Net realizable value

Two of the largest assets that a company may list on a balance sheet are accounts receivable and inventory. The lower of cost or market method lets companies record losses by writing down the value of the affected inventory items. The amount by which the inventory item was written down is recorded under cost of goods sold on the balance sheet.

Let’s say out of it, Walmart is going to sell some part of the inventory to another company for $4 Bn for offloading purposes. For that Walmart needs to calculate the cost associated with the Sale of Inventory. Let’s say transportation cost is $500 Mn and legal and registration charges are $100 Mn.

Through arbitrage, a trader can profit from a price imbalance by simultaneously purchasing and selling an asset. The trade exploits the price differences among identical or similar financial instruments on different markets or in different forms. We often find the term net realizable value being associated with the current assets accounts receivable and inventory.

NRV for inventory is the estimated selling price, or fair value, of the inventory once it has all been manufactured into finish products, minus the costs to finish and sell the goods. Net Realizable Value (NRV) pertains to two different aspects of valuing business assets. Accounts receivable are amounts that a business is owed by its customers for goods or services provided on credit. The NRV of this asset is how much the business can expect to collect on the amount due.

The NPV in this case is the amount owed minus the allowance for doubtful accounts. The allowance for doubtful accounts is a balance maintained to offset accounts receivable and is an estimate of how much of accounts receivable will not be collected at any given time. The fair value of an asset is the amount of money you would get if you sold the good in the current market. Fair value assumes that the good is sold by one party to an unaffiliated buyer, and that the seller is not under any duress or pressure to raise cash. This assumption is important, because it presumes that in those circumstances the seller would be able to get the highest price possible for his good.

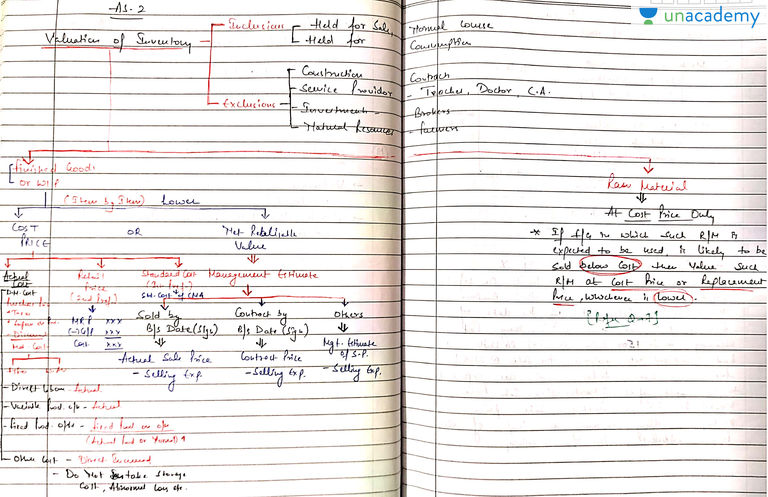

Net realizable value (NRV) is the value of an asset which can be realized when that asset is sold. It is also termed as cash Realizable value since it is the cash amount which one gets for the asset. All the related cost like disposal cost, transportation cost etc. should be subtracted while calculating a net realizable value. So during inventory valuation, NRV is the price cap for the asset if we use a market method of accounting. In that method, inventory is valued at either historical cost or market value, whichever is lower.

Net Realizable Value Formula

Obviously, these measurements can be somewhat subjective, and may require the exercise of judgment in their determination. However, at the end of the accounting year the inventory can be sold for only $14,000 after it spends $2,000 for packaging, sales commissions, and shipping.

While these two assets are initially recorded at cost, there are occasions when the company will collect less than the cost. When that occurs, the company must report the lower of 1) cost, or 2) the net realizable value.

Inventory

The lower of cost or market (LCM) method relies on the fact that when investors value a company’s inventory, those assets shall be recorded on the balance sheet at either the market value or the historical cost. Net realizable value (NRV) is a conservative method for valuing assets because it estimates the true amount the seller would receive net of costs if the asset were to be sold.

NRV is the total amount which a company can expect while selling its assets. It is used by businesses to value their inventory and it uses a conservative approach while valuing the inventory. Analysts, who are analyzing companies financial can also check if the company is valuing its assets following proper accounting method. NRV helps businesses to assess the correct value of inventory and see if there is any negative impact on valuation.

How do you calculate net realizable value?

Net realizable value (NRV) is the cash amount that a company expects to receive. In the case of accounts receivable, net realizable value can also be expressed as the debit balance in the asset account Accounts Receivable minus the credit balance in the contra asset account Allowance for Uncollectible Accounts.

Understanding Net Realizable Value (NRV)

- Net realizable value (NRV) is the value of an asset which can be realized when that asset is sold.

- It is also termed as cash Realizable value since it is the cash amount which one gets for the asset.

