percentage-of-sales method

In other words, they represent the earnings after dividends have been deducted. The process for determining the addition to retained earnings as a result of the increased sales is calculated by using the forecasted net income and the percentage of earnings that are kept in the business. The standard figure used in the analysis of a common size income statement is total sales revenue. The common size percentages are calculated to show each line item as a percentage of the standard figure or revenue. The percentage-of-sales method is used to develop a budgeted set of financial statements.

What is the Percentage of Sales Method?

He would like to complete his financial forecast for next year and is wondering if he could use the percentage of sales method. A common size income statement is an income statement whereby each line item is expressed as a percentage of revenue or sales. Common size financial statements help to analyze and compare a company’s performance over several periods with varying sales figures. The common size percentages can be subsequently compared to those of competitors to determine how the company is performing relative to the industry. Now that you’ve calculated your year-end average A/R balance, you can use this to calculate your company’s ACP and understand the relationship between these figures.

To calculate year-end accounts receivable, you don’t need to estimate your company’s ACP. Take the starting A/R balance at the beginning of the year, plus the ending A/R balance at the end of each month. Add these and divide the total by 13 to get the average A/R balance for the year; use this for your year-end figure. Using the balance each month as part of your averaging calculation allows you to factor in fluctuations in A/R due to busier sales during certain months such as the Christmas holiday season. Companies want to know how soon they’ll get their money after making a credit sale to a customer.

Explanation of percentage-of-sales approach

Under the percentage of accounts receivable method, a company derives an estimate for the value of bad debts under the allowance method is to calculate bad debts as a percentage of the account receivable balance. Once all of the amounts have been determined, Mr. Weaver can put this information into his forecasted, or pro-forma, income statement and balance sheet. The income statement would show the current year and forecast year amounts for sales, cost of goods sold, net income, dividends and addition to retained earnings. The balance sheet would show the current year and forecast year amounts for assets as well as liabilities and owner’s equity.

Now let’s take a look at how to calculate changes in retained earnings. Retained earnings represent the amount of earnings that have been retained in the business since the company started operating.

Once the sales growth has been determined, the company can prepare pro-forma, or forecasted financial statements. For most businesses, especially in retail, owners and managers like to know the percentages of increase and decrease for just about everything, from sales to salaries.

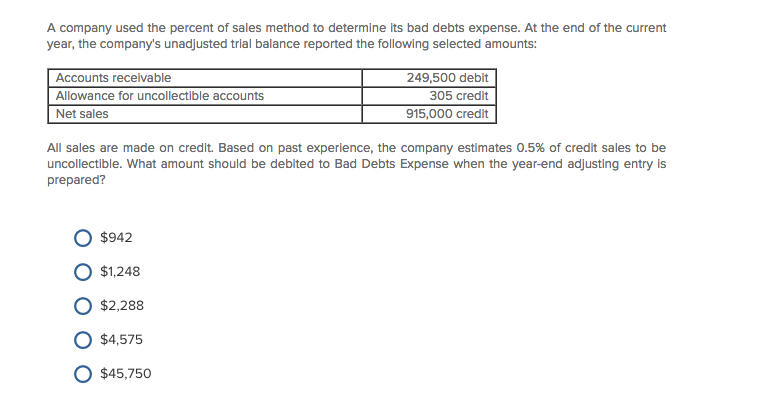

Use the following formulas to calculate the percentages of increase and decrease in your company. This approach does not consider the balance in the allowance for doubtful accounts because such balance is not used in the calculation of bad debt expense.

The process for determining the addition to retained earnings that will result from an increase in sales is calculated by multiplying the current retained earnings balance by the forecasted net income. Retained earnings represent the earnings retained by the business and not distributed to its shareholders since the business started operating.

procedure used to set advertising budgets, based on a predetermined percentage of past sales or a forecast of future sales. This method of budget allocation is popular with advertisers because of its simplicity and its ability to relate advertising expenditures directly to sales. Management usually determines the budget’s percentage figure, which is based on the industry average or the company’s historical or previous year’s advertising spending.

Percentage of Sales Method

Analysts study the income statement for insights into a company’s historic growth and profitability. The balance sheet provides relevant information about a company’s liquidity and financial strength.

As a result, the financial statement user can more easily compare the financial performance to the company’s peers. A common size income statement is an income statement in which each line item is expressed as a percentage of the value of revenue or sales. It is used for vertical analysis, in which each line item in a financial statement is represented as a percentage of a base figure within the statement.

- The percentage of sales method is a financial forecasting tool that helps determine the impact of a forecasted change in sales volume on accounts that vary with a change in sales.

