Cost in Excess of Billings Law and Legal Definition

Under U.S. generally accepted accounting principles, the PCM is the preferred method for contract accounting, and GAAP places a number of conditions and restrictions upon its use. GAAP also allows the completed contract method, in which a contractor don’t recognize expenses or revenues until the contract is finished.

The percentage of completion method of accounting requires the reporting of revenues and expenses on a period-by-period basis, as determined by the percentage of the contract that has been fulfilled. The current income and expenses are compared with the total estimated costs to determine the tax liability for the year.

How do you calculate percentage of completion?

The percentage of completion method of accounting requires the reporting of revenues and expenses on a period-by-period basis, as determined by the percentage of the contract that has been fulfilled. The current income and expenses are compared with the total estimated costs to determine the tax liability for the year.

The percentage of completion method is an accounting method in which the revenues and expenses of long-term contracts are recognized as a percentage of the work completed during the period. This is in contrast to the completed contract method, which defers the reporting of income and expenses until a project is completed. The percentage-of-completion method of accounting is common for the construction industry, but companies in other sectors also use the method. The Completed-contract method is an accounting method of work-in-progress evaluation, for recording long-term contracts.

Use the Percentage Completion (POC) method with construction based projects that extend over the course of several years. Furthermore, many accountants prefer the percentage completion accounting over the Completed Contract Method. Because the projects are usually long term lasting several years, it estimates completion for the company.

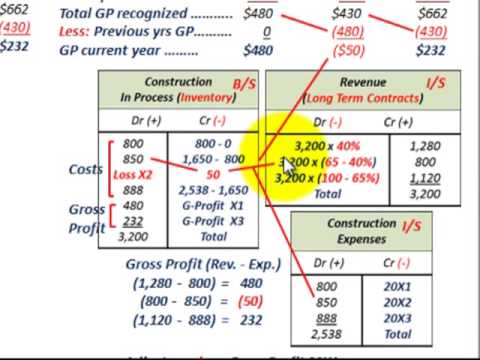

For example, a project that is 20% complete in year one and 35% complete in year two would only have the incremental 15% of revenue recognized in the second year. The recognition of income and expenses on this work-in-progress basis applies to the income statement, but the balance sheet is handled the same way as the completed contract method.

First, take an estimated percentage of how close the project is to being completed by taking the cost to date for the project over the total estimated cost. Then multiply the percentage calculated by the total project revenue to compute revenue for the period. Then derive the construction income by subtracting the cost from the period revenue. Under the cost recovery method no income is recognized on any sale till the time the cost of the product that has been sold is completely recovered in the form cash. This particular method is utilized at a time when collection of the selling price is highly uncertain and reaches an extent where it becomes difficult to justify the installment related method.

What is the Percentage of Completion Method?

In this method, the completion factor equals the project costs already incurred divided by the total estimated project costs. The contractor should disregard startup costs that don’t relate to contract performance. For example, the contractor doesn’t count the costs of buying and storing materials at the job site until the materials are actually used on the project. However, the contract can count toward completion the pre-installation costs of unique materials or assemblies to be used exclusively on a particular project.

Each of the installments should also be segregated between interest and principal. Once the entire costs of sales are recovered, any remaining cash receipt is recognized as gross profit. GAAP and the Internal Revenue Service don’t agree on all aspects of the percentage of completion method.

- The current income and expenses are compared with the total estimated costs to determine the tax liability for the year.

- For example, a project that is 20% complete in year one and 35% complete in year two would only have the incremental 15% of revenue recognized in the second year.

- The percentage of completion method of accounting requires the reporting of revenues and expenses on a period-by-period basis, as determined by the percentage of the contract that has been fulfilled.

Work in Progress vs. Work in Process: What’s the Difference?

The percentage of completion method falls in-line with IFRS 15, which indicates that revenue from performance obligations recognized over a period of time should be based on the percentage of completion. The method recognizes revenues and expenses in proportion to the completeness of the contracted project. Construction and engineering contracts normally use the percentage of completion method for revenue recognition.

This method is considered to be the very conservative when compared to other methods of recognizing revenue. As per the cost recovery method, both cost and revenue from selling an item is recognized at the selling point itself. However, the gross profit that comes with it is deferred till the time the entire sales cost has been fully recovered.

Under GAAP, you report the period’s profits based on earned revenues minus the costs of these revenues, using the appropriate input or output measure. The IRS allows contractors to deduct expenses as incurred, which might be in a different period than the one calculated via the GAAP methods. Therefore, the GAAP and IRS project profits might differ in a contract period, although they should coincide by the end of the project. GAAP allows revenue recognition based on the cost-to-cost method, but only in certain applications, including construction projects.

Potential for Abuse of the Percentage of Completion Method

The PCM determines when a contractor should bill a client as a contract progresses. The method applies to earned revenue and the costs of the earned revenue in each contract period. The method provides reasonably accurate income measurement and helps even out income and taxes over the entire contract period.

What is the percentage of completion method in GAAP?

The Percentage of completion formula is very simple. First, take an estimated percentage of how close the project is to being completed by taking the cost to date for the project over the total estimated cost. Then multiply the percentage calculated by the total project revenue to compute revenue for the period.

Construction-in-progress are generally not classified as inventory as it would not be in-line with IAS2.9 (Inventories to be stated at lower of cost or NRV). Percentage of completion (PoC) is an accounting method of work-in-progress evaluation, for recording long-term contracts. GAAP allows another method of revenue recognition for long-term construction contracts, the completed-contract method.

To employ the PCM, a contract must describe how to determine a “completion factor” that determines how much income the contractor has earned up to that point. The revenues earned and the costs of these revenues are equal to the completion factor times the total contract revenues and costs, respectively. GAAP doesn’t permit a contractor to determine revenue based on cash receipts.

GAAP allows another method of revenue recognition for long-term construction contracts, the percentage-of-completion method. The contract is considered complete when the costs remaining are insignificant. A primary advantage of the percentage-of-completion method over the completed-contract method is that it reports income evenly over the course of the contract. As a result, it presents a more accurate picture of a construction company’s financial position. Revenues and gross profit are recognized each period based on the construction progress, in other words, the percentage of completion.