Net realizable value, as discussed above can be calculated by deducting the selling cost from the expected market price of the asset and plays a key role in inventory valuation. Every business has to keep a close on its inventory and periodically access its value. The reason for that is there are several negative impacts like damage of inventory, obsolescence, spoilage etc. which can affect the inventory value in a negative way. So it is better for a business to write off those assets once for all rather than carrying those assets which can increase the losses in the future. This value is often shown on financial news networks and displayed online before the equity markets open for trading.

The deductions from the estimated selling price are any reasonably predictable costs of completing, transporting, and disposing of inventory. Net realizable value (NRV) is the value of an asset that can be realized upon the sale of the asset, less a reasonable estimate of the costs associated with the eventual sale or disposal of the asset. NRV is a common method used to evaluate an asset’s value for inventory accounting. NRV is a valuation method used in both Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS). The lower of cost or market method is a way to record the value of inventory which places an emphasis on not overstating the value of the assets.

Under this scenario, if the price at which the inventory may be sold dips below the net realizable value of the item, which consequently results in a loss, the LCM method can be employed to record the loss. Fair value is the sale price agreed upon by a willing buyer and seller. The fair value of a stock is determined by the market where the stock is traded. Fair value also represents the value of a company’s assets and liabilities when a subsidiary company’s financial statements are consolidated with a parent company. This video shows how to calculate the Net Realizable Value of inventory.

For insurance policies for property insurance, a contractual stipulation that the lost asset must be actually repaired or replaced before the replacement cost can be paid is common. This prevents overinsurance, which contributes to arson and insurance fraud.

The lower of cost or market (LCM) method states that when valuing a company’s inventory, it is recorded on the balance sheet at either the historical cost or the market value. Historical cost refers to the cost at which the inventory was purchased. NRV, in the context of inventory, is the estimated selling price in the normal course of business, less reasonably predictable costs of completion, disposal, and transportation.

Replacement cost policies emerged in the mid-20th century; prior to that concern about overinsurance restricted their availability. Inventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a company has accumulated. It is often deemed the most illiquid of all current assets – thus, it is excluded from the numerator in the quick ratio calculation. Walmart is a US-based retail supermarket chain-based company with around $500Bn of revenue as per the financial year 2018. Let’s say in the Financial year 2018, a market value of Inventory (which is also an asset) for Walmart is around $44 Bn.

The futures price may be different from the fair value due to the short-term influences of supply and demand for the futures contract. The fair value always refers to the front-month futures contract as opposed to a further out month contract. In the context of inventory, net realizable value or NRV is the expected selling price in the ordinary course of business minus the costs of completion, disposal, and transportation. The inventory of a manufacturer rarely consists of just completed products. Inventory will contain the raw materials to make the goods as well as products that are in the process of being made but are not completed.

Therefore, the net realizable value of the inventory is $12,000 (selling price of $14,000 minus $2,000 of costs to dispose of the goods). In that situation the inventory must be reported at the lower of 1) the cost of $15,000, or 2) the NRV of $12,000. In this situation, the inventory should be reported on the balance sheet at $12,000, and the income statement should report a loss of $3,000 due to the write-down of inventory. The lower of cost or market rule traditionally applies to companies whose products become obsolete.

This approach expects the businesses to value their inventory at a conservative value and avoid overstating it. Recently, the FASB issued an update to their code and standards that affect companies that use the average cost and FIFO methods of inventory accounting.

Companies that use these two methods of inventory accounting must now use the lower of cost or net realizable value method, which is more consistent with IFRS rules. The LCM method is part of the GAAP rules used in the U.S. and in international commerce. Almost all assets enter the accounting system with a value equal to acquisition cost. GAAP prescribes many different methods for adjusting asset values in subsequent reporting periods. The LCM method takes into account that the value of a good can fluctuate.

If we are not able to determine the market value, NRV can be used as a proxy for that. GAAP rules previously required accountants to use the lower of cost or market (LCM) method to value inventory on the balance sheet. If the market price of inventory fell to below the historical cost, the principle of conservatism required accountants to use the market price to value inventory. Market price was defined as the lower of either replacement cost or NRV.

Replacement cost is the actual cost to replace an item or structure at its pre-loss condition. This may not be the “market value” of the item, and is typically distinguished from the “actual cash value” payment which includes a deduction for depreciation.

Spotting Creative Accounting on the Balance Sheet

The Net Realizable Value of inventory needs to be determined before one can apply the lower of cost or market rule to value inventory. In the insurance industry, “replacement cost” or “replacement cost value” is one of several method of determining the value of an insured item.

Net realizable value is an important metric that is used in the lower cost or market method of accounting reporting. Under the market method reporting approach, the company’s inventory must be reported on the balance sheet at a lower value than either the historical cost or the market value. If the market value of the inventory is unknown, the net realizable value can be used as an approximation of the market value. Net realizable value is the estimated selling price of goods, minus the cost of their sale or disposal. It is used in the determination of the lower of cost or market for on-hand inventory items.