Accrual Accounting

A company that incurs an expense that it is yet to pay for will recognize the business expense on the day the expense arises. Under the accrual method of accounting, the company receiving goods or services on credit must report the liability no later than the date they were received. The accrued expense will be recorded as an account payable under the current liabilities section of the balance sheet, and also as an expense in the income statement. On the general ledger, when the bill is paid, the accounts payable account is debited and the cash account is credited.

For example, revenue is recognized when a sales transaction is made and the customer takes possession of a good, regardless of whether the customer paid cash or credit at that time. To illustrate reversing entries, let’s assume that a retailer uses a temporary employment agency service to provide workers from December 15 to December 29. The temp agency will bill the retailer on January 6 and the retailer is required to pay the invoice by January 10.

A corresponding interest liability will be recorded on the balance sheet. An accrued expense is an expense that has been incurred, but for which there is not yet any expenditure documentation. In place of the expenditure documentation, a journal entry is created to record an accrued expense, as well as an offsetting liability (which is usually classified as a current liability in the balance sheet). In the absence of a journal entry, the expense would not appear at all in the entity’s financial statements in the period incurred, which would result in reported profits being too high in that period. In short, accrued expenses are recorded to increase the accuracy of the financial statements, so that expenses are more closely aligned with those revenues with which they are associated.

Accrued expenses

The accruals are made via adjusting journal entries at the end of each accounting period, so the reported financial statements can be inclusive of these amounts. Utilities provide the service (gas, electric, telephone) and then bill for the service they provided based on some type of metering.

Important Points to Note about Accrued Expense Journal Entry

Further, the company has a liability or obligation for the unpaid interest up to the end of the accounting period. What the accountant is saying is that an accrual-type adjusting journal entry needs to be recorded. Meanwhile, the advantage of the accrual method is that it includes accounts receivables and payables and, as a result, is a more accurate picture of the profitability of a company, particularly in the long term.

What is an example of an accrual?

Accruals concept. July 01, 2018. Accrual Definition. An accrual is a journal entry that is used to recognize revenues and expenses that have been earned or consumed, respectively, and for which the related cash amounts have not yet been received or paid out.

Accruals are revenues earned or expenses incurred which impact a company’s net income on the income statement, although cash related to the transaction has not yet changed hands. Accruals also affect the balance sheet, as they involve non-cash assets and liabilities. Accrual accounts include, among many others, accounts payable, accounts receivable, accrued tax liabilities, and accrued interest earned or payable.

Therefore, prior to issuing the 2019 financial statements, an adjusting journal entry records this accrual with a debit to an expense account and a credit to a liability account. Once the payment has been made in the new year, the liability account will be decreased through a debit, and the cash account will be reduced through a credit. In double-entry bookkeeping, the offset to an accrued expense is an accrued liability account, which appears on the balance sheet. The offset to accrued revenue is an accrued asset account, which also appears on the balance sheet.

The reason for this is that the accrual method records all revenues when they are earned and all expenses when they are incurred. Say a software company offers you a monthly subscription for one of their programs, billing you for the subscription at the end of every month. The revenue made from the software subscription is recognized on the company’s income statement as accrued revenue in the month the service was delivered—say, February. At the same time, an accounts receivable asset account is created on the company’s balance sheet. When you actually pay your bill in March, the accounts receivable account is reduced, and the company’s cash account goes up.

What is the journal entry for accrued income?

Examples of expenses that are are commonly accrued include: Interest on loans, for which no lender invoice has yet been received. Taxes incurred, for which no invoice from a government entity has yet been received. Wages incurred, for which payment to employees has not yet been made.

The revenue recognition principle requires that revenue transactions be recorded in the same accounting period in which they are earned, rather than when the cash payment for the product or service is received. The matching principle is an accounting concept that seeks to tie revenue generated in an accounting period to the expenses incurred to generate that revenue. Under generally accepted accounting principles (GAAP), accrued revenue is recognized when the performing party satisfies a performance obligation.

What Are Accruals?

The accruals must be added via adjusting journal entries so that the financial statements report these amounts. Both accrual and account payable are accounting entries that appear on a business’ income statements and balance sheets. An account payable is a liability to a creditor that denotes when a company owes money for goods or services.

The accrual method enables the accountant to enter, adjust, and track “as yet unrecorded” earned revenues and incurred expenses. For the records to be usable in the financial statement reports, the accountant must adjust journal entries systematically and accurately, and they must be verifiable. Contrary to Cash Basis Accounting, in Accrual Basis Accounting, financial items are accounted when they are earned and deductions are claimed when expenses are incurred, irrespective of the actual cash flow. Accrual accounting method measures the financial performance of a company by recognizing accounting events regardless of when corresponding cash transactions occur.

- The accrued expense will be recorded as an account payable under the current liabilities section of the balance sheet, and also as an expense in the income statement.

- Under the accrual method of accounting, the company receiving goods or services on credit must report the liability no later than the date they were received.

- A company that incurs an expense that it is yet to pay for will recognize the business expense on the day the expense arises.

Journal Entry For Accrued Expenses

When accrued revenue is first recorded, the amount is recognized on theincome statementthrough a credit to revenue. An associated accrued revenue account on the company’s balance sheet is debited by the same amount, potentially in the form ofaccounts receivable. When a customer makes payment, an accountant for the company would record an adjustment to the asset account for accrued revenue, only affecting the balance sheet. Under the accrual accounting method, when a company incurs an expense, the transaction is recorded as an accounts payable liability on the balance sheet and as an expense on the income statement. As a result, if anyone looks at the balance in the accounts payable category, they will see the total amount the business owes all of its vendors and short-term lenders.

