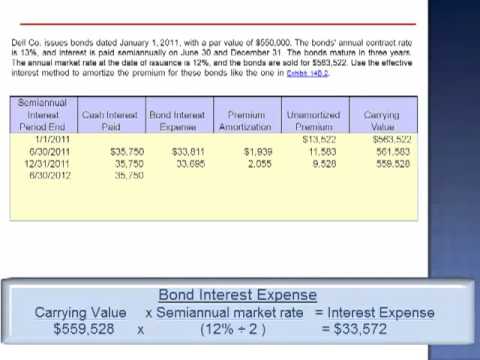

Effective Interest Rates

The effective interest rate is also known as the annual percentage yield, or APY. Among Excel’s more popular formulas, the EFFECT formula is often used by financial professionals to figure out an effective interest rate from a nominal interest rate.

Read on to learn how to use Excel’s EFFECT formula to calculate an effective interest rate (APY) from a nominal interest rate (APR). The nominal interest rate, also called annual percentage rate (APR), is simply the monthly interest rate (say 1% per month) multiplied by twelve (the number of periods in a year). There are several online calculators that you can use to calculate the effective interest rate quickly. In addition, the EFFECT() function in Microsoft Excel will calculate the effective rate given the nominal rate and number of compounding periods. For example, for a deposit at a stated rate of 10% compounded monthly, the effective annual interest rate would be 10.47%.

Effective interest rate is the per year rate that gives you exactly the same interest equal to using nominal rate that is compounded multiple times a year. where “ia” is the effective annual interest rate, “r” is the nominal annual interest rate, and “m” is the number of compounding periods per year. The effective annual interest rate is equal to 1 plus the nominal interest rate in percent divided by the number of compounding persiods per year n, to the power of n, minus 1. In accountancy the term effective interest rate is used to describe the rate used to calculate interest expense or income under the effective interest method. This is not the same as the effective annual rate, and is usually stated as an APR rate.

Going back to the example in the previous video, we deposited $800 in a bank account that gives us 6% of interest compounded monthly. To calculate the effective interest rate, we need to calculate the period interest rate first and then we use the equation that we just extracted. So effective interest rate would be 6.17%, which means if we apply 6.17% interest rate per year, it will give us exactly the same future value as applying interest rate of 6% compounded monthly.

Suppose you have an investment account with a “Stated Rate” of 7% compounded monthly then the Effective Annual Interest Rate will be about 7.23%. Further, you want to know what your return will be in 5 years. Using the calculator, your periods are years, nominal rate is 7%, compounding is monthly, 12 times per yearly period, and your number of periods is 5.

APR vs APY: Why Your Bank Hopes You Can’t Tell the Difference

As it turns out, a 12% APR (nominal) interest loan has an effective (APY) interest rate of about 12.68%. On a loan with a life of only one year, the difference between 12% and 12.68% is minimal. On a long-term loan such as a mortgage, the difference can be significant.

In previous slide, I explained how we calculate the F1 future value at the end of year one from period interest rate, i, and number of compounding periods per year, m. An effective interest rate is the interest rate that when applied once per year, it will give you the same amount of interest equal to a nominal rate of r. Annual percentage yield, or APY, is the term that is used in the banking industry for effective interest rate.

For example, a bank must enter the total annual charge for loans as a percentage price. Meanwhile, this particular loan becomes less favorable if you keep the money for a shorter period of time. For example, if you borrow $1,000 from a bank for 120 days and the interest rate remains at 6%, the effective annual interest rate is much higher. Going back to the example in the previous video, you saw that if you deposit $100 in a bank account, that gives you 6% interest rate compounded monthly, you will receive $106 plus $0.17 per year.

Interest Rates

The more often compounding occurs, the higher the effective interest rate. Investment B has a higher stated nominal interest rate, but the effective annual interest rate is lower than the effective rate for investment A. This is because Investment B compounds fewer times over the course of the year. Effective interest rate calculation determines the effective interest rate, which represents the actual costs of the capital or the actual revenue from a capital investment.

