How Variance Analysis Can Improve Financial Results

You must examine any cost variance figures you get in the context of your business to determine the true impact those numbers will have. A budget variance is the difference between the budgeted or baseline amount of expense or revenue, and the actual amount. The budget variance is favorable when the actual revenue is higher than the budget or when the actual expense is less than the budget. In rare cases, the budget variance can also refer to the difference between actual and budgeted assets and liabilities. The variance is not simply the average difference from the expected value.

In program and project management, for example, financial data are generally assessed at key intervals or milestones. For instance, a monthly closing report might provide quantitative data about expenses, revenue and remaining inventory levels. Variances between planned and actual costs might lead to adjusting business goals, objectives or strategies. Budget variance is a periodic measure used by governments, corporations or individuals to quantify the difference between budgeted and actual figures for a particular accounting category. A favorable budget variance refers to positive variances or gains; an unfavorable budget variance describes negative variance, meaning losses and shortfalls.

How do you calculate budget variance?

A budget variance is the difference between the budgeted or baseline amount of expense or revenue, and the actual amount. The budget variance is favorable when the actual revenue is higher than the budget or when the actual expense is less than the budget.

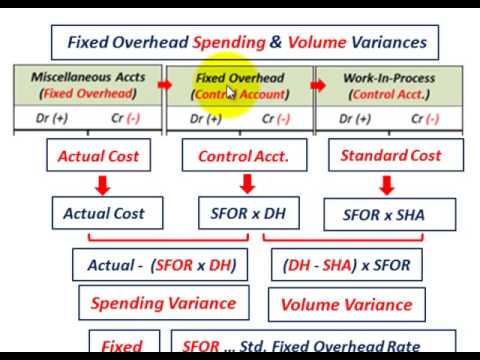

RemarksIf the cost variance is negative, the cost for the task is currently under the budgeted, or baseline, amount. If the cost variance is positive, the cost for the task is currently over budget. When the task is complete, this field shows the difference between baseline costs and actual costs. A favorable variance is one where revenue comes in higher than budgeted or expenses are lower than predicted.

RemarksIf the cost variance is negative, the cost for the assignment is currently under the budgeted, or baseline, amount. If the cost variance is positive, the cost for the assignment is currently over budget. When the assignment is complete, this field shows the difference between baseline costs and actual costs.

As an example of a budget variance, ABC Company had budgeted $400,000 of selling and administrative expenses, and actual expenses are $420,000. Because costs are higher than you planned, the variance is unfavorable. A favorable variance exists when actual costs are lower than planned.

Variance analysis A02, AO4

On the other hand, positive variances in terms of a company’s profits are presented without parentheses. Negative figures happen if you spend more on a project than you allowed in your budget.

Your budget uses the same budgeted labor hours that you calculated earlier. Because the actual hourly rate we paid was less than planned ($23 – $25), we have a favorable price variance. Because the variance relates to a cost, a negative number indicates a cost savings. Many owners create a company budget, but don’t use it to make changes in the business. To make use of your budget, compare your actual results to your budget.

In project management, variance analysis helps maintain control over a project’s expenses by monitoring planned versus actual costs. Effective variance analysis can help a company spot trends, issues, opportunities and threats to short-term or long-term success. When revenues are lower than expected, or expenses are higher than expected, the variance is unfavorable.

For example, if a company budgets $10,000 for an expense and spends $8,000, subtract $8,000 from $10,000. The difference is a surplus of $2,000, or a positive expense variance.

How and why a company should use a static budget, static budget variances, and flexible budgets.

The University of Colorado, for example, prepares its revenue and expense reports monthly. It asks managers to compare actual expenses to the budget at least quarterly and make spending adjustments as necessary.

- During the budgeting process, a company does its best to estimate the sales revenues and expenses it will incur during the upcoming accounting period.

- After the period is over, management will compare budgeted figures with actual ones and determine variances.

Conversely, an unfavorable variance occurs when revenue falls short of the budgeted amount or expenses are higher than predicted. Hence, net income may be below what management originally expected. Depending on their accounting systems, companies break down expenses in various ways.

One level may show a positive expense variance that disappears at another level. For example, a company has a $10,000 advertising budget and plans $5,000 to advertise boots and $5,000 to advertise athletic shoes. However, it actually spends $3,000 advertising boots and $7,000 advertising athletic shoes.

It has a $2,000 positive expense variance for boots and a $2,000 negative expense variance for shoes. These two variances cancel each other out at a higher level, and shoe advertising overall is on budget. A negative variance occurs where ‘actual’ is less than ‘planned’ or ‘budgeted’ value. Examples would be when the raw materials cost less than expected, sales were less than predicted, and labour costs were below the budgeted figure. In your budgeting process, you estimate a standard variable overhead rate of $10 per labor hour.

Causes of variances

For example, when actual expenses are lower than projected expenses, the variance is favorable. Likewise, if actual revenues are higher than expected, the variance is favorable. An expense or expenditure variance is the difference between a budgeted expense and the actual amount. The variance is positive or negative, depending on whether an expense is less or more than budgeted.

For example, if the expected price of raw materials was $7 a pound but the company was forced to pay $9 a pound, the $200 variance would be unfavorable instead of favorable. Data on positive and negative expense variance helps management measure and improve performance.

Any differences you find between budgeted and actual results are called variances. Creating a detailed budget is critically important for the success of your business. A well-managed company will budget for sales, production costs and all other expenses. The negative variances, which are unfavorable in terms of a company’s profits, are usually presented in parentheses.

If a company budgets $8,000 and spends $10,000, subtract $10,000 from $8,000. The result is -$2,000, a negative expense variance or cost overrun. Cost variance allows you to monitor the financial progression of whatever it is you are doing in your business.

When cost variances are low, you know you have controlled your risks well. You also know you have retrieved and analyzed data related to operations sufficiently. Ideally, your actual costs should match what you budgeted and your cost variance should be zero, but in practice this is fairly difficult to achieve.

Budget variances occur because forecasters are unable to predict the future costs and revenue with complete accuracy. Regardless of whether the variance is positive or negative, it means one of two things. The first is that, due to insufficient or inappropriate data or human error, you overestimated or underestimated expenses. A favorable variance occurs when net income is higher than originally expected or budgeted.

During the budgeting process, a company does its best to estimate the sales revenues and expenses it will incur during the upcoming accounting period. After the period is over, management will compare budgeted figures with actual ones and determine variances. If revenues were higher than expected, or expenses were lower, the variance is favorable. If revenues were lower than budgeted or expenses were higher, the variance is unfavorable. Variance analysis is important to assist with managing budgets by controlling budgeted versus actual costs.

Positive figures result if you spend less on a project than the budget predicted. Negative cost variance figures are almost always a bad thing for a business, as companies cannot always guarantee they can come up with the funds to cover the excess cost. However, positive cost variances aren’t always good for a company, either. For instance, if you come out in the black on your project budget by sacrificing customer service or quality parts, you may not sell as many of the products or may lose clients.

Negative variance

Variance analysis, also described as analysis of variance or ANOVA, involves assessing the difference between two figures. It is a tool applied to financial and operational data that aims to identify and determine the cause of the variance. In applied statistics, there are different forms of variance analysis.

Managers also compare current and previous year’s budgets to check whether planned expansions or contractions are taking place. In addition, managers can examine whether a specific positive expense variance came by accident or design. They can determine whether or not the organization got the desired result even with the cost savings.