Non-GAAP Earnings Definition

What are Generally Accepted Accounting Principles?

International Financial Reporting Standards (IFRS) – as the name implies – is an international standard developed by the International Accounting Standards Board (IASB). Generally Accepted Accounting Principles (GAAP) is only used in the United States. Generally accepted accounting principles (GAAP) are a common set of accounting rules and standards that dictate how financial statements are prepared. Public companies, nonprofit organizations, and government entities are required to prepare financial statements in accordance with GAAP. These guidelines were developed over time by the Financial Accounting Standards Board (FASB), and the American Institute of Certified Public Accountants (AICPA).

Generally accepted accounting principles (GAAP) are controlled by the Financial Accounting Standards Board (FASB), a nongovernmental entity. The FASB creates specific guidelines that company accountants should follow when compiling and reporting information for financial statements or auditing purposes. GAAP is not law, and there is nothing illegal about violations of its rules unless those violations happen to coincide with other laws. Generally accepted accounting principles, or GAAP, are a set of rules that encompass the details, complexities, and legalities of business and corporate accounting.

Per generally accepted accounting principles (GAAP), companies are responsible for providing reports on their cash flows, profit-making operations, and overall financial conditions. GAAP dictates that business organizations use the same accounting principles from one reporting period to the next, which promotes consistency and the usability of financial statements. For instance, switching from the first-in, first-out inventory accounting method to the last-in, first-out method without notice has the potential to confuse the users of financial statements. Similarly, consistent revenue recognition and bad debt accounting methods influence internal decision-makers and investors.

IFRS is designed to provide a global framework for how public companies prepare and disclose their financial statements. Adopting a single set of world-wide standards simplifies accounting procedures for international countries and provides investors and auditors with a cohesive view of finances. IFRS provides general guidance for the preparation of financial statements, rather than rules for industry-specific reporting. This is one of the chief examples of private businesses regulating themselves to help promote credibility within an industry.

By being more principles-based, IFRS, arguably, represents and captures the economics of a transaction better than GAAP. Some of the differences between the two accounting frameworks are highlighted below. The first committee was called the Committee on Accounting Procedures, or CAP for short. Several years later, CAP was replaced with the Financial Accounting Standards Board (FASB).

The first body to assume this task was the Committee on Accounting Procedure, which was replaced in 1959 by the Accounting Principles Board. In 1973, the Accounting Principles Board was replaced after much criticism by the FASB. The Statement of Financial Accounting Concepts is issued by the Financial Accounting Standards Board (FASB) and covers financial reporting concepts.

What is GAAP?

Where is GAAP used?

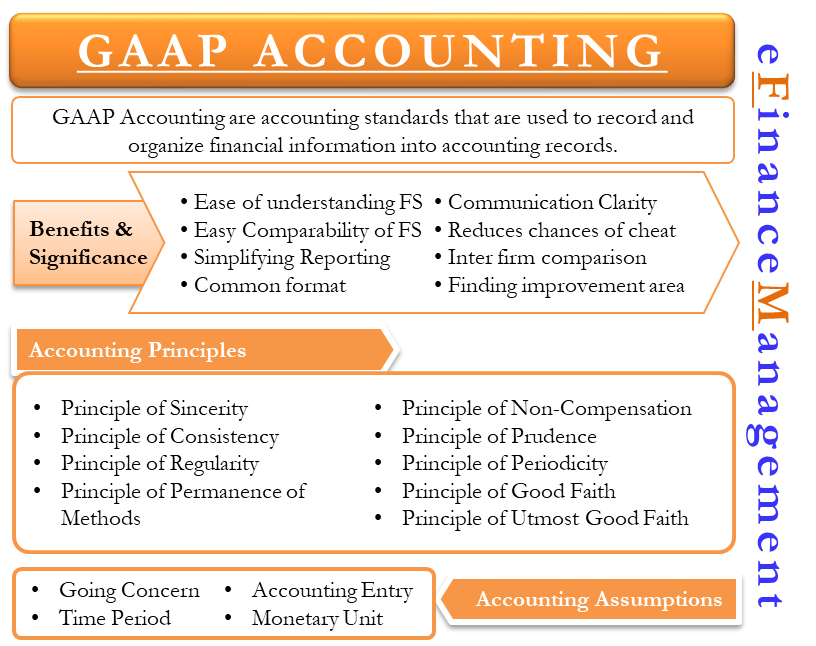

GAAP is a combination of authoritative standards (set by policy boards) and the commonly accepted ways of recording and reporting accounting information. GAAP aims to improve the clarity, consistency, and comparability of the communication of financial information.

GAAP earnings are used to standardize the financial reporting of publicly traded companies. There is no universal GAAP standard and the specifics vary from one geographic location or industry to another. In the United States, the Securities and Exchange Commission (SEC) mandates that financial reports adhere to GAAP requirements. The Financial Accounting Standards Board (FASB) stipulates GAAP overall and the Governmental Accounting Standards Board (GASB) stipulates GAAP for state and local government.

For example, without GAAP, one firm might report the income from future year contracts in its current year, vastly inflating its profits. Another company might not, making it look worse than its competitor even though it might be better. GAAP is a common set of accounting principles, standards, and procedures that public companies in the U.S. must follow when they compile their financial statements.

A third important relation of mine is the International Accounting Standards Board (IASB). The IASB is the body that sets the global standards for international accounting. The members of this board are from diverse nationalities, but each has the common interest of setting globally accepted accounting principles.

