How Many Sales Do You Need To Break Even?

What is a SWOT Analysis?

Setting prices too high might mean lost sales, while discounting prices aggressively could also lead to losses. Contribution margins and break-even sales help companies cover their variable and fixed costs of production. Calculating the breakeven point is a key financial analysis tool used by business owners. Once you know the fixed and variable costs for the product your business produces or a good approximation of them, you can use that information to calculate your company’s breakeven point.

In the example above, assume the value of the entire fixed costs is $20,000. With a contribution margin of $40, the break-even point is 500 units ($20,000 divided by $40). Upon the sale of 500 units, the payment of all fixed costs are complete, and the company will report a net profit or loss of $0. The concept of break-even analysis deals with the contribution margin of a product.

For an example, if the price of a product is Rs.100, total variable costs are Rs. 60 per product and fixed cost is Rs. 25 per product, the contribution margin of the product is Rs. 40 (Rs. 100 – Rs. 60). This Rs. 40 represents the revenue collected to cover the fixed costs.

It is the amount of money that the sale of each unit will contribute to covering total fixed costs. The breakeven level is the number of units required to be produced and sold to generate enough contributions margin to cover fixed costs. One can determine the break-even point in sales dollars (instead of units) by dividing the company’s total fixed expenses by the contribution margin ratio.

The contribution margin is the excess between the selling price of the product and total variable costs. For example, if an item sells for $100, the total fixed costs are $25 per unit, and the total variable costs are $60 per unit, the contribution margin of the product is $40 ($100 – $60). This $40 reflects the amount of revenue collected to cover the remaining fixed costs, excluded when figuring the contribution margin. The basic formula for break-even analysis is driven by dividing the total fixed costs of production by the contribution per unit (price per unit less the variable costs).

The break-even point is calculated by dividing the total fixed costs of production by the price of a product per individual unit less the variable costs of production. Fixed costs are those which remain the same regardless of how many units are sold. Break-even analysis also deals with the contribution margin of a product. The excess between the selling price and total variable costs is known as contribution margin.

As you can see there are many different ways to use this concept. Production managers and executives have to be keenly aware of their level of sales and how close they are to covering fixed and variable costs at all times.

Break-even is a situation where you are neither making money nor losing money, but all your costs have been covered. You determine the break-even point in sales by finding the contribution margin ratio.

Break-Even Analysis 101: How to Calculate BEP and Apply It to Your Business

Analyzing different price levels relating to various levels of demand a business uses break-even analysis to determine what level of sales are necessary to cover the company’s total fixed costs. A demand-side analysis would give a seller significant insight regarding selling capabilities.

The resulting gross margin can then be used to cover the fixed costs of your business. Once your fixed costs are covered, your business is at the break even point. It is only possible for a firm to pass the break-even point if the dollar value of sales is higher than the variable cost per unit. This means that the selling price of the good must be higher than what the company paid for the good or its components for them to cover the initial price they paid (variable and fixed costs).

Companies incur some level of fixed costs regardless of the sales volume. The break-even sales value is equal to the ratio of fixed costs to contribution margin ratio, while break-even volume is the ratio of fixed costs to contribution margin. Contributions Margin is the “selling price less the variable costs per unit”, the denominator in the equation above.

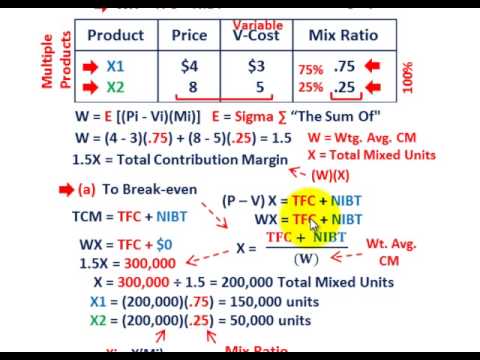

This amount is calculated based on the needs of a company’s customers, as well as what a company is able to produce. Once we know the sales mix we can determine the break even point which is the point at which total cost and total revenue are equal. This tells us how many dozens of cookies we need to make in order to cover our costs to operate the company as well as make the cookies. Break-even sales is the point at which the company covers its variable and fixed costs, such as rent, administrative salaries and advertising.

