Capital assets explained – FreeAgent

When a company acquires or disposes of a fixed asset, this is recorded on the cash flow statement under the cash flow from investing activities. The purchase of fixed assets represents a cash outflow to the company, while a sale is a cash inflow.

Fixed Asset

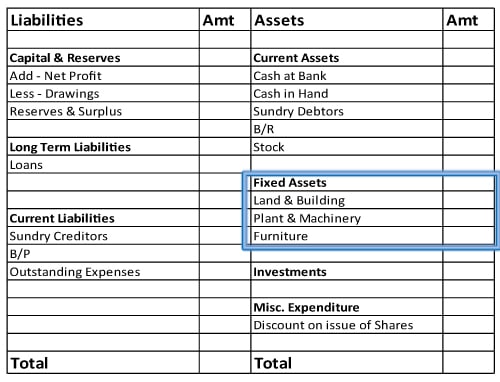

A company’s balance sheet statement consists of its assets, liabilities, and shareholders’ equity. Assets are divided into current assets and noncurrent assets, the difference for which lies in their useful lives. Current assets are typically liquid assets which will be converted into cash in less than a year. Noncurrent assets refer to assets and property owned by a business which are not easily converted to cash.

Also referred to as PPE (property, plant, and equipment), these are purchased for continued and long-term use in earning profit in a business. They are written off against profits over their anticipated life by charging depreciation expenses (with exception of land assets).

Accumulated depreciation is the total amount of depreciation expense that has been charged to profit and loss account from the date of purchase of the fixed asset. A typical case of fixed asset is a producer’s plant resources, for example, its structures and hardware. The word “fix” indicates that these assets won’t be sold in the current bookkeeping year.

For example, understanding which assets are current assets and which are fixed assets is important in understanding the net working capital of a company. In the scenario of a company in a high-risk industry, understanding which assets are tangible and intangible helps to assess its solvency and risk.

If the value of the asset falls below its net book value, the asset is subject to an impairment write-down. This means that its recorded value on the balance sheet is adjusted downward to reflect that its overvalued compared to the market value.

What are examples of fixed assets?

The term fixed assets generally refers to the long-term assets, tangible assets used in a business that are classified as property, plant and equipment. Examples of fixed assets are land, buildings, manufacturing equipment, office equipment, furniture, fixtures, and vehicles.

The balance sheet of a firm records the monetary value of the assets owned by that firm. It covers money and other valuables belonging to an individual or to a business.

What Is an Asset?

A fixed asset is bought for production or supply of goods or services, for rental to third parties, or for use in the organization. The term “fixed” translates to the fact that these assets will not be used up or sold within the accounting year. A fixed asset typically has a physical form and is reported on the balance sheet as property, plant, and equipment (PP&E).

What Is a Fixed Asset?

- Current assets are typically liquid assets which will be converted into cash in less than a year.

- A company’s balance sheet statement consists of its assets, liabilities, and shareholders’ equity.

The different categories of noncurrent assets include fixed assets, intangible assets, long-term investments, and deferred charges. When a company purchases a fixed asset, they record the cost as an asset on the balance sheet instead of expensing it onto the income statement. Due to the nature of fixed assets being used in the company’s operations to generate revenue, the fixed asset is initially capitalized on the balance sheet and then gradually depreciated over its useful life.

A fixed asset shows up as property, plant, and equipment (a non-current asset) on a company’s balance sheet. A company’s fixed assets are reported in the noncurrent (or long-term) asset section of the balance sheet in the section described as property, plant and equipment. The fixed assets except for land will be depreciated and their accumulated depreciation will also be reported under property, plant and equipment. Current assets include cash and cash equivalents, accounts receivable, inventory, and prepaid expenses. Because they provide long-term income, these assets are expensed differently than other items.

This trade is vital to the exactness of your business’ financial records and reports. Detailed documentation of an organisation’s capital adds to the understanding of the financial wellbeing and estimation of that business. Data including fixed assets and depreciation is additionally utilised by potential financial specialists when they are thinking about whether an organisation is a profitable or non-profitable firm.

They are typically used in the balance sheet of the property report as property, plant, and hardware. If your business has a fixed assets, sound accounting standards can fill in as a manual for properly represent these long haul goods on your bookkeeping records. Particular exchanges that influence capital to incorporate the buy, revaluation, devaluation and sale of the asset.

Examples of Fixed Assets

Other noncurrent assets include long-term investments and intangibles. Intangible assets are fixed assets, meant to be used over the long-term, but they lack physical existence.

Fixed assets most commonly appear on the balance sheet as property, plant, and equipment (PP&E). Accumulated depreciation is the cumulative depreciation of an asset that has been recorded.Fixed assets like property, plant, and equipment are long-term assets. Depreciation expenses a portion of the cost of the asset in the year it was purchased and each year for the rest of the asset’s useful life. Accumulated depreciation allows investors and analysts to see how much of a fixed asset’s cost has been depreciated.

In other words, accumulated depreciation is a contra-asset account, meaning it offsets the value of the asset that it is depreciating. As a result, accumulated depreciation is a negative balance reported on the balance sheet under the long-term assets section. The fixed assets include tangible assets mostly such as plant & machinery, building, equipment, furniture etc.

Tangible assets are subject to periodic depreciation, as intangible assets are subject to amortization. The asset’s value decreases along with its depreciation amount on the company’s balance sheet. The corporation can then match the asset’s cost with its long-term value. A fixed asset is a long-term tangible piece of property or equipment that a firm owns and uses in its operations to generate income. Fixed assets are not expected to be consumed or converted into cash within a year.

Capital Expenditures vs. Operating Expenditures: What’s the Difference?

Examples of intangible assets include goodwill, copyrights, trademarks, and intellectual property. Meanwhile, long-term investments can include bond investments that will not be sold or mature within a year. By having accumulated depreciation recorded as a credit balance, the fixed asset can be offset.

Fixed assets additionally incorporate any property that organisation doesn’t sell directly to the customer. Thus, ABC firm acquired a fixed asset worth Rs. 25 lakhs, and this will also reflect in their balance sheet. This fixed asset is useful in calculating overall revenue of the company.

Accumulated depreciation is shown in the face of the balance sheet or in the notes. An asset is anything of monetary value owned by a person or business. In financial accounting, an asset is any resource owned by the business. Anything tangible or intangible that can be owned or controlled to produce value and that is held by a company to produce positive economic value is an asset. Simply stated, assets represent value of ownership that can be converted into cash (although cash itself is also considered an asset).

Revenue is only increased when receivables are converted into cash inflows through the collection. Revenue represents the total income of a company before deducting expenses. Companies looking to increase profits want to increase their receivables by selling their goods or services. Typically, companies practice accrual-based accounting, wherein they add the balance of accounts receivable to total revenue when building the balance sheet, even if the cash hasn’t been collected yet. Fixed assets are recorded as a debit on the balance sheet while accumulated depreciation is recorded as a credit–offsetting the asset.