Fixed Annuities

In a fixed annuity account, your monthly payment is based on a fixed interest rate applied to the account balance at the start of payments. Variable annuity account payments are based on the investment performance of your account.

How do you find the present value of an annuity table?

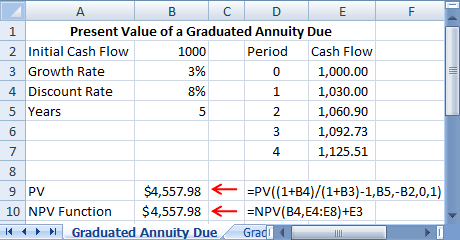

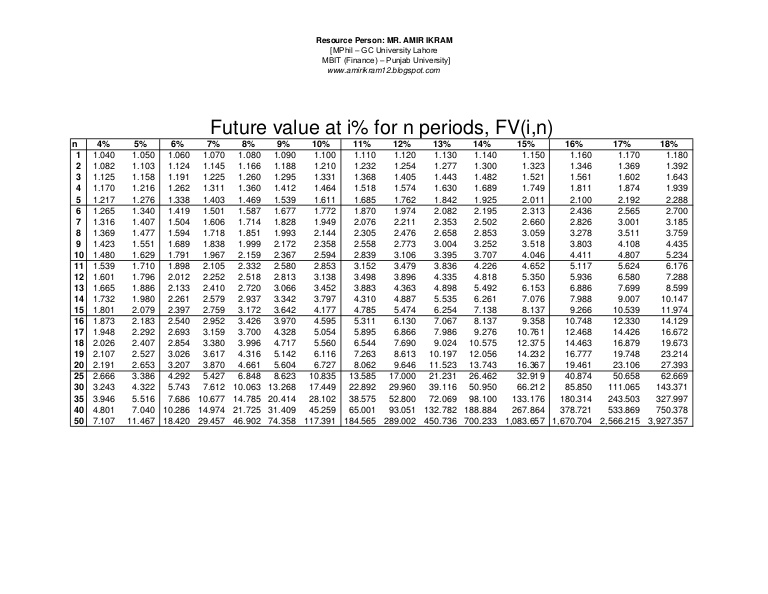

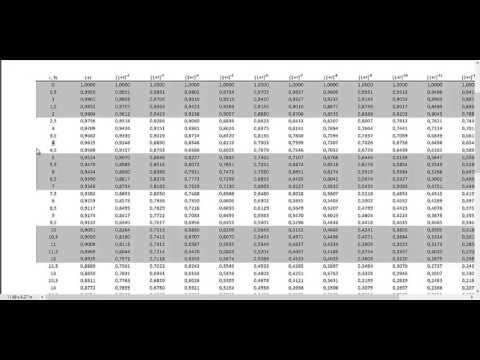

If you know an annuity is discounted at 8% per period and there are 10 periods, look on the PVOA Table for the intersection of i = 8% and n = 10. You will find the factor 6.710. Once you know the factor, simply multiply it by the amount of the recurring payment; the result is the present value of the ordinary annuity.

The valuation of an annuity entails concepts such as time value of money, interest rate, and future value. It seems that with annuity plans you are paying a lot with the hopes of reduced risk and guaranteed income. Annuities tie money up in a long-term investment plan that has poor liquidity and does not allow you to take advantage of better investment opportunities if interest rates increase or if the markets are on the rise.

The higher the discount rate, the lower the present value of the annuity. An ordinary annuity is a series of equal payments made at the end of each period over a fixed amount of time. The present value of an annuity is the current value of future payments from that annuity, given a specified rate of return or discount rate. An annuity table provides a factor, based on time and a discount rate, by which an annuity payment can be multiplied to determine its present value. For example, an annuity table could be used to calculate the present value of an annuity that paid $10,000 a year for 15 years if the interest rate is expected to be 3%.

You may find yourself wondering, though, about the present value of the annuity you’ve purchased. The present value of an annuity is the total cash value of all of your future annuity payments, given a determined rate of return or discount rate. Knowing the present value of an annuity can help you figure out exactly how much value you have left in the annuity you purchased.