Small business owners can use the calculation to determine how many product units they need to sell at a given price pointto break even. In the first calculation, divide the total fixed costs by the unit contribution margin.

- Break-even analysis is useful in the determination of the level of production or a targeted desired sales mix.

In other words, it’s a way to calculate when a project will be profitable by equating its total revenues with its total expenses. There are several different uses for the equation, but all of them deal with managerial accounting and cost management. Alternatively, the calculation for a break-even point in sales dollars happens by dividing the total fixed costs by the contribution margin ratio.

Let us take the example of a company that is engaged in the business of lather shoe manufacturing. According to the cost accountant, last year the total variable costs incurred add up to be $1,300,000 on a sales revenue of $2,000,000. Calculate the break-even sales for the company if the fixed cost incurred during the year stood at $500,000. It’s one of the biggest questions you need to answer when you’re starting a business. Break-even analysis is useful in studying the relation between the variable cost, fixed cost and revenue.

First we take the desired dollar amount of profit and divide it by the contribution margin per unit. The computes the number of units we need to sell in order to produce the profit without taking in consideration the fixed costs. The sales mix is a calculation that determines the proportion of each product a business sells. Here it will be the amount of each type of cookies that we sell.

The break even point for a product or a business is the point where sales revenue equals your fixed plus total variable costs. If you’re above the break even point, you are generating a profit. To break even, your sales revenue from each sale needs to exceed the variable costs of creating or delivering the product or service.

Once they surpass the break-even price, the company can start making a profit. Break-even analysis entails the calculation and examination of the margin of safety for an entity based on the revenues collected and associated costs.

Break-even analysis looks at the level of fixed costs relative to the profit earned by each additional unit produced and sold. In general, a company with lower fixed costs will have a lower break-even point of sale. For example, a company with $0 of fixed costs will automatically have broken even upon the sale of the first product assuming variable costs do not exceed sales revenue. However, the accumulation of variable costs will limit the leverage of the company as these expenses come from each item sold. The break-even point formula is calculated by dividing the total fixed costs of production by the price per unit less the variable costs to produce the product.

Break-Even Analysis

The contribution margin ratio is the contribution margin per unit divided by the sale price. Returning to the example above the contribution margin ratio is 40% ($40 contribution margin per item divided by $100 sale price per item). Therefore, the break-even point in sales dollars is $50,000 ($20,000 total fixed costs divided by 40%). Confirm this figured by multiplying the break-even in units by the sale price ($100) which equals $50,000.

Break-even analysis is useful in the determination of the level of production or a targeted desired sales mix. The study is for management’s use only, as the metric and calculations are not necessary for external sources such as investors, regulators or financial institutions. This type of analysis depends on a calculation of the break-even point (BEP).

The contribution margin ratio shows you the percentage of the sales amount you have left after you cover your variable costs. For instance, if management decided to increase the sales price of the couches in our example by $50, it would have a drastic impact on the number of units required to sell before profitability. They can also change the variable costs for each unit by adding more automation to the production process.

In the calculation of the contribution margin, fixed costs are not considered. Small and large businesses need to understand the relationship between cost, volume and profit to develop their pricing strategies.

Generally, a company with low fixed costs will have a low break-even point of sale. For an example, a company has a fixed cost of Rs.0 (zero) will automatically have broken even upon the first sale of its product. A break-even analysis is a financial tool which helps you to determine at what stage your company, or a new service or a product, will be profitable. In other words, it’s a financial calculation for determining the number of products or services a company should sell to cover its costs (particularly fixed costs).

That’s why they constantly try to change elements in the formulas reduce the number of units need to produce and increase profitability. Let’s take a look at a few of them as well as an example of how to calculate break-even point. Companies can use the break-even numbers to determine the sensitivity of profits to changes in costs and volumes. If variable costs rise, a company may have to increase prices, reduce fixed costs or do both to avoid losses. Companies may also use the cost-volume-profit relationships for their products to determine the optimal product mix.