Similarly, an accrual basis company will record an expense as incurred, while a cash basis company would instead wait to pay its supplier before recording the expense. A company has sold merchandise on credit to a customer who is credit worthy and there is absolute certainty that the payment will be received in the future.

Journal Entry for Accrued Income

Therefore, an adjusting journal entry for an accrual will impact both the balance sheet and the income statement. The use of accrual accounts greatly improves the quality of information on financial statements. Before the use of accruals, accountants only recorded cash transactions. Unfortunately, cash transactions don’t give information about other important business activities, such as revenue based on credit extended to customers or a company’s future liabilities. By recording accruals, a company can measure what it owes in the short-term and also what cash revenue it expects to receive.

It also allows a company to record assets that do not have a cash value, such as goodwill. On another hand, a decrease in accrued expense happens when a company pays down its outstanding accounts payable on a later date. To recognize a decrease in accrued expense, a company will debit the accounts payable in order to decrease the accounts payable on the liability side and will credit the cash account on the asset side by the same amount. It is to be noted that the cash paid in the current period is not an expense for this period because the corresponding expense has happened and subsequently recorded in the previous accounting period. Therefore, a decrease in accrued expense has no effect on the income statement.

Accrual basis accounting is the standard approach to recording transactions for all larger businesses. This concept differs from the cash basis of accounting, under which revenues are recorded when cash is received, and expenses are recorded when cash is paid. For example, a company operating under the accrual basis of accounting will record a sale as soon as it issues an invoice to a customer, while a cash basis company would instead wait to be paid before it records the sale.

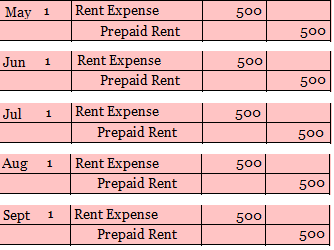

However, as of December 31 only one month of the insurance is used up. Hence the cost of the remaining five months is deferred to the balance sheet account Prepaid Insurance until it is moved to Insurance Expense during the months of January through May. The concept of an accrued liability relates to timing and the matching principle. Under accrual accounting, all expenses are to be recorded in financial statements in the period in which they are incurred, which may differ from the period in which they are paid. An accrued liability is an expense that a business has incurred but has not yet paid.

Accrued revenue is recorded in the financial statements through the use of an adjusting journal entry. The accountant debits an asset account for accrued revenue which is reversed when the exact amount of revenue is actually collected, crediting accrued revenue. Accrued revenue covers items that would not otherwise appear in the general ledger at the end of the period. When one company records accrued revenues, the other company will record the transaction as an accrued expense, which is a liability on the balance sheet. Accrued revenue is the product of accrual accounting and the revenue recognition and matching principles.

When the expense is paid, the account payable liability account decreases and the asset used to pay for the liability also decreases. Accruals and deferrals are the basis of the accrual method of accounting, the preferred method by generally accepted accounting principles (GAAP). Using the accrual method, an accountant makes adjustments for revenue that has been earned but is not yet recorded in the general ledger and expenses that have been incurred but are also not yet recorded.

The accrual method recognizes revenue when the services provided for the client are concluded even though cash isn’t yet in the bank. The sale is booked to an account known as accounts receivable, found in the current assets section of the balance sheet. To record accruals, the accountant must use an accounting formula known as the accrual method.

Assuming the retailer’s accounting year ends on December 31, the retailer will make an accrual adjusting entry on December 31 for the estimated amount. If the estimated amount is $18,000 the retailer will debit Temp Service Expense for $18,000 and will credit Accrued Expenses Payable for $18,000. This adjusting entry assures that the retailer’s income statement for the period ended December 31 will report the $18,000 expense and its balance sheet as of December 31 will report the $18,000 liability. Under the accrual accounting method, an accrual occurs when a company’s good or service is delivered prior to receiving payment, or when a company receives a good or service prior to paying for it. For example, when a business sells something on predetermined credit terms, the funds from the sale is considered accrued revenue.

As a result the company will incur the utility expense before it receives a bill and before the accounting period ends. Accrual accounting, however, says that the cash method isn’t accurate because it is likely, if not certain, that the company will receive the cash at some point in the future because the services have been provided.

Accrual follows the matching principle in which the revenues are matched (or offset) to expenses in the accounting period in which the transaction occurs rather than when payment is made (or received). For example, a company with a bond will accrue interest expense on its monthly financial statements, although interest on bonds is typically paid semi-annually. The interest expense recorded in an adjusting journal entry will be the amount that has accrued as of the financial statement date.

A company can accrue liabilities for any number of obligations, and the accruals can be recorded as either short-term or long-term liabilities on a company’s balance sheet. Payroll taxes, including Social Security, Medicare, and federal unemployment taxes are liabilities that can be accrued periodically in preparation for payment before the taxes are due. The accrual basis of accounting is the concept of recording revenues when earned and expenses as incurred. The use of this approach also impacts the balance sheet, where receivables or payables may be recorded even in the absence of an associated cash receipt or cash payment, respectively.

Accrual accounting is considered to be the standard accounting practice for most companies and is the most widely used accounting method in the automated accounting system. The need for this method arose out of the increasing complexity of business transactions and investor demand for more timely and accurate financial information. An example of an expense accrual involves employee bonuses that were earned in 2019, but will not be paid until 2020. The 2019 financial statements need to reflect the bonus expense earned by employees in 2019 as well as the bonus liability the company plans to pay out.