For example, a firm expecting to do $50 million worth of business next year and choosing to allocate 5% of their sales to the advertising budget, would propose a $2.5 million advertising budget. A similar decision may be based on market share, with $2 million being allocated for every share point a brand holds. Many advertisers, however, shun this method because it is based on the theory that advertising results from sales, while the converse is true, that is, that sales result from advertising. In other words, advertisers feel that advertising communicates to prospeactive buyers the features and benefits of a product that are necessary to generate sales. In addition, the method does not recognize that as conditions change, advertising expenditures should change with them.

Time-Intensive Completion – While there are various methods of sales forecasting, the two broad approaches include manual and data-driven processes. Within a traditional manual system, salespeople prepare their own forecasts by reviewing current accounts and overall projected sales. In more data-driven processes, a company often has marketing, IT and sales staff involved in building a system to collect and interpret data. Analysts common size an income statement by dividing each line item (for example, gross profit, operating income and sales and marketing expenses) by the top line (sales).

The common size percentages help to highlight any consistency in the numbers over time–whether those trends are positive or negative. Large changes in the percentage of revenue as compared to the various expense categories over a given period could be a sign that the business model, sales performance, or manufacturing costs are changing.

What does percent of sales mean?

The percentage of sales method is used to calculate how much financing is needed to increase sales. The method allows for the creation of a balance sheet and an income statement. The equation to calculate the forecasted net income is: Forecasted Sales = Current Sales x (1 + Growth Rate/100).

Common size income statements with easy-to-read percentages allow for more consistent and comparable financial statement analysis over time and between competitors. Generally accepted accounting principles (GAAP) are based on consistency and comparability of financial statements. A common size income statement makes it easier to see what’s driving a company’s profits. The common size percentages also help to show how each line item or component affects the financial position of the company.

How do you calculate the percentage of sales?

The percentage of sales method is used to calculate how much financing is needed to increase sales. The method allows for the creation of a balance sheet and an income statement. The equation to calculate the forecasted net income is: Forecasted Sales = Current Sales x (1 + Growth Rate/100).

To calculate the ACP, first need to estimate the company’s full year’s sales amount made to customers, but only those made on credit terms. For a budget or forecast, you could use the previous year’s credit sales numbers as a starting point and then factor in some growth to arrive at an estimate for the current or upcoming year forecast. The ability to come up with an estimate for year-end accounts receivable (A/R) helps companies assemble budgets or forecast financial statements. Accounts receivable represents the credit sales a company makes to its customers that have been billed but not yet paid by the customer. Getting a feel for how much customers could owe the company on credit at the end of the year helps a company project sales, expenses and cash flow needs, among other financial metrics.

That is because the bad debt expense was recognized when the company recorded the estimated uncollectable amount in the period of respective sales recognition. So, bad debt expenses are only recorded when the company posts the estimates of uncollectable balances due from customers, but not when bad debts are actually written off. This approach fully satisfies the matching principle because revenues and related bad debt expenses are recorded in the same period. Keep in mind that the financial statements contain other accounts that do not vary with sales, such as notes payable, long-term debt, and common shares. The changes in these accounts are determined by which method the company chooses to finance its growth, debt, or equity.

Percentage of accounts receivable method – Accounting

Each historical expense is converted into a percentage of net sales, and these percentages are then applied to the forecasted sales level in the budget period. For example, if the historical cost of goods sold as a percentage of sales has been 42%, then the same percentage is applied to the forecasted sales level. The approach can also be used to forecast some balance sheet items, such as accounts receivable, accounts payable, and inventory. Percentage of Sales method is a forecasting approach which is based on the assumption that the balance sheet and income statement accounts would vary with sales. Based on previous sales, new budgets for ad commercials are decided.

Definition: Percentage of Sales method

The forecast, or pro-forma, balance sheet will not balance initially; that is, total assets will not equal total liabilities and owner’s equity. The difference represents the amount of external financing that must be obtained to finance the increase in sales. The percentage of sales method is a financial forecasting method that businesses use to predict their sales growth on an annual basis. They use this information to predict the amount of financing they need to acquire to help accomplish their goal.

The percentage of sales method is a financial forecasting tool that helps determine the impact of a forecasted change in sales volume on accounts that vary with a change in sales. Once changes have been determined, the company can prepare a forecast balance sheet, which shows assets, liabilities and owner’s equity, and an income statement, which shows revenue, expenses and net income. By analyzing how a company’s financial results have changed over time, common size financial statements help investors spot trends that a standard financial statement may not uncover.

The common size income statement for Company A shows operating profits are 25% of sales (25/100). The same calculation for Company B shows operating profits at 75% of sales (15/20). The common size statements make it easy to see that Company B is proportionally more profitable and better at controlling expenses. The two financial statements that analysts common size most often are the income statement and the balance sheet.

Once a sale is made but before the customers send in a check for payment, the company accounts for unpaid customer balances in its financial statements in the A/R asset account on the balance sheet. However, a look at the common size financial statement of the two businesses, which restates each company’s figures as a percent of sales, reveals Company B is actually more profitable.