Cash Equity Definition

The dividend account has a normal debit balance; when the company pays dividends, it debits this account, which reduces shareholders’ equity. Stockholders’ equity can be calculated by subtracting the total liabilities of a business from total assets or as the sum of share capital and retained earnings minus treasury shares.

For example, 1 million shares with $1 of par value would result in $1 million of common share capital on the balance sheet. Let’s look at the stockholders’ equity section of a balance sheet. There are 10,000 authorized shares, and of those, 2,000 shares have been issued for $50,000. At the balance sheet date, the corporation had cumulative net income after income taxes of $40,000 and had paid cumulative dividends of $12,000, resulting in retained earnings of $28,000.

Shareholder equity can also represent the net or book value of a company. Shareholder’s equity can also be expressed as a company’s share capital and retained earnings less the value of treasury shares.

Though both methods yield the same figure, the use of total assets and total liabilities is more illustrative of a company’s financial health. Shareholders’ equity is the initial amount of money invested in a business. In order for the balance sheet to balance, total assets on one side have to equal total liabilities plus shareholders’ equity on the other side. Shareholders equity is the difference between total assets and total liabilities. It is also the Share capital retained in the company in addition to the retained earnings minus the treasury shares.

A balance sheet, along with the income and cash flow statement, is an important tool for investors to gain insight into a company and its operations. It is a snapshot at a single point in time of the company’s accounts – covering its assets, liabilities and shareholders’ equity. The purpose of a balance sheet is to give interested parties an idea of the company’s financial position, in addition to displaying what the company owns and owes. It is important that all investors know how to use, analyze and read a balance sheet.

AccountingTools

Shareholder equity (SE), also referred to as shareholders’ equity and stockholders’ equity, is the corporation’s owners’ residual claim after debts have been paid. Equity is equal to a firm’s total assets minus its total liabilities. Equity is found on a company’s balance sheet; it is one of the most common financial metrics employed by analysts to assess the financial health of a company.

How do you calculate stockholders equity?

Stockholders’ equity is the total amount of capital given to a company by its shareholders in exchange for stock, plus any donated capital or retained earnings. In other words, stockholders’ equity is the total amount of assets that the investors will own once debts and liabilities are paid off.

For the liabilities side, the accounts are organized from short to long-term borrowings and other obligations. All the information needed to compute a company’s shareholder equity is available on its balance sheet.

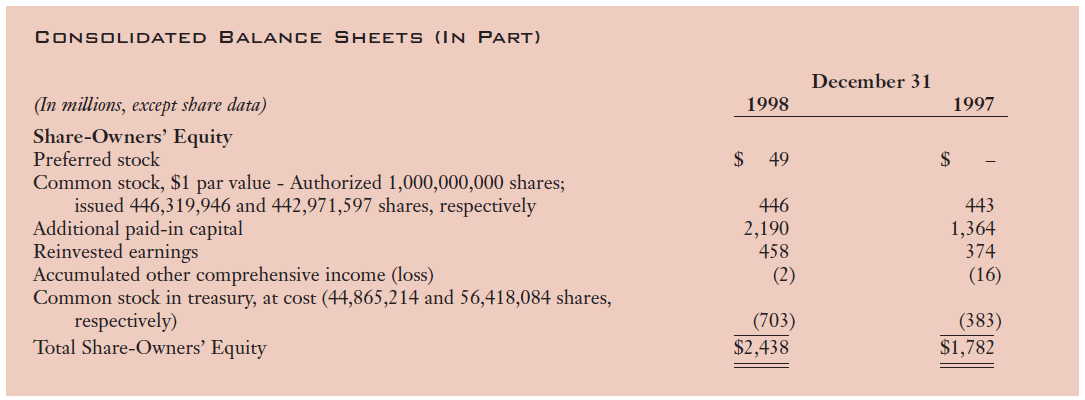

If a company has preferred stock, it is listed first in the stockholders’ equity section due to its preference in dividends and during liquidation. represents the owners’ or shareholder’s investment in the business as a capital contribution.

Some of the accounts have a normal credit balance, while others have a normal debit balance. For example, common stock and retained earnings have normal credit balances. This means an increase in these accounts increases shareholders’ equity.

- Stockholders’ equity might include common stock, paid-in capital, retained earnings and treasury stock.

- Stockholders’ equity, also referred to as shareholders’ equity, is the remaining amount of assets available to shareholders after all liabilities have been paid.

What Is the Stockholders’ Equity Equation?

Shareholders’ equity, which refers to net assets after deduction of all liabilities, makes up the last piece of the accounting equation. Shareholders’ equity contains several accounts on the balance sheet that vary depending on the type and structure of the company.

What is included in stockholders equity?

Stockholders’ equity is the amount of assets remaining in a business after all liabilities have been settled. It is calculated as the capital given to a business by its shareholders, plus donated capital and earnings generated by the operation of the business, less any dividends issued.

Example of How to Use Shareholder Equity

This account represents the shares that entitle the shareowners to vote and their residual claim on the company’s assets. The value of common stock is equal to the par value of the shares times the number of shares outstanding.

This includes both shorter-term borrowings, such as accounts payables, along with the current portion of longer-term borrowing, such as the latest interest payment on a 10-year loan. Preferred stock, common stock, additional paid‐in‐capital, retained earnings, and treasury stock are all reported on the balance sheet in the stockholders’ equity section. Information regarding the par value, authorized shares, issued shares, and outstanding shares must be disclosed for each type of stock.

Another interesting aspect of the balance sheet is how it is organized. The assets and liabilities sections of the balance sheet are organized by how current the account is. So for the asset side, the accounts are classified typically from most liquid to least liquid.

How to Calculate Stockholders’ Equity for a Balance Sheet?

Shareholders equity is the amount that shows how the company has been financed with the help of common shares and preferred shares. Shareholders equity is also called Share Capital, Stockholder’s Equity or Net worth.

To find this information for publicly-held companies, search their most recent financial report online. Once you find this information, you’ll want to add the company’s long-term assets to their current assets to get their total asset value. Then, find their total liabilities by adding their long-term liabilities to their current liabilities.

As you can see from the balance sheet above, it is broken into two main areas. Assets are on the top, and below them are the company’s liabilities and shareholders’ equity. It is also clear that this balance sheet is in balance where the value of the assets equals the combined value of the liabilities and shareholders’ equity.

Stockholders’ equity, also referred to as shareholders’ equity, is the remaining amount of assets available to shareholders after all liabilities have been paid. It is calculated either as a firm’s total assets less its total liabilities or alternatively as the sum of share capital and retained earnings less treasury shares. Stockholders’ equity might include common stock, paid-in capital, retained earnings and treasury stock.

Long-term assets are assets that cannot be converted to cash or consumed within a year (e.g. investments; property, plant, and equipment; and intangibles, such as patents). These are the financial obligations a company owes to outside parties.

Long-term liabilities are debts and other non-debt financial obligations, which are due after a period of at least one year from the date of the balance sheet. Current liabilities are the company’s liabilities that will come due, or must be paid, within one year.