

If annuity payments are due at the beginning of the period, the payments are referred to as an annuity due. To calculate the present value interest factor of an annuity due, take the calculation of the present value interest factor and multiply it by (1+r), with the variable being the discount rate. The discount rate used in the present value interest factor calculation approximates the expected rate of return for future periods.

Understanding the Present Value of an Annuity

The moral is to save early and save often (and live long!) to take advantage of the power of compound interest. Here we use the same values as the PV of an annuity problem above to calculate PVwhen the payments are made at the end of the period (ordinary annuity) and at the beginning of the period (annuity due). Both annuities-due and ordinary annuities have a finite number of payments, so it is possible, though cumbersome, to find the PV for each period.

Present Value Annuity Due Tables

The first and last payments of an annuity due both occur one period before they would in an ordinary annuity, so they have different values in the future. The present value (PV) of an annuity due is the value today of a series of payments in the future.

Calculating Present and Future Value of Annuities

These annuities are called ordinary annuities (also known as annuities in arrears). The next graphic portrays a 5-year, 10%, ordinary annuity involving level payments of $5,000 each. Notice the similarity to the preceding graphic – except that each year’s payment is shifted to the end of the year. This means each payment will accumulate interest for one less year, and the final payment will accumulate no interest! Be sure to note the striking difference between the accumulated total under an annuity due versus and ordinary annuity ($33,578 vs. $30,526).

Accounting Ratios

Once you have the PVIFA factor value, you can multiply it by the periodic payment amount to find the current present value of the annuity. The preceding annuity table is useful as a quick reference, but only provides values for discrete time periods and interest rates that may not exactly correspond to a real-world scenario. Accordingly, use the annuity formula in an electronic spreadsheet to more precisely calculate the correct amount of the present value of an annuity due. This problem calculates the difference between the present value (PV) of an ordinary annuity and an annuity due. The timing difference in the payments is illustrated in an Excel schedule.

This is illustrated graphically in the section that follows, “Visual Comparison of Cash Flows.” It can also be clearly seen in the discount and accumulation schedules constructed in the “Excel” section. The Present Value (PV) of an annuity can be found by calculating the PV of each individual payment and then summing them up. As in the case of finding the Future Value (FV) of an annuity, it is important to note when each payment occurs. Annuities-due have payments at the beginning of each period, and ordinary annuities have them at the end.