3.5 Process Costing

You then add them to the already completed units to get 750,000. This gives you the number of equivalent whole units you have produced.

The production cost report takes data from production and reports it as total amounts incurred during the associated time period. This report is used by management to analyze production processes and determine if improvements need to be made to maximize efficiency.

1) Makes no distinction between work done in prior or current periods. 2) Blends together units and costs from prior and current periods. 3) Determines equivalent units of production for a department by adding together the number of units transferred out plus the equivalent units in ending Work in Process Inventory.

We will continue the discussion under the weighted average method and calculate a cost per equivalent unit. There are three sections of the report. This compares total units in production to total units reconciled (those units completed + those units in WIP). The second illustrates the cost per equivalent unit.

Calculate Equivalent Units of Production

However, since the production process takes three weeks to complete, all the units produced in the last half of March will be in WIP inventory at the end of March. Calculate the costs assigned to ending WIP inventory for the Painting department for direct materials, direct labor, overhead, and in total. In the previous page, we discussed the physical flow of units (step 1) and how to calculate equivalent units of production (step 2) under the weighted average method.

You can use the same method for calculating the overhead costs and materials if you know the percentage of completion of each pricing factor. The production manager is told to push his employees to get as far as possible with production, thereby increasing the percentage of completion for ending WIP inventory.

This allows managers to see how much of a product was completed during a specific time period and how much of a product is still in work in progress. It also allows managers to calculate per unit cost of production to help determine unit pricing for customers.

As a result, the equivalent units of direct materials will always be higher than other manufacturing costs. Preliminary figures show current year net income before taxes totaling $1,970,000, which is short of the target by $30,000. Companies determine the efficiency of their manufacturing processes in various ways. One method is to calculate equivalent units of production.

A total of 10,000 units of product remain in the Assembly department at the end of the year. Direct materials are 80 percent complete and direct labor is 40 percent complete. Calculate the equivalent units in the Assembly department for direct materials and direct labor. Each department in the manufacturing process is required to report equivalent units, both those completed and those in working progress (WIP).

Weighted average method of equivalent units of production

- As a result, the equivalent units of direct materials will always be higher than other manufacturing costs.

- Preliminary figures show current year net income before taxes totaling $1,970,000, which is short of the target by $30,000.

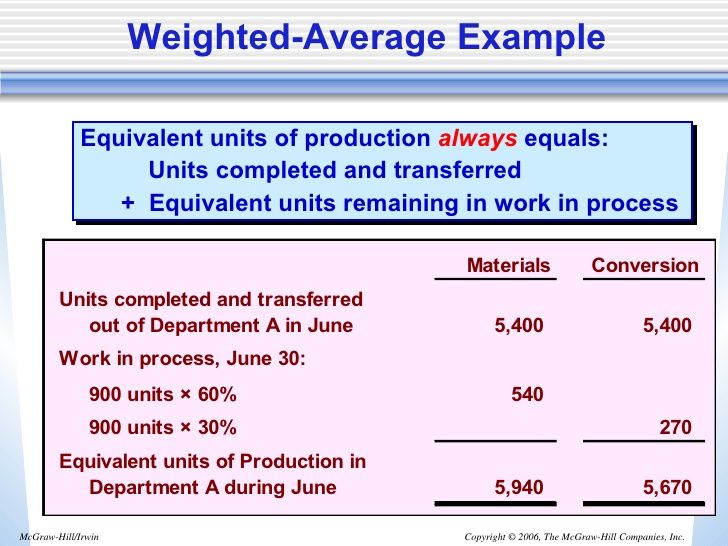

In process costing, the total output of a department during a particular period of time is usually termed as equivalent units of production. In our example, the equivalent units of production of department X is 5,400 units which could be used for computing per unit cost of the department. There is a simple formula that is used to calculate the equivalent units of production for those partially completed units. This formula not only applies to materials that are in continuous production, but also to labor costs and overhead costs.

A production cost report is a departmental report that illustrates all of the information for quick analysis by management. Assume that a manufacturer uses direct labor continuously in one of its production departments.

The weighted average method of computing equivalent units of production blends together the units and cost of current period with the units and cost of previous period. Under this method, the equivalents units of production in a department are equal to the units completed and transferred out plus the equivalent units in in ending work in process inventory.

Example of Equivalent Units of Production

During June, the department began with no units in inventory and then started and completed 10,000 units. In addition, it started 1,000 units but they were only 30% complete at the end of June. The production cost report for this department will indicate that it manufactured 10,300 (10,000 + 300) equivalent units of product during June. The four key steps of assigning costs to units transferred out and units in ending WIP inventory are formally presented in a production cost report.

An average cost per unit is determined by dividing the total cost by the total equivalent units, to ascertain the value of the units completed and units in process. For example, if there are 1,000 units in progress, and the company has only expended 40% of the processing costs on these units, then you have 400 equivalent units of production. The concept of equivalent units is used solely in process costing because you are determining the equivalent unit calculation based on a mass quantity of an item.

What are the equivalent units for direct materials?

An equivalent unit of production is an expression of the amount of work done by a manufacturer on units of output that are partially completed at the end of an accounting period. Basically the fully completed units and the partially completed units are expressed in terms of fully completed units.

Calculate the costs assigned to units completed and transferred out of the Painting department for direct materials, direct labor, overhead, and in total. A total of 6,000 units of product remain in the Quality Testing department at the end of the year. Direct materials are 75 percent complete and direct labor is 20 percent complete. Calculate the equivalent units in the Quality Testing department for direct materials and direct labor. According to this method opening inventory of work-in-progress and its costs are merged with production and cost of the current period respectively.

Join PRO or PRO Plus and Get Lifetime Access to Our Premium Materials

Equivalent units are used to prepare the production cost report. Without this information, you cannot prepare the production cost report. Equivalent Units of Production Units Complete Equivalent Units Completed and transferred 600, percent 600,000 Work in process, ending 600, percent 150,000 Equivalent units equals 750,000. Although 25 percent of the units are unfinished, you can treat them as 150,000 completed units.

Calculate the equivalent units for each of the three product costs—direct materials, direct labor, and overhead. Say you’ve cut enough material to make 600,000 units of shirts. The table shows the computation of equivalent units. To use the FIFO method, only the percentage of beginning parts completed during the accounting period is used, along with the production costs incurred in completing those units.

The production cost report summarizes the production and cost activity within a processing department for a reporting period. A separate report is prepared for each processing department. Rounding the cost per equivalent unit to the nearest thousandth will minimize rounding differences when reconciling costs to be accounted for in step 2 with costs accounted for in step 4.

The third section illustrates cost allocation between completed units and WIP units. The production cost report is a useful tool to aid management in the planning process of operations. It is very dynamic and adaptable to any type of manufacturing process. The units that are currently in production multiplied by the percentage of those that are complete or those that are in process are called equivalent units. It accounts for all the costs related to a department’s production.