The Financial Accounting Standards Board (FASB) uses GAAP as the foundation for its comprehensive set of approved accounting methods and practices. Generally Accepted Accounting Principles (GAAP) refers to a widely accepted set of rules, standards, conventions, and procedures for reporting financial info. In USA this set of rules has been established by the Financial Accounting Standards Board (FASB). GAAP is an amalgamation of authoritative standards and the usually accepted methods of recording and reporting info on accounting.

These standards are used in over 120 countries, including those in the European Union (EU). However, the FASB and the IASB continue to work together to issue similar regulations on certain topics as accounting issues arise. For example, in 2016 the FASB and the IASB jointly announced new revenue recognition standards. The International Financial Reporting Standards (IFRS), the accounting standard used in more than 110 countries, has some key differences from the United States’ Generally Accepted Accounting Principles (GAAP). At the conceptual level, IFRS is considered more of a principles-based accounting standard in contrast to GAAP, which is considered more rules-based.

What’s the Difference Between IFRS and GAAP?

- GAAP is a combination of authoritative standards (set by policy boards) and the commonly accepted ways of recording and reporting accounting information.

- Generally accepted accounting principles (GAAP) refer to a common set of accounting principles, standards, and procedures issued by the Financial Accounting Standards Board (FASB).

GAAP is codified into the Accounting Standards Codification (ASC), which is available online and (more legibly) in printed form. The international alternative to GAAP is the International Financial Reporting Standards (IFRS), set by the International Accounting Standards Board (IASB).

Generally accepted accounting principles (GAAP) refer to a common set of accounting principles, standards, and procedures issued by the Financial Accounting Standards Board (FASB). Public companies in the United States must follow GAAP when their accountants compile their financial statements. GAAP is a combination of authoritative standards (set by policy boards) and the commonly accepted ways of recording and reporting accounting information. GAAP aims to improve the clarity, consistency, and comparability of the communication of financial information. We live in an increasingly global economy, so it’s important for business owners and accounting professionals to be aware of the differences between the two predominant accounting methods used around the world.

Non-GAAP earnings are an alternative accounting method used to measure the earnings of a company. Many companies report non-GAAP earnings in addition to their earnings based on Generally Accepted Accounting Principles (GAAP). These pro forma figures, which exclude “one-time” transactions, can sometimes provide a more accurate measure of a company’s financial performance from direct business operations.

Generally accepted accounting principles, or GAAP, are the rules used in the U. Their objective is to make the accounting process uniform so financial reports are comparable from one company to another.

FASB is the current committee that reviews and sets the standards for financial reporting in the United States. In the international business world, it is the International Accounting Standards Board (IASB) that sets the standards that foreign countries abide by for financial reporting. In the United States, publicly traded companies are regulated by the Securities and Exchange Commission (SEC). Since its inception, the SEC has delegated its accounting and financial reporting standards responsibilities to private-sector groups.

By observing GAAP and the consistency principle, businesses make it easier for stakeholders to evaluate financial data. GAAP is used primarily by businesses reporting their financial results in the United States. International Financial Reporting Standards, or IFRS, is the accounting framework used in most other countries. IFRS focuses more on general principles than GAAP, which makes the IFRS body of work much smaller, cleaner, and easier to understand than GAAP. Since IFRS is still being constructed, GAAP is considered to be the more comprehensive accounting framework.

The Difference Between Principles-Based and Rules-Based Accounting

To understand non-GAAP earnings, it’s important to understand GAAP earnings. GAAP earnings are a common set of standards accepted and used by companies and their accounting departments.

The Financial Accounting Standards Board (FASB) is responsible for generating rulings under GAAP, and the SEC enforces those standards on the financial community. In the late 1930s, the AIA created a subcommittee to specifically create the GAAP principles.

It was called the Committee on Accounting Procedure, or CAP, and comprised 18 accountants and three accounting professors. In 1973, the SEC decided to replace CAP with the Financial Accounting Standards Board (FASB), which is still in place today. In the United States, the most common accounting framework for the preparation of financial statements is Generally Accepted Accounting Principles (GAAP). This framework provides a common set of rules in order for readers to properly understand and interpret financial results. Many countries around the world have adopted the International Financial Reporting Standards (IFRS).

When and Why Were GAAP First Established?

Managers and investors would struggle to interpret financial statements without U.S. GAAP provides a standardized methodology for recording transactions and events that impact the financial position of a company. Small-business leaders can use this set of accounting standards to track and improve financial performance. In the United States, the Financial Accounting Standards Board (FASB) issues Generally Accepted Accounting Principles (GAAP).

GAAP is not the international accounting standard; this is a developing challenge as businesses become more globalized. The International Financial Reporting Standards(IFRS) is the most common set of principles outside the United States and is used in places such as the European Union, Australia, Canada, Japan, India, and Singapore. To reduce tension between these two major systems, the FASB and International Accounting Standards Board are working to converge standards. The International Accounting Standards Board (IASB) issues International Financial Reporting Standards (IFRS).

According to Stephen Zeff in The CPA Journal, GAAP terminology was first used in 1936 by the American Institute of Accountants (AIA). Federal endorsement of GAAP began with legislation like the Securities Act of 1933and the Securities Exchange Act of 1934, laws enforced by the U.S. Today, the Financial Accounting Standards Board (FASB), an independent authority, continually monitors and updates GAAP. GAAP is derived from the pronouncements of a series of government-sponsored accounting entities, of which the Financial Accounting Standards Board (FASB) is the latest.

Comparability is the ability for financial statement users to review multiple companies’ financials side by side with the guarantee that accounting principles have been followed to the same set of standards. Accounting information is not absolute or concrete, and standards such as GAAP are developed to minimize the negative effects of inconsistent data. Without GAAP, comparing financial statements of companies would be extremely difficult, even within the same industry, making an apples-to-apples comparison hard.