Closing Entry Definition

Since a revenue account has a current credit balance, posting a debit closing entry of the same amount to the revenue account will bring the revenue account balance to zero. On the other hand, an expense account has a current debit balance, and posting a credit closing entry of the same amount to the expense account will reset the expense account balance to zero. With both revenue and expense accounts reset to zero balance, they are ready for recording any revenues and expenses for the next accounting period. Revenue and expense accounts in the income statement are considered temporary accounts.

Starting with zero balances in the temporary accounts each year makes it easier to track revenues, expenses, and withdrawals and to compare them from one year to the next. There are four closing entries, which transfer all temporary account balances to the owner’s capital account. An adjusting journal entry is an entry in a company’s general ledger that occurs at the end of an accounting period to record any unrecognized income or expenses for the period. When a transaction is started in one accounting period and ended in a later period, an adjusting journal entry is required to properly account for the transaction.

They are accrued revenues, accrued expenses, deferred revenues and deferred expenses. After the closing entries have been made, the temporary account balances will be reflected in the Retained Earnings (a capital account). However, an intermediate account called Income Summary usually is created. Revenues and expenses are transferred to the Income Summary account, the balance of which clearly shows the firm’s income for the period. A closing entry is a journal entry made at the end of accounting periodsthat involves shifting data from temporary accounts on the income statement to permanent accounts on the balance sheet.

Temporary accounts include revenue, expenses, and dividends and must be closed at the end of the accounting year. An accounting procedure followed by accountant at the end of every month to close the accounting records of current accounting month. Closing indicates that no entries will be posted in the closed period.

Accounts payable is also a permanent account that appears on the balance sheet, whereas expenses is a temporary account that shows up on an income statement. Debit the revenue account by the amount of its balance at the end of the accounting period to reduce it to zero.

It is processed according to a company’s predefined closing operation or is established at the time of process migration. It is important to perform“Month End Closing”in every organization as this enables accountant to generate accurate and consistent financial statements accountant. It also helps in early identification of any accounting issues, bank related issues rather than at year-end. A simple walk through of month end closing process is described below.

In the double-entry system of accounting, each financial transaction has at least one debit and one credit entry. Debits and credits are the key tools for adjusting company accounts. Closing entries are part of the accounting cycle, which starts with a financial transaction and ends with the preparation of financial statements. Account adjustments are entries made in the general journal at the end of an accounting period to bring account balances up-to-date. They are the result of internal events, which are events that occur within a business that don’t involve an exchange of goods or services with another entity.

Example of a Closing Entry

What accounts do you close in closing entries?

There are four closing entries, which transfer all temporary account balances to the owner’s capital account. Close the income statement accounts with credit balances (normally revenue accounts) to a special temporary account named income summary.

The amount of revenues and expenses from one period to the next are independent of each other. Thus, at the end of an accounting period, revenues and expenses must be closed out and so they can start anew at zero balance for the next period.

The income summary account serves as a temporary account used only during the closing process. It contains all the company’s revenues and expenses for the current accounting time period.

Strictly speaking, accounts payable (AP) are not expenses—although you might colloquially refer to both of them as expenses, the accounting terms mean two different things. Accounts payable and expenses fall under two separate general ledger (GL) accounts. Generally, the accounts payable GL is for money owed that hasn’t been paid yet, whereas expenses are costs which have already been incurred.

Income summary is an account used specifically for the closing process. For example, if your small business has $100,000 in revenue, you would debit $100,000 to the revenue account and credit $100,000 to the income summary account.

Unit 4: Completion of the Accounting Cycle

- An adjusting journal entry involves an income statement account (revenue or expense) along with a balance sheet account (asset or liability).

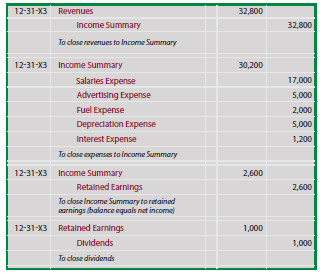

Now Paul must close theincome summary accountto retained earnings in the next step of the closing entries. If a company’s revenues were greater than its expenses, the closing entry entails debiting income summary and crediting retained earnings. In the event of a loss for the period, the income summary account needs to be credited and retained earnings are reduced through a debit. Close the income statement accounts with debit balances (normally expense accounts) to the income summary account.

Depending on whether it is a credit or debit balance in the income summary account, the transfer of income summary can be an increase or decrease to retained earnings. Because income summary shows the combined balance from revenue and expense closing entries, a profit will result in a credit balance in income summary and a loss causes a debit balance. While posting a credit balance of income summary to retained earnings increases retained earnings, posting a debit balance of income summary to retained earnings decreases retained earnings.

The journal entries to close expense accounts are to credit the expense account and debit income summary. The final journal entries are to debit income summary and credit retained earnings for a profit, and credit income summary and debit retained earnings for a loss. A company’s income statement shows the sales, expenses and profits for an accounting period.

An adjusting journal entry involves an income statement account (revenue or expense) along with a balance sheet account (asset or liability). Income statement accounts that may need to be adjusted include interest expense, insurance expense, depreciation expense, and revenue. The entries are made in accordance with the matching principle to match expenses to the related revenue in the same accounting period. The adjustments made in journal entries are carried over to the general ledger which flows through to the financial statements.

In other words, it contains net incomeor the earnings figure that remains after subtracting all business expenses, depreciation, debt service expense, and taxes. The income summary account doesn’t factor in when preparing financial statements because its only purpose is to be used during the closing process. Unlike balance sheet accounts, income statement accounts are temporary. At the end of an accounting period, closing journal entries transfer the income statement account balances to the retained earnings account on the balance sheet. The journal entries to close revenue accounts are to debit the revenue account and credit income summary, which is also a temporary account used for the closing process.

Closing entries are entries used to shift balances from temporary to permanent accounts at the end of an accounting period. These journal entries condense your accounts so you can determine your retained earnings, or the amount your business has after paying expenses and dividends. Creating closing entries is one of the last steps of the accounting cycle. The closing entries for any revenues and expenses are subsequently posted to the existing revenue and expense accounts in the general ledger.

What are the 4 closing entries?

The four basic steps in the closing process are: Closing the revenue accounts—transferring the credit balances in the revenue accounts to a clearing account called Income Summary. Closing the expense accounts—transferring the debit balances in the expense accounts to a clearing account called Income Summary.

A general ledger is a record of all of a company’s accounts and their associated transactions and balances. Revenue, expense and dividend accounts are temporary accounts because they hold a balance for only one accounting period. Permanent accounts, such as assets, in comparison, hold a balance over multiple periods. A company must close the income summary and transfer its balance to the account of retained earnings by posting the income summary balance to retained earnings.

What is a Closing Entry?

To update the balance in the owner’s capital account, accountants close revenue, expense, and drawing accounts at the end of each fiscal year or, occasionally, at the end of each accounting period. For this reason, these types of accounts are called temporary or nominal accounts. When an accountant closes an account, the account balance returns to zero.

Adjusting journal entries can also refer to financial reporting that corrects a mistake made previously in the accounting period. A term often used for closing entries is “reconciling” the company’s accounts. Accountants perform closing entries to return the revenue, expense, and drawing temporary account balances to zero in preparation for the new accounting period.

Without completing closing entries and income summary posting, a company’s retained earnings doesn’t reflect current period’s profit or loss. Now that all the temporary accounts are closed, the income summary account should have a balance equal to the net income shown on Paul’sincome statement.