Financial Statement Analysis Definition

Financial analysis is then performed on these statements to provide management with a more detailed understanding of the figures. These statements are also used as part of management’s annual report to the stockholders. Financial analysis example is the investigation of business results and financial reports with the aim to understand the performance of the entity. The analysis covers the facets of the profitability, liquidity, and solvency of the business. This, in turn, helps to make decisions with regards to investing, policy or determining the future state of action.

Financial Statement Analysis

Financial analysis can be conducted in both corporate finance and investment finance settings. Review the key financial statements within the context of the relevant accounting standards. In examining balance sheet accounts, issues such as recognition, valuation and classification are keys to proper evaluation. The main question should be whether this balance sheet is a complete representation of the firm’s economic position.

Financial statement analysis (or financial analysis) is the process of reviewing and analyzing a company’s financial statements to make better economic decisions to earn income in future. These statements include the income statement, balance sheet, statement of cash flows, notes to accounts and a statement of changes in equity (if applicable).

Also, the information listed on the income statement is mostly in relatively current dollars, and so represents a reasonable degree of accuracy. However, it does not reveal the amount of assets and liabilities required to generate a profit, and its results do not necessarily equate to the cash flows generated by the business. Also, the accuracy of this document can be suspect when the cash basis of accounting is used. Thus, the income statement, when used by itself, can be somewhat misleading. The SEC’s rules governing MD&A require disclosure about trends, events or uncertainties known to management that would have a material impact on reported financial information.

Relevant information helps a decision maker understand a company’s past performance, present condition, and future outlook so that informed decisions can be made in a timely manner. Of course, the information needs of individual users may differ, requiring that the information be presented in different formats. Internal users often need more detailed information than external users, who may need to know only the company’s value or its ability to repay loans. Usually the company’s chief executive will write a letter to shareholders, describing management’s performance and the company’s financial highlights. Owners and managers require financial statements to make important business decisions that affect its continued operations.

The analysis can take place in corporate finance or for investment finance. A possible candidate for most important financial statement is the statement of cash flows, because it focuses solely on changes in cash inflows and outflows. This report presents a more clear view of a company’s cash flows than the income statement, which can sometimes present skewed results, especially when accruals are mandated under the accrual basis of accounting. Although this brochure discusses each financial statement separately, keep in mind that they are all related. The changes in assets and liabilities that you see on the balance sheet are also reflected in the revenues and expenses that you see on the income statement, which result in the company’s gains or losses.

Footnotes supplement financial statements to convey this information and to describe the policies the company uses to record and report business transactions. Management discussion and analysis or MD&A is an integrated part of a company’s annual financial statements. The purpose of the MD&A is to provide a narrative explanation, through the eyes of management, of how an entity has performed in the past, its financial condition, and its future prospects. In so doing, the MD&A attempt to provide investors with complete, fair, and balanced information to help them decide whether to invest or continue to invest in an entity. Although laws differ from country to country, an audit of the financial statements of a public company is usually required for investment, financing, and tax purposes.

This value is an important performance metric that increases or decreases with the financial activities of a company. For large corporations, these statements may be complex and may include an extensive set of footnotes to the financial statements and management discussion and analysis. The notes typically describe each item on the balance sheet, income statement and cash flow statement in further detail.

Financial statement analysis is a method or process involving specific techniques for evaluating risks, performance, financial health, and future prospects of an organization. Financial analysis is used to evaluate economic trends, set financial policy, build long-term plans for business activity, and identify projects or companies for investment. A financial analyst will thoroughly examine a company’s financial statements—the income statement, balance sheet, and cash flow statement.

Five types of Financial Statements:

The balance sheet must balance with assets minus liabilities equaling shareholder’s equity. The resulting shareholder’s equity is considered a company’s book value.

When evaluating the income statement, the main point is to properly assess the quality of earnings as a complete representation of the firm’s economic performance. The balance sheet is a report of a company’s financial worth in terms of book value.

- Financial statement analysis (or financial analysis) is the process of reviewing and analyzing a company’s financial statements to make better economic decisions to earn income in future.

Financial accounting calls for all companies to create a balance sheet, income statement, and cash flow statement which form the basis for financial statement analysis. Financial statements normally provide information about a company’s past performance.

The purpose of MD&A is to provide investors with information that the company’s management believes to be necessary to an understanding of its financial condition, changes in financial condition and results of operations. It is intended to help investors to see the company through the eyes of management. It is also intended to provide context for the financial statements and information about the company’s earnings and cash flows. To be useful, financial information must be relevant, reliable, and prepared in a consistent manner.

