A Complete Overview of Lockboxes

Banks provide a periodic reviewing service to match the addresses from which customers are issuing their payments to lockbox locations, to see if the lockbox configuration is optimized. If not, lockboxes are shifted to more customer-centric locations, and customers are notified to alter their remit-to addresses to the new locations.

Further scaling the volume of checks based on the ebbs and flows of the business becomes easier without the need to hire additional staff. collect the total sums of money dropped off on a daily (or more frequent) basis from the box. Each payment and any remittance info that has been received are set to process.

Continually shifting lockbox locations is not recommended, since it annoys the accounts payable employees of customers, which must keep updating the pay-to addresses in their computer systems. A lockbox system is an arrangement of several lockboxes that are strategically placed near geographic clusters of company customers, so that aggregate mail time from the customers to the lockboxes is minimized. A lockbox system is encouraged by banks, which earn a fixed monthly fee for each lockbox, as well as a servicing charge for each payment processed. For example, a company in Boston may elect to have lockboxes in Chicago, Los Angeles, Houston, and Miami, in order to reduce the mail float for payments made from customers located near these cities. Lockbox services offer speed and efficiency, getting money into your bank account faster than you’d be able to do it yourself.

Low-Cost Ways To Transfer Money

How does a bank lock box work?

Lockbox system. July 06, 2019. A lockbox is a bank-operated mailing address to which a company directs its customers to send their payments. The bank opens the incoming mail, deposits all received funds in the company’s bank account, and scans the payments and any remittance information.

Also, there is somewhat of a security risk in using lockbox payments. If your bank relies on manual data entry for processing lockbox payments, there is a risk of fraud, whether on the part of an unscrupulous bank clerk or offshore contractor or a customer writing a fraudulent check. Plus the high volume of checks processed means there’s a margin for error.

Whether they’re right for your company or business depends on the volume of payments you receive and whether the cost of lockbox banking is offset by the reduction in mail float and increase in the availability of funds. Lockbox payments are a way for companies to streamline the way they accept money from customers and get access to the cash. When a company uses a lockbox service, they typically set up a special P.O. box for their customers to send payments to; then the bank collects those payments, deposits the cash, and updates the company on their transactions. Many AP departments are modernizing their invoice & payment process to reduce the number of physical checks they have to manually cut & process.

Bank employees who have access to lockboxes are rarely supervised, which opens up the situation to possible fraud. The fraud primarily occurs in the form of check counterfeiting, because the checks that are in the lockboxes provide all the information needed to make counterfeits. Lockbox banking is a service provided by banks to companies for the receipt of payment from customers. Under the service, the payments made by customers are directed to a special post office box instead of going to the company. The bank goes to the box, retrieves the payments, processes them and deposits the funds directly into the company’s bank account.

The Advantages & Disadvantages of Using a Lockbox Collection System

This is especially beneficial if a company is unable to deposit checks on a timely basis or if it is constantly receiving customer payments through the mail. But in today’s digitally connected Internet economy, electronic alternatives to traditional lockbox services have emerged.

While it’s true a lockbox can be faster than a check sent to directly to your organization, lockboxes are not a digital or electronic process. This means that while they may lesson the time that a check is in the mail, they don’t eliminate the time a check is the mail.

Lockboxes work best for companies that receive large payments from customers, such as mortgage firms, but utility companies and others who receive smaller payments also successfully use them. Compare the cost of using your bank’s lockbox to the interest you’ll earn by having payments in your account one, two or more days earlier. A study of the time it takes you to process payments in-house will help you to accurately estimate the money you’ll gain from earlier deposits. Lockbox systems also work well if you have several branches of your business in different locations, or if you have a number of customers in one distant location. Putting a lockbox nearest your customers can reduce the time it takes for their payments to reach you.

Lockboxes are only as secure as the employees in charge of collecting payments from the boxes. These clerical employees may be among the least senior at the bank and susceptible to bribery. In one instance, investigator Stephen G. Korinko with Stroz Friedberg uncovered the theft of $11 million from a large bank’s lockbox service. Part of the lockbox processing is done on a daily basis, so businesses can increase their control and efficiency in receivables management while improving audit controls and data security. Businesses benefit from enhanced reporting capabilities with daily access to deposit amounts, fund availability and payment information, including electronic images of processed payments and coupons.

Lockbox banking accelerates the payment and deposit portion of your cash conversion period in two different ways. First, lockbox banking cuts down on any postal delays caused by having your customers’ payments delivered to your business address. Mail delivered to your place of business entails some extra sorting so that your mail gets into the hands of the correct carrier, not to mention the added time it takes the carrier to actually deliver it to your address. Second, using a lockbox shortens the amount of time necessary to process your customers’ payments, by having your bank open the payment envelopes and deposit them directly into your bank account.

- Companies that have branches in different parts of the country may set up lockboxes near those branches.

- Your employees post the checks after the fact, based on the reports you receive from the bank.

- Instead of checks sitting in your office while an employee matches the payment to a bill and logs the payment into your system, then takes the payments to the bank, the payments go directly to the bank.

Further because the check still must be deposited and processed (albeit by a bank employee), the funds are not available in real-time. The payee might not be set up to accept electronic payments, so the bill-pay service will print out large numbers of paper checks and then mail them to the lockbox, where they will be processed alongside all the other paper checks.

Key Takeaways

Instead of checks sitting in your office while an employee matches the payment to a bill and logs the payment into your system, then takes the payments to the bank, the payments go directly to the bank. Your employees post the checks after the fact, based on the reports you receive from the bank. Companies that have branches in different parts of the country may set up lockboxes near those branches. Depending on where they’re located, customers send payments to the closest lockbox. This shortens mailing time and further speeds up access to funds for the company.

