Journal Entry for Prepaid Insurance

You would initially debit the Prepaid Insurance account for $2,400 and credit the Cash account for $2,400. After one month, you will have used up one month of your insurance policy and only have 11 months remaining on the policy. Thus, you record an adjusting journal entry at the end of the first month by debit Insurance Expense for $200 and crediting the Prepaid Insurance account for $200. You would then make this same adjusting journal entry at the end of each month until the policy expires. The $1,500 balance in the asset account Prepaid Insurance is the preliminary balance.

This is usually done at the end of each accounting period through an adjusting entry. As time passes, you decrease the prepaid insurance account and record insurance expense. For example, let’s say your company pays $2,400 for a 1-year insurance policy upfront.

Therefore the balance in Accounts Receivable might be approximately the amount of one month’s sales, if the company allows customers to pay their invoices in 30 days. A common prepaid expense is the six-month insurance premium that is paid in advance for insurance coverage on a company’s vehicles. The amount paid is often recorded in the current asset account Prepaid Insurance. If the company issues monthly financial statements, its income statement will report Insurance Expense which is one-sixth of the six-month premium. The balance in the account Prepaid Insurance will be the amount that is still prepaid as of the date of the balance sheet.

A prepaid expense is a type of asset on the balance sheet that results from a business making advanced payments for goods or services to be received in the future. Prepaid expenses are initially recorded as assets, but their value is expensed over time onto the income statement.

The income statement account Supplies Expense has been increased by the $375 adjusting entry. It is assumed that the decrease in the supplies on hand means that the supplies have been used during the current accounting period.

Each month, an adjusting entry will be made to expense $10,000 (1/12 of the prepaid amount) to the income statement through a credit to prepaid insurance and a debit to insurance expense. In the twelfth month, the final $10,000 will be fully expensed and the prepaid account will be zero. If the premium were $1,200 per year, for instance, you would record the check for $1,200 as a credit to the cash account in your journal, decreasing the value of that account. Then you would enter a debit of $1,200 to the prepaid insurance asset account, increasing its value. Each month, you will need to move the used portion of the insurance payment to an expense account.

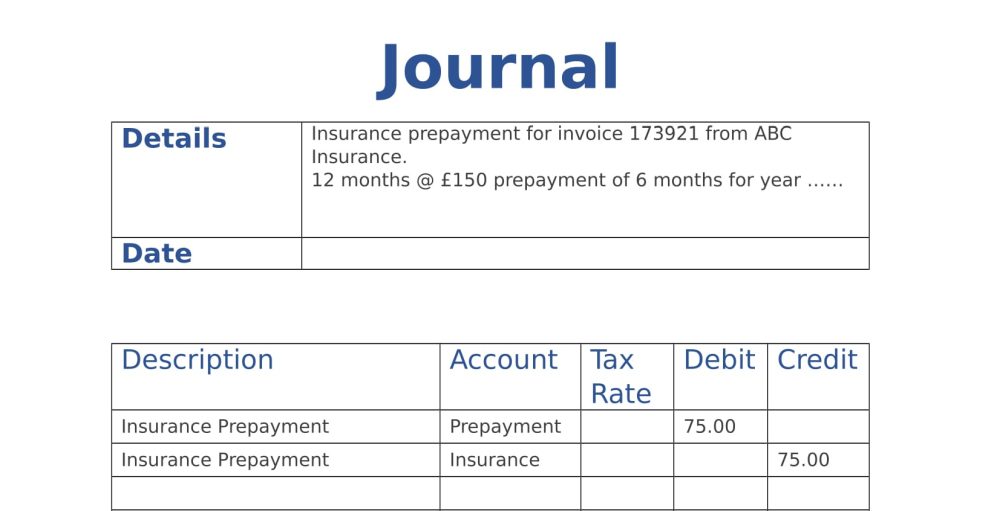

How do you record adjusting entry for prepaid insurance?

When the asset is charged to expense, the journal entry is to debit the insurance expense account and credit the prepaid insurance account. The initial entry is a debit of $12,000 to the prepaid insurance (asset) account, and a credit of $12,000 to the cash (asset) account.