The effective interest rate is the interest rate on a loan or financial product restated from the nominal interest rate as an interest rate with annual compound interest payable in arrears. It is used to compare the annual interest between loans with different compounding terms (daily, monthly, quarterly, semi-annually, annually, or other).

All loans have compound interest, meaning the bank includes the previous month’s accrued interest when calculating your next month’s interest. The effective rate takes this into consideration and expresses it as a rate that is generally slightly higher than the stated interest rate but lower than the APR.

- The effective interest rate is the interest rate on a loan or financial product restated from the nominal interest rate as an interest rate with annual compound interest payable in arrears.

- It is also called effective annual interest rate, annual equivalent rate (AER) or simply effective rate.

What Is the Effective Interest Method of Amortization?

The annual interest rate quoted by the bank is often called the nominal rate (nominal means in name only). The effective annual interest rate gives effect to the compounding of the nominal rate. When analyzing a loan or an investment, it can be difficult to get a clear picture of the loan’s true cost or the investment’s true yield. There are several different terms used to describe the interest rate or yield on a loan, including annual percentage yield, annual percentage rate, effective rate, nominal rate, and more.

But you will almost never see the effective interest rate, despite its importance in financing. The system uses a comparison account to calculate the effective interest rate. This account contains all actual payments from the bank and customers.

A statement that the “interest rate is 10%” means that interest is 10% per year, compounded annually. In this case, the nominal annual interest rate is 10%, and the effective annual interest rate is also 10%. However, if compounding is more frequent than once per year, then the effective interest rate will be greater than 10%.

Banks will advertise the effective annual interest rate of 10.47% rather than the stated interest rate of 10%. The effective annual interest rate is the real return paid on savings or the real cost of a loan as it takes into account the effects of compounding and any fees charged. Looked at yet another way, the effective annual rate tells you by what percentage the principal will grow in a year taking compounding into account. The effective interest rate is the total interest cost associated with the loan.

Of these, the effective interest rate is perhaps the most useful, giving a relatively complete picture of the true cost of borrowing. To calculate the effective interest rate on a loan, you will need to understand the loan’s stated terms and perform a simple calculation.

Effective Annual Interest Rate

It is also called effective annual interest rate, annual equivalent rate (AER) or simply effective rate. Two interest rates used in business loans are the nominal interest rate and the effective interest rate.

Every time a payment is made, interest is computed and paid. The annual interest rate and the effective interest rate can be two very different numbers because of the effects of interest compounding. Knowing the effective interest rate is important for small business when determining which bank is offering the best loan or which investment is offering the highest rate of return.

For example, for a loan at a stated interest rate of 30%, compounded monthly, the effective annual interest rate would be 34.48%. Banks will typically advertise the stated interest rate of 30% rather than the effective interest rate of 34.48%. The effective annual interest rate is the real return on a savings account or any interest-paying investment when the effects of compounding over time are taken into account. It also reveals the real percentage rate owed in interest on a loan, a credit card, or any other debt. m is the number of compounding periods per year, and i is period interest rate.

The Effective Interest Rate Calculator is used to calculate the effective annual interest rate based on the nominal annual interest rate and the number of compounding periods per year. A bank certificate of deposit, a savings account, or a loan offer may be advertised with its nominal interest rate as well as its effective annual interest rate. The nominal interest rate does not take reflect the effects of compounding interest or even the fees that come with these financial products. Effective interest rates are relevant when there is more than one compounding period in a year. Many personal loans use a compounding period other than a year, normally a month.

Note that now you can change the values in both B1 and B2 and Excel will calculate the effective interest rate (APY) in cell B3. For example, change the nominal interest rate (APR) in B1 to 6% and the effective interest rate (APY) in B3 changes to 6.17%. Using the EFFECT function in Excel, you can figure out any effective interest rate given any nominal rate and the number of compounding periods in a year. However, since interest is compounded monthly, the actual or effective interest rate is higher because interest in the current month compounds against interest in the previous month.

Example of Effective Annual Interest Rate

You can see here, when you read somewhere, that for example interest rate is 6% compounded monthly, it is a bit confusing. Because it doesn’t tell you what would be the actual interest rate per year.