General ledger accounts: How a General Ledger Works With Double-Entry Accounting Along With Examples

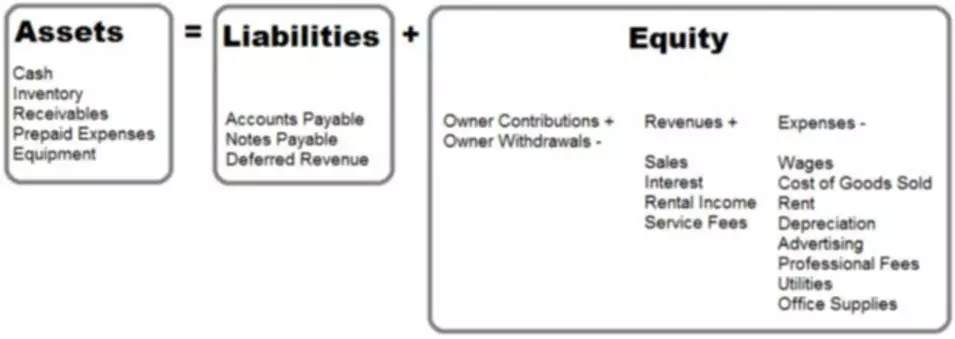

If your business doesn’t make enough purchases to warrant keeping them in its own ledger, you can include them in your general ledger. Revenue accounts in the general ledger are typically divided into categories, such as sales and interest. For example, sales may be further divided into retail sales and wholesale sales, or foreign sales and domestic sales. Accounts payable is the money a company owes to its suppliers and vendors for products and services purchased on credit.

- At times this can involve reviewing dozens of journal entries, but it is imperative to maintain reliably error-free and credible company financial statements.

- “As transactions in your business occur, they are noted in the general ledger under each account using double-entry accounting.

- Also known as an accounting ledger, the general ledger serves as the record for a business’s financial data.

- This ledger is used to record each transaction and uses a trial balance to validate the information.

- If it doesn’t, then ‘the books’ are imbalanced and the accountant responsible will have to provide an explanation.

Your general ledger might break these down into accounts for rent, merchant fees, software subscriptions, telephone and internet, cleaning, and so on. Accounts receivable (AR) refers to money that is owed to a company by its customers. The accounts receivable process begins when a customer purchases goods or services from a company and is issued an invoice. The customer usually has a set amount of time to pay the invoice, such as 30 days. For this transaction, the credit column will remain unchanged for this account.

Process

This ledger is used to record each transaction and uses a trial balance to validate the information. These accounts only contain summary balances that have been posted from subsidiary ledgers. This is done in order to minimize the transaction volume cluttering the general ledger. The accounts receivable and accounts payable accounts are the most likely to be control accounts. At the end of each fiscal period, a trial balance is calculated by listing all of the debit and credit accounts and their totals.

Examples of other general ledger accounts that are commonly used are noted below. Owner’s equity is the portion of the business’s assets that you or your shareholders own. When your business records revenue from sales, this will increase owner’s equity because it means that the company has earned more money.

A company may opt to store its general ledger using blockchain technology, which can prevent fraudulent accounting transactions and preserve the ledger’s data integrity. It assists in more accurate financial reporting on revenue and expenditure, and it creates clarity around what items take up the biggest share of capital. General ledger reconciliation is the process of ensuring that the general ledger is in balance. By reconciling all transactions, you ensure that all entries are correctly entered and that your books balance. Quite simply, every entry into a debit account will impact the credit account, and this must therefore be recorded, too. In this accounting method, an entry on the debit side must be accompanied by a corresponding entry on the credit side.

The difference between journals and accounting ledgers

General Ledger Accounts (GLs) are account numbers used to categorize types of financial transactions. A “chart of accounts” is a complete listing of every account in an accounting system. A ‘balanced book’ also provides the foundation for checking every other financial statement. If the general ledger doesn’t balance, it opens up the investigation into specific financial areas of an organization, and this can lead to smarter processes and innovation in record keeping. For example, when an accountant enters a credit entry into the credit account, this increases an owner’s equity and positively impacts the liabilities account. As a consequence, the debit account will decrease because there is now more cash in the bank.

- Depending on the size of your business and what your business does, you may not need to use all of them.

- Of course, with the right accounting software, you can configure it to auto-generate tax reports for you, which not only saves you time, but also reduces human error and increases compliance.

- At any time in an organization’s lifespan, this equation should balance.

- The expense side of the income statement might be based on GL accounts for interest expenses and advertising expenses.

- Even with automated accounting software, accountants have to track all financial records so there’s visibility over money coming in, and money going out.

Let’s look at some of the accounts small businesses may use in the general ledger. Here is an example of an accounting system transaction within a general ledger for a fictional account, ABCDEFGH Software. Instead, they show actual amounts spent or received and not merely projected in a budget.

Format of a ledger

In accounting, a general ledger is used to record a company’s ongoing transactions. Within a general ledger, transactional data is organized into assets, liabilities, revenues, expenses, and owner’s equity. After each sub-ledger has been closed out, the accountant prepares the trial balance. This data from the trial balance is then used to create the company’s financial statements, such as its balance sheet, income statement, statement of cash flows, and other financial reports.

A general ledger represents the record-keeping system for a company’s financial data, with debit and credit account records validated by a trial balance. Transaction data is segregated, by type, into accounts for assets, liabilities, owners’ equity, revenues, and expenses. The totals calculated in the general ledger are then entered into other key financial reports, notably the balance sheet — sometimes called the statement of financial position. The balance sheet records assets and liabilities, as well as the income statement, which shows revenues and expenses. In the case of certain types of accounting errors, it becomes necessary to go back to the general ledger and dig into the detail of each recorded transaction to locate the issue. At times this can involve reviewing dozens of journal entries, but it is imperative to maintain reliably error-free and credible company financial statements.

General ledgers and double-entry bookkeeping

Organizations may instead employ one or more spreadsheets for their ledgers, including the general ledger, or may utilize specialized software to automate ledger entry and handling. For many smaller businesses, a general ledger costs more in time than it does in financial success, and many small business owners opt out of such scrutinized record keeping. However, real-time speed is only possible with the right accounting software. With an automated approach to the general ledger, accountants can receive instant alerts as soon as a wrong entry is made.

general ledger (GL)

Prior to digitization, accountants would literally ‘keep the books’ by handwriting entries into big ledgers, and it was how organizations of all sizes kept track of each and every transaction. By recording each transaction correctly, your trial balance should show equal credits and debits. In accounting, the terms debit and credit differ from their commonplace meanings.

Other types of GL accounts

Companies use a general ledger reconciliation process to find and correct such errors in the accounting records. In some areas of accounting and finance, blockchain technology is used in the reconciliation process to make it faster and cheaper. Broadly, the general ledger contains accounts that correspond to the income statement and balance sheet for which they are destined. The income statement will also account for other expenses, such as selling, general and administrative expenses, depreciation, interest, and income taxes. The difference between these inflows and outflows is the company’s net income for the reporting period.

It assists in tax reporting

The net result is that both the increase and the decrease only affect one side of the accounting equation. A cash book functions as both a journal and a ledger because it contains both credits and debits. Because a cash book is updated and referenced frequently, similar to a journal, mistakes can be found and corrected day-to-day instead of at the end of the month. One important difference between a journal and a ledger is that the ledger is where double-entry bookkeeping takes place. This is why there are two sides to a ledger, one for debits and one for credits.