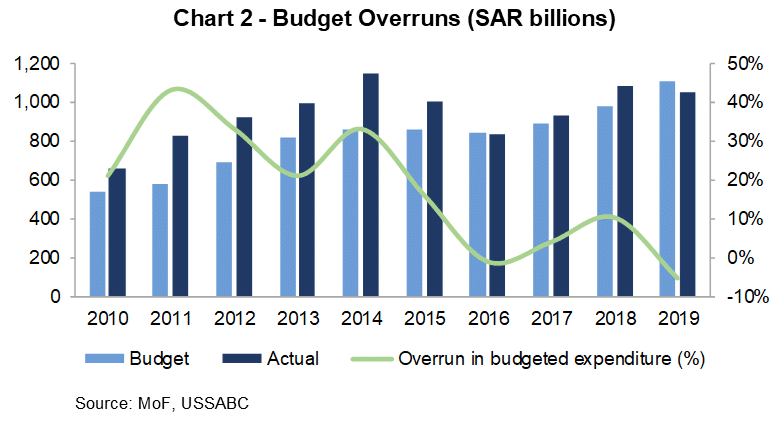

Budget vs Target

Oracle co-CEO Mark Hurd dead at 62, succession plan looms

Be sure to check in periodically to ensure you’re staying within your confines and to adjust as needed for added or lost income sources or expenses. While there are thousands of basic budgeting templates out there, one of my favorites is this template from Money Under 30. It’s simple, straightforward, and within minutes, you will have your bottom line.

Try not to allow your total expenses to exceed your total income. Occasionally exceeding your new income only means that your savings will dwindle. While you can do so from time to time if needed, you should not make a monthly habit of it. Your total income, however, also includes your savings, so if you exceed it, you will go into debt.

Always leave room for these fluctuations and don’t make savings goals that cut your budget too closely. Skip bonuses, overtime, and non-recurring income.

Others can suggest financial goals for you; however, you must decide which goals to pursue. Your financial goals can range from spending all of your current income to developing an extensive savings and investment program for your future financial security.

It usually covers a period in the short-term future. The cash flow budget helps the business to determine when income will be sufficient to cover expenses and when the company will need to seek outside financing. A budget is the sum of money allocated for a particular purpose and the summary of intended expenditures along with proposals for how to meet them. It may include a budget surplus, providing money for use at a future time, or a deficit in which expenses exceed income. Take time to regularly view your savings and investments to determine if they are on track for your savings goals.

Comparing your income and expenses provides your cash flow and insight into where your money is going. This serves as the foundation for creating your financial plan.

Subtract your expenses from your income to see how much money you have left over each month. If you don’t have any money left over, you’ll need to cut expenses or increase your income if you plan to save.

Financial Forecasting

It involves setting spending goals, debt management goals, and savings goals. Many of these tools are easily available to the public in the form of a Microsoft Excel spreadsheet, Mint.com, or FC360 Advisors’ budgeting tool. Once your budget is set up, use your budget to dictate your allowable spending each month.

What is budgeting?

Consider if your current level of risk is providing the returns you’re expecting and make adjustments as necessary. Making alterations is an important part of budgeting, but you can only expect to alter so much. Even if you plan on only spending money on the absolute bare necessities, the prices for many of them, such as gas and food, fluctuate in ways that you may not be able to anticipate.

Monthly Budgeting & Forecasting Model

- Seeing the need to help our clients better manage their money, FC360 has developed a budgeting tool for our clients which helps manage cash flow based on income and expenses.

- Our tool allows our clients to monitor progress on a monthly basis while helping them indentify opportunities for improvement.

The master budget is typically presented in either a monthly or quarterly format, and usually covers a company’s entire fiscal year. There may also be a discussion of the headcount changes that are required to achieve the budget. You’re the boss of your money—and creating a monthly budget is the way you take control. On the hard days, the easy days, the in-between days—EveryDollar is here with tips and info to help you along in your budgeting journey. You can make those money goals a reality—one monthly budget at a time.

There are two tools available to investors that want to take control and plan for their financial future. The first tool—considered by us to be the most important— is a budgeting tool that quickly allows you to practice debt management.

For example, jobs are an income source, while bills and rent payments are expenses. A third category (other than income and expenses) may be assets (such as property, investments or other savings or value) representing a potential reserve for funds in case of budget shortfalls. A budget is a financial plan for a defined period, often one year.

Seeing the need to help our clients better manage their money, FC360 has developed a budgeting tool for our clients which helps manage cash flow based on income and expenses. Our tool allows our clients to monitor progress on a monthly basis while helping them indentify opportunities for improvement. We offer this tool free of charge to our clients as a benefit to help them get one-step closer to achieving their financial goals and dreams. FC360 is also currently working to develop a financial planning solution for our clients in the near future. The master budget is the aggregation of all lower-level budgets produced by a company’s various functional areas, and also includes budgeted financial statements, a cash forecast, and a financing plan.

It may also include planned sales volumes and revenues, resource quantities, costs and expenses, assets, liabilities and cash flows. Companies, governments, families and other organizations use it to express strategic plans of activities or events in measurable terms. Specific financial goals are vital to financial planning.

Budgeting documents how the overall plan will be executed month to month and typically includes estimates of revenue and expenses and expected cash flow and debt reduction. Companies often set up their budgets at the beginning of a calendar or fiscal year and leave room for adjustment as revenues grow or decline. Budgets are compared with actual financial statements to calculate the variances or errors between the two. Cash flow/cash budget – a prediction of future cash receipts and expenditures for a particular time period.

Budgeting represents a company’s financial position, cash flow and goals. A company’s budget is usually re-evaluated periodically, usually once per fiscal year, depending on how management wants to update the information. Budgeting creates a baseline to compare actual results to determine how the results vary from the expected performance. A personal budget or home budget is a finance plan that allocates future personal income towards expenses, savings and debt repayment.

Past spending and personal debt are considered when creating a personal budget. There are several methods and tools available for creating, using and adjusting a personal budget.

Once you understand your current financial situation, you can plan for where you want to be. Now that you know when to budget, let’s talk about how you set up that first budget. “Income” is any money you plan to receive during that month. Budgeting and forecasting allow a business to plan accurately for its fiscal year. Below are 10 ways to improve these processes to create a strategic plan that meets your business’s financial goals.

Finally, think about how much money is required to achieve each goal. However, it is important to understand what achieving your financial goals will require. This information may then be used in comparison with your income and expenses. Look for areas where you can decrease expenses in order to work toward your financial goals. Bringing in additional income will also allow you to achieve your financial goals sooner.

What is budget forecasting?

Budgeting quantifies the expectation of revenues that a business wants to achieve for a future period, whereas financial forecasting estimates the number of revenues that will be achieved in a future period.

To do a monthly budget, start by calculating your monthly income and fixed expenses, like your rent, debt payments, and groceries. Enter this data into a spreadsheet to keep yourself organized, and use receipts or bank statements to figure out how much you usually spend. Then, calculate your other monthly expenditures, like the amount you spend on entertainment.

The second tool is a financial plan or savings goal planner. Budgeting and debt management are crucial because if an individual can set and follow a reasonable spending plan, then they are more likely to be able to save. Setting a budget and following through is an easy process that takes a little work and lots of discipline.