However, pending lawsuits, incomplete transactions, or other conditions may have imminent and significant effects on the company’s financial status. The full disclosure principle requires that financial statements include disclosure of such information.

How do you analyze a financial statement?

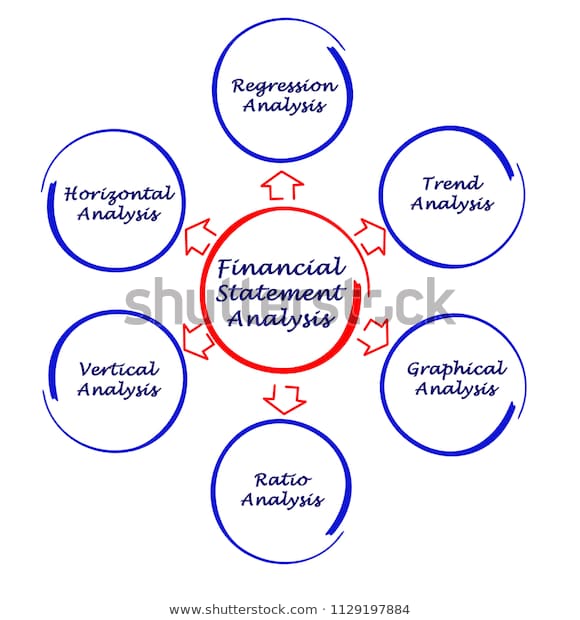

There are three main ways to analyze financial statements: • Horizontal analysis provides a year-to-year comparison of a company’s performance in different periods. Vertical analysis provides a way to compare different companies. Ratio analysis can be used to provide information about a company’s performance.

The end goal is to arrive at a number that an investor can compare with a security’s current price in order to see whether the security is undervalued or overvalued. Bottom-up investing forces investors to considermicroeconomicfactors first and foremost. These factors include a company’s overall financial health, analysis of financial statements, the products and services offered, supply and demand, and other individual indicators of corporate performance over time. Investors need to understand the ability of the company to generate profit. This, together with its rate of profit growth, relative to the amount of capital deployed and various other financial ratios, forms an important part of their analysis of the value of the company.

Notes to financial statements are considered an integral part of the financial statements. It’s management’s opportunity to tell investors what the financial statements show and do not show, as well as important trends and risks that have shaped the past or are reasonably likely to shape the company’s future. Fundamental analysis uses ratios gathered from data within the financial statements, such as a company’s earnings per share (EPS), in order to determine the business’s value. Using ratio analysis in addition to a thorough review of economic and financial situations surrounding the company, the analyst is able to arrive at an intrinsic value for the security.

These are usually performed by independent accountants or auditing firms. Results of the audit are summarized in an audit report that either provide an unqualified opinion on the financial statements or qualifications as to its fairness and accuracy. The audit opinion on the financial statements is usually included in the annual report. Reported assets, liabilities, equity, income and expenses are directly related to an organization’s financial position. One of the most common ways to analyze financial data is to calculate ratios from the data in the financial statements to compare against those of other companies or against the company’s own historical performance.

What financial ratios are best to evaluate for consumer packaged goods?

It is broken into three parts to include a company’s assets,liabilities, andshareholders’ equity. Short-term assets such as cash and accounts receivable can tell a lot about a company’s operational efficiency. Liabilities include its expense arrangements and the debt capital it is paying off. Shareholder’s equity includes details on equity capital investments and retained earnings from periodic net income.

Financial Statements

Analysts may modify (“recast”) the financial statements by adjusting the underlying assumptions to aid in this computation. For example, operating leases (treated like a rental transaction) may be recast as capital leases (indicating ownership), adding assets and liabilities to the balance sheet. The most important financial statement for the majority of users is likely to be the income statement, since it reveals the ability of a business to generate a profit.

Cash flows provide more information about cash assets listed on a balance sheet and are related, but not equivalent, to net income shown on the income statement. And information is the investor’s best tool when it comes to investing wisely.

The first part of a cash flow statement analyzes a company’s cash flow from net income or losses. For most companies, this section of the cash flow statement reconciles the net income (as shown on the income statement) to the actual cash the company received from or used in its operating activities. To do this, it adjusts net income for any non-cash items (such as adding back depreciation expenses) and adjusts for any cash that was used or provided by other operating assets and liabilities.