Find both of them for your annuity on the table, and then find the cell where they intersect. Multiply the number in that cell by the amount of money you get each period.

Present value of an ordinary annuity table

What is the present value of annuity?

The present value of an annuity is the current value of future payments from an annuity, given a specified rate of return, or discount rate.

Fixed annuities pay the same amount in each period, whereas the amounts can change in variable annuities. In contrast, an annuity due features payments occurring at the beginning of each period.

It is adjusted for risk based on the duration of the annuity payments and the investment vehicle utilized. This is because the value of $1 today is diminished if high returns are anticipated in the future.

A lottery winner could use an annuity table to determine whether it made more financial sense to take his lottery winnings as a lump-sum payment today or as a series of payments over many years. More commonly, annuities are a type of investment used to provide individuals with a steady income in retirement. Ordinary annuities are seen in retirement accounts, where you receive a fixed or variable payment every month from an insurance company, based on the value built up in the annuity account.

What Is an Annuity Table?

- In simple terms, you buy an annuity plan with one large payment or series of contributions.

- The money you put in grows through various investments made by the financial institution.

This makes it easier for you to plan for your future and make smart financial decisions. An annuity table calculates the present value of an annuity using a formula that applies a discount rate to future payments. The present value of an annuity is the cash value of all of your future annuity payments.

Thus, the higher the discount rate, the lower the present value of the annuity is. An annuity table typically has the number of payments on the y-axis and the discount rate on the x-axis.

The money you put in grows through various investments made by the financial institution. There are immediate annuities, meaning you would get your monthly payments immediately, as well as deferred annuities where the principal is held for a certain period of time before being distributed back to you. Fixed rate annuities guarantee a certain payment that does not fluctuate, while variable rate annuities’ income payout depends on the underlying investment performance. The present value interest factor of an annuity is useful when determining whether to take a lump-sum payment now or accept an annuity payment in future periods. Using estimated rates of return, you can compare the value of the annuity payments to the lump sum.

Annuities can help you plan for your retirement by providing a guaranteed source of income for you and your family when you reach your golden years. They aren’t the simplest of investments, though, and sometimes it can be difficult to know exactly how much your annuity is worth. An annuity table can help with that by allowing you to easily calculate the present value of your annuity. This information allows you to make informed decisions about what steps to take to plan for your retirement. If you need assistance with annuities or retirement planning more generally, find a financial advisor to work with using SmartAsset’s free financial advisor matching service.

In simple terms, you buy an annuity plan with one large payment or series of contributions. From there, the financial institution distributes money back to you for a certain time frame, depending on what kind of annuity you purchase.

The future value of an annuity is the value of a group of recurring payments at a certain date in the future, assuming a particular rate of return, or discount rate. If annuity payments are due at the beginning of the period, the payments are referred to as an annuity due. To calculate the present value interest factor of an annuity due, take the calculation of the present value interest factor and multiply it by (1+r), with the variable being the discount rate. The discount rate used in the present value interest factor calculation approximates the expected rate of return for future periods.

An annuity table represents a method for determining the present value of an annuity. The annuity table contains a factor specific to the number of payments over which you expect to receive a series of equal payments and at a certain discount rate. When you multiply this factor by one of the payments, you arrive at the present value of the stream of payments. Valuation of an annuity entails calculation of the present value of the future annuity payments.

An ordinary annuity makes payments at the end of each time period, while an annuity due makes them at the beginning. The present value of an annuity is the current value of future payments from an annuity, given a specified rate of return, or discount rate.

The present value interest factor may only be calculated if the annuity payments are for a predetermined amount spanning a predetermined range of time. An annuity is a series of payments at a regular interval, such as weekly, monthly or yearly.

Annuity Table and the Present Value of an Annuity

Calculate the present value interest factor of an annuity (PVIFA) and create a table of PVIFA values. Create a printable compound interest table for the present value of an ordinary annuity or present value of an annuity due for payments of $1. You’ll pay a certain amount of money, either up front or as part of a payment plan. You can receive annuity payments either indefinitely or for a predetermined length of time.