As with most payment processing services, there are both pros and cons to lockbox banking. It provides companies with a very efficient way of depositing customer payments.

While they do speed up processing time, reduce mail float, and provide quicker access to funds, there are still some disadvantages to lockbox payments. For one, though they’re faster than accepting checks at the office, they’re still slow— slower than other electronic means of transfer. Payments must still travel through the mail and be processed before they’re available to accounts receivable.

From there, the bank typically uses an outsourced bpo team to manually process each payment or automatically batch run use OCR and Check21 to scan, capture and process high volume electronic payments and discard the original check. The processed payments are posted to a secure website where the banking staff can be then apply the given funds to the organization’s accounts receivable. Depending on the service level from the bank, daily reports and nightly backups can be applied as needed. If you receive a high volume of small payments, the cost of lockbox banking could quickly outweigh any advantages.

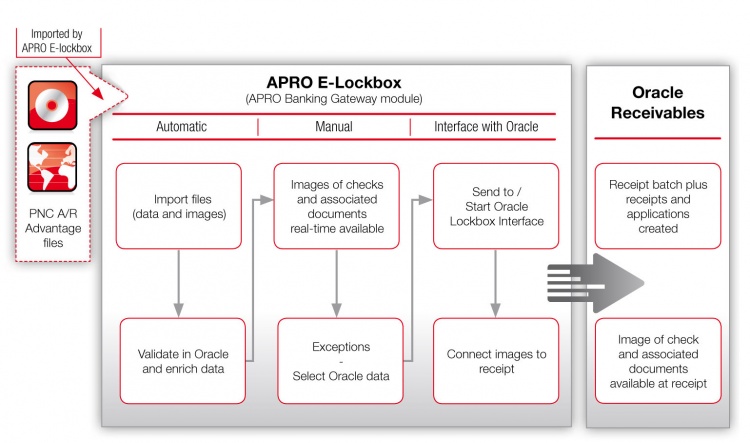

A lockbox is a bank-operated mailing address to which a company directs its customers to send their payments. The bank opens the incoming mail, deposits all received funds in the company’s bank account, and scans the payments and any remittance information. The scanned images are posted to a secure website, where the company’s accounting staff can access the images to apply payments to outstanding accounts receivable. Image-based services scan everything that gets sent to your lockbox so that you can view it online. You can often see images from payments received on the same day they reach the lockbox.

Lockbox payments also reduce “mail float,” or the time between a customer mailing the check and your company receiving it. Remitting payment to a lockbox is an easy, simple way for a customer to send a check for payment or deposit. For the price of a stamp, their payment is delivered reliably and their checks clear quickly.

What Is Lockbox Banking?

You can establish lockboxes in several different post offices or cities. A basic rule is that your lockboxes should be set up nearest to your customers to reduce the amount of time between your customers’ mailing their payments and the deposit into your bank account.

When your payment arrives at the lockbox, it’s collected by the bank along with potentially many other payments, possibly up to several times a day. The bank may scan your remittance slip and check, enabling the company to receive your information in digital format.

Since the payment processing is done at the bank, your customers’ payments are received and deposited all within the same day. Doing this work yourself can delay the deposit of the payments anywhere from one to two days depending on how long it takes you to process your customers’ payments for deposit, and to actually make the deposit at the bank. For businesses that receive a large volume of payments or large-denomination checks accompanied by remittance documents, a lockbox arrangement can streamline collections and payment processing.

Why do companies use a lockbox?

Lockbox banking is a service provided by banks to companies for the receipt of payment from customers. The bank goes to the box, retrieves the payments, processes them and deposits the funds directly into the company’s bank account.

A business establishes a post office box to receive payments from customers. The bank couriers the day’s deposits and communications to its processing center. The business’s remittance documents are scanned, payment information is captured, and clearing updates are transmitted to its accounts receivable. Each night, the business’s lockbox data is backed up for secure storage and easy access. Overall, lockbox payments can save you time, help you manage your business more effectively, and improve customer service.

Lockboxes are commonly used in industries such as business to business services, real estate & property, manufacturing, utility billing, and other cases where high volumes of checks are being sent. One benefit of the lockbox service to the commercial customer is that it can maintain special mailboxes in different locations around the country and a customer sends payment to the closest lockbox. The company then authorizes a bank to check these mailboxes as often as is reasonable, given the number of payments that will be received. Because the bank is making the collection, the funds that have been received are immediately deposited into the company’s account without first being processed by the company’s accounting system, thereby speeding up cash collection.

Utilizing advanced lockbox technology, banks have established multiple communication hubs for businesses to use to receive payments and deposits. SIMPLE DISURSEMENT SYSTEMS Simple Disbursement Systems tend to be manual and paper-based. COMPLEX DISBURSEMENT SYSTEMS Complex Disbursement Systems are characterized by a greater use of electronic payments, specialized disbursement accounts, flexible account funding and greater control and information capabilities. These systems often are linked to the company’s collection and concentration systems to maximize efficiency of funds movement. Lockboxes are strategically placed in a business centric location to reduce mail delivery time as well even encourage a physical drop off by the clients.

The money is deposited and the company is notified of the payment to their account. Lockbox services do not directly integrate with payment methods such as cards, ACH, EDI, or newer Internet based digital payment rails such as eCheck. This adds complexity in a receivable process running different systems for different payment methods. Because the banks are doing lockbox processing at scale, there is efficiency gain with them doing the check processing versus having a staff member do it. There is no need to prepare deposit slips or drive to the bank or build reports.