The initial entry is a debit of $12,000 to the prepaid insurance (asset) account, and a credit of $12,000 to the cash (asset) account. In each successive month for the next twelve months, there should be a journal entry that debits the insurance expense account and credits the prepaid expenses (asset) account. Note that the ending balance in the asset Prepaid Insurance is now $600—the correct amount of insurance that has been paid in advance.

Notice that the ending balance in the asset Accounts Receivable is now $7,600—the correct amount that the company has a right to receive. The balance in Service Revenues will increase during the year as the account is credited whenever a sales invoice is prepared. The balance in Accounts Receivable also increases if the sale was on credit (as opposed to a cash sale). However, Accounts Receivable will decrease whenever a customer pays some of the amount owed to the company.

At the end of the month, before the books are closed for the month, make one double entry to the journal. If the premium were $1,200 per year, you would enter a credit of $100 to the prepaid insurance asset account, decreasing its value. Then you would enter a debit to the insurance expense account, increasing the value of the expenses.

- For example, assume ABC Company purchases insurance for the upcoming twelve month period.

- ABC Company will initially book the full $120,000 as a debit to prepaid insurance, an asset on the balance sheet, and a credit to cash.

Prepaid insurance

Unlike conventional expenses, the business will receive something of value from the prepaid expense over the course of several accounting periods. The initial journal entry for prepaid rent is a debit to prepaid rent and a credit to cash.

The correct amount is the amount that has been paid by the company for insurance coverage that will expire after the balance sheet date. Notice that the ending balance in the asset Supplies is now $725—the correct amount of supplies that the company actually has on hand.

prepaid insurance definition

How is prepaid insurance recorded?

A prepaid expense can be recorded initially as an expense or as a current asset. The current month’s insurance expense of $1,000 ($6,000/6 months) is reported on each month’s income statement. The unexpired amount of the prepaid insurance is reported on the balance sheet as of the last day of each month.

The income statement account Insurance Expense has been increased by the $900 adjusting entry. It is assumed that the decrease in the amount prepaid was the amount being used or expiring during the current accounting period. The balance in Insurance Expense starts with a zero balance each year and increases during the year as the account is debited. The balance at the end of the accounting year in the asset Prepaid Insurance will carry over to the next accounting year.

For example, assume ABC Company purchases insurance for the upcoming twelve month period. ABC Company will initially book the full $120,000 as a debit to prepaid insurance, an asset on the balance sheet, and a credit to cash.

Asset and Expense

Therefore the account Accumulated Depreciation – Equipment will need to have an ending balance of $9,000. The income statement account that is pertinent to this adjusting entry and which will be debited for $1,500 is Depreciation Expense – Equipment. As the amount of prepaid insurance expires, the expired portion is moved from the current asset account Prepaid Insurance to the income statement account Insurance Expense.

Is a prepaid expense recorded initially as an expense?

As each month passes, one rent payment is credited from the prepaid rent asset account, and a rent expense account is debited. This process is repeated as many times as necessary to recognize rent expense in the proper accounting period. The correct balance should be the cumulative amount of depreciation from the time that the equipment was acquired through the date of the balance sheet. A review indicates that as of December 31 the accumulated amount of depreciation should be $9,000.

These are both asset accounts and do not increase or decrease a company’s balance sheet. Recall that prepaid expenses are considered an asset because they provide future economic benefits to the company. For example, a business buys one year of general liability insurance in advance, for $12,000.

This reflects the depletion of the asset by the amount of one month’s insurance, and it correctly enters the expense on the income statement. Prepaid insurance is considered a business asset, and is listed as an asset account on the left side of the balance sheet. The payment of the insurance expense is similar to money in the bank, and the money will be withdrawn from the account as the insurance is “used up” each month or each accounting period. Prepaid insurance is usually considered a current asset, as it will be converted to cash or used within a fairly short time. At the end of the accounting year, the ending balances in the balance sheet accounts (assets and liabilities) will carry forward